Did you know, according to a Gallup study, only 32% of Americans prepare a detailed household budget? If you want to save more money and pay down debt, you need a detailed budget. Find out step by step exactly how I use my monthly household budget template to save over 50% of my income.

If you are interested in using these monthly budget spreadsheets too you can buy them HERE and instantly download them in an Excel file or convert it to a Google Sheet.

With that said let’s get started!

Jump Ahead To:

What Are The Best Tools For Budgeting?

A Microsoft Excel Budget Template or Google Spreadsheet is a good tool to use for budgeting. They help you create your family budget and manage your personal finances. A budget spreadsheet is easy to use, has many features, and can be used while on the go with your phone.

Where a simple budget spreadsheet really shines is it can help you create a plan that is tailor-made and perfect for you.

Additionally, keeping track of expenses over time allows you to see trends in your spending habits. This is very important because it helps you make your budget better and more accurate. Plus, it lets you know where you’re having problems with spending money.

What Is A Budget Spreadsheet?

A budget spreadsheet can be used in either Microsoft Excel or Google Sheets. Once you download it, it can be specially designed for you and your financial needs. These spreadsheets are unique because they allow you to easily customize the template by adding or removing budget categories as needed.

Simply input your numbers, and a budget spreadsheet will automatically calculate your net income and expenses. You can then read off the total spending for each month and automatically see if you’re overspending in any area.

This is especially useful for anyone who spends more than they should on eating out, entertainment, or other items.

Do I Have To Use A Budget Spreadsheet?

You don’t have to use a monthly budget spreadsheet, but it does offer several advantages over using traditional pen and paper or a free budget worksheet PDF.

For one, the data automatically calculates at each cell as you enter your expenses and income, which is much more difficult to do by hand.

Also, a personal budget spreadsheet is a great money management tool because it will automatically put expenses in their correct expense category, saving you the hassle of having to manually assign categories.

The best budget spreadsheets monitor your spending habits and cash flow over time to give you an accurate picture of where your money is going each month. This allows you to get control of your finances and make more informed decisions about how much should go towards which categories.

The best thing about a Google spreadsheet is that you can share it with your spouse. This helps to make sure your entire household can stay on the same page when it comes to money management, saving money, and achieving your financial goals.

A Budget Spreadsheet Allows You To See You Spending Trends Over Time

A personal budget spreadsheet will allow you to see your spending trends over time. You need to add your income and expenses every month so you can see your progress.

While some people may think of it as a pain to spend time each month updating their budget spreadsheet, it’s an important part of the process. This is because you’ll be able to see what areas are spending the most money over time and where you need to cut back.

What Does A Normal Personal Or Household Budget Look Like?

Every individual or household will have different spending habits, there is no right or wrong way to plan your budget.

So I’m going to share with you my monthly budgeting method. You can use this for yourself as an example.

How To Use My Budget Spreadsheet

1. Determine Your Take-Home Pay

First, I start by determining my take-home pay every month. Since I’m self-employed I take the average of all my monthly income for the year to determine my income. I also make sure to subtract any obligations I have, like taxes and business expenses, to determine my take-home pay.

Action Tips For You:

- Determine how much money you take-home after taxes on a monthly basis.

How:

If you have earned income from an employer where taxes are automatically taken out, it should be fairly easy for you to determine your take-home pay. Whatever you see on your pay stubs is your take-home pay. If you are paid biweekly, you get 26 paychecks a year, so learn how to maximize those three-paycheck months and put that extra income toward your financial goals.

However, if you have automatic deductions from your paycheck, add those back to your check. Some examples of automatic deductions are: for a 401(k) or other retirement accounts, savings, or health and life insurance. This will allow you to see the actual amount of your take-home pay.

If you are self-employed, have irregular income, or other outside sources of income you can use two methods to determine your take-home pay:

- If you have a record of your income for the past 12 months, you can take the average of all your monthly income for the past 12 months. Or if you like to be conservative, use the number from the month you earned your lowest income.

- If you don’t have a long income history, use the income you made from the previous month to determine your take-home pay for this month.

Whatever method you use, be sure to subtract obligations like taxes and business expenses to determine your take-home pay.

2. Determine Your Monthly Expenses

After I figured out my take-home pay, I look to see what my monthly expenses are. The way I determined what my monthly expenses were is I literally sat down and wrote everything I spent money on.

When making my list, I didn’t worry about how much I actually spent; I just wanted to list the things I spent my money on.

When I concluded I listed everything I could think of, I started to figure out how much I spent on each item on my list. Some things I knew exactly how much I spent because it was a fixed expense. A fixed expense means it cost the same every month (like rent, cable, internet, and student loans).

Figuring out my variable expenses were a little more difficult. A variable expense just means the expense varies or costs a different amount every month. Some examples of variable expenses are electricity, grocery bills, or gas.

For the expenses I wasn’t sure about, I would look at old credit card statements and bank statements. This allowed me to see what I normally spent on things in a particular category. If there was anything on my list that I still wasn’t sure how much I spent, I would make an educated guess.

Action Tips For You:

- List all expenses for the month.

- Write down how much you actually spend on each expense.

How:

Write down a list of all your expected expenses for the month. If you are not sure what your expected expenses are, start by looking at what areas you spent money on in the past three months. You can find this information by reviewing your past credit card and bank statements.

You can download this list of over 80 budget subcategories to make sure you include everything in your budget.

A lot of people often go wrong when making a budget because they accidentally leave out categories that will require money at some point. That can throw your whole budget off.

This list is designed to cover as many personal budget categories as possible. Don’t get overwhelmed by this list, because not every category will apply to you. Go through the checklist, and put a check next to each item you spend money on. Then include those categories in your budget.

Once you make your list, start writing how much you normally spend in that area. Unfortunately, you will not be able to account for the areas where you spent cash. However, it will provide you with a rough outline of your spending.

If there are any spending categories that you can’t figure out how much you spent, just take a guess of what you think you spent. Make sure to include a “miscellaneous” category as a catch-all for any expenses you may have forgotten to list.

Be prepared to devote some time to this task. It can be very tedious, but it’s important not to skip this step. This is the foundation of making a real budget that will work. The good news is once you do this, you rarely have to do this again because you usually spend money in the same categories every month.

3. Determine How Much to Spend In Each Budget Expense Category

After establishing my monthly income and what I actually spend, I look to see if the end result shows more income than expenses. If my expense column is more than my take-home pay, I figure out what areas I can cut back on spending.

Next, I determine if my spending in each category is reasonable. To determine if my spending is reasonable, I start by looking at what the national average is.

For example, if the national average for food and dining out is 10% of your income, and I’m spending 20% of my income, I know this may be an area to consider cutting back.

Finally, I always make sure I allocate at least 10% of my take-home pay to my savings goals.

Action Tips For You:

- Make sure your monthly income is more than expenses.

- Try to match your spending with recommended spending based on the national average (read this article to know how much you should be spending).

- Always pay yourself at least 10% of your take-home pay.

How:

You can read my article “9 Must-Have Budget Categories (and Percentages)” to get a general idea of how much of your income you should allocate to each spending area.

My Monthly Budget spreadsheet makes it easy for you to see exactly what percent of your income is going to what expense categories. This makes it simple for you to compare your spending to the recommended averages I give you in the 9 Must-Have Budget Categories (and Percentages) article.

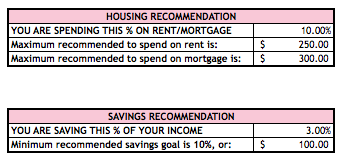

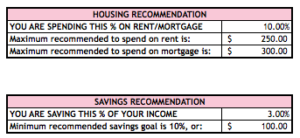

I have included a “Housing Recommendation” section in my Monthly Budget spreadsheet to remind you how much you should be spending on your rent or mortgage. Since housing is usually the biggest expense category we have, spending too much in this area can make or break your budget.

If you notice your spending in a particular area is significantly higher than what I laid out in the 9 Must-Have Budget Categories (and Percentages) article, think of ways you can cut back spending in that area.

If you can’t cut back on one particular high-spend area, see if you can cut back on any other areas to make up for it.

For example, if you live in a high cost of living area, as I do, finding a place to rent that’s 25% of your income is almost impossible. Therefore, maybe you can cut back on other areas, such as transportation (i.e. – get rid of your car), to make up the difference.

Finally, don’t forget to pay yourself in your budget! If you don’t have any money left over in your budget, start determining where you can cut back so that you have money to put toward your financial goals.

My Monthly Budget template includes a “Savings Recommendation” section. This is a great way for you to see the minimum amount of money you should be saving based on your income. Always remember to keep your financial goals in mind when making your budget.

4. Track Your Monthly Spending

Once my budget is set up, I track my spending to make sure that I stick to my spending plan. Personally, I don’t like recording my spending, so I use technology to help me.

I linked all my credit cards and bank accounts to Empower, which automatically logs my spending for me. It is a FREE resource that I highly recommend. I like to visit Empower at least once a week to make sure there are no unauthorized transactions in my bank accounts or on my credit cards.

Finally, reviewing my spending throughout the month allows me to make any necessary adjustments if my spending is going off track.

Action Tips For You:

- Use a daily expense tracker or a tracking system online to keep track of your finances.

- Track your spending every day or at least once a week.

- Review your spending throughout the month. Make any necessary adjustments if your spending is going off track.

How:

I highly recommend using a system like Empower.com to track your spending. I think it makes life so much easier for you to see where you’re spending your money.

However, if you’re not comfortable with linking your bank accounts to a third-party system, there are still other simple ways to track your spending.

You can go online and log on directly to your bank or credit card account and view your spending. A lot of banks make it easy and may break down your spending in different categories in your monthly statement.

In the alternative, if you want to stay on top of your spending and track it more regularly, you can use this FREE Daily Expense Tracker.

Print out multiple sheets (one for each spending category or sub-category). Then put all your sheets in one place (like a binder or folder). I recommend you update your spending every day or every week in the expense tracker.

If you track your spending every day, you should write down what you spend as you go. Make a note on your phone or on a small piece of paper as you spend throughout the day. Then write the numbers in your expense tracker at the end of the day.

If you decide to track your spending every week instead, you can go online to your credit card or bank’s website to see your spending for the week. You can then write down those transactions in your daily expense tracker.

Remember to also keep track of any cash you may have spent since this will not be on your bank statements.

5. Review Your Spending With A Yearly Budget Spreadsheet

At the end of the month, I go to Empower where I can see my spending by category. I then take this information and plug it into my Monthly Budget template.

When I look at my Monthly Budget template, the first question I ask is “Did I stay on budget?”

If I was over budget, I looked at each general spending category to see where I overspent. I can then break it down even more specifically to see which subcategory I overspent.

Finally, at the end of each quarter (every 3 months) I take the numbers from my Monthly Budget and plug them into my Yearly Budget. This allows me to compare my progress from one month to the other.

For example, if I overspent on dining out in January, I can see if I made up the difference by spending less in next month’s budget for February or March.

I also use my Yearly Budget to compare how my income was from month to month. This is especially helpful if you are a freelancer or self-employed like me.

Having all the data in one place allows me to get an idea of what my average income is. This helps me make a more accurate prediction of my take-home pay for when I create my budget next year.

My Yearly Budget is the best way for me to tie everything together. This is the easiest way to see my overall financial progress.

Action Tips For You:

- Plug your spending into the Monthly Budget template at the end of the month.

- Review to see if you stayed on budget. If you did not stay on budget look to see where you overspent and try to do better in next month’s budget.

- Every 3 months, take the numbers from your monthly budget and plug them into your annual budget.

How:

Again, I highly recommend using a system like Empower to see how much you spend every month. It makes it very easy to plug your numbers into the budget spreadsheet.

If you decide to use another method like the Daily Expense Tracker, you just need to plug the totals you have at the bottom of each of your worksheets into your spreadsheets. Each worksheet should represent a spending category or sub-category.

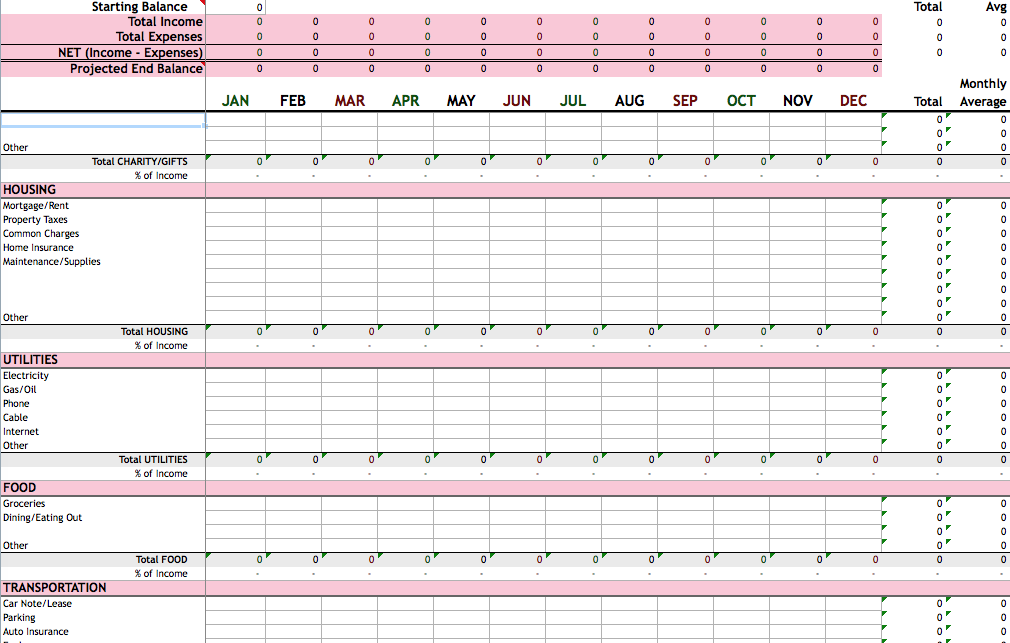

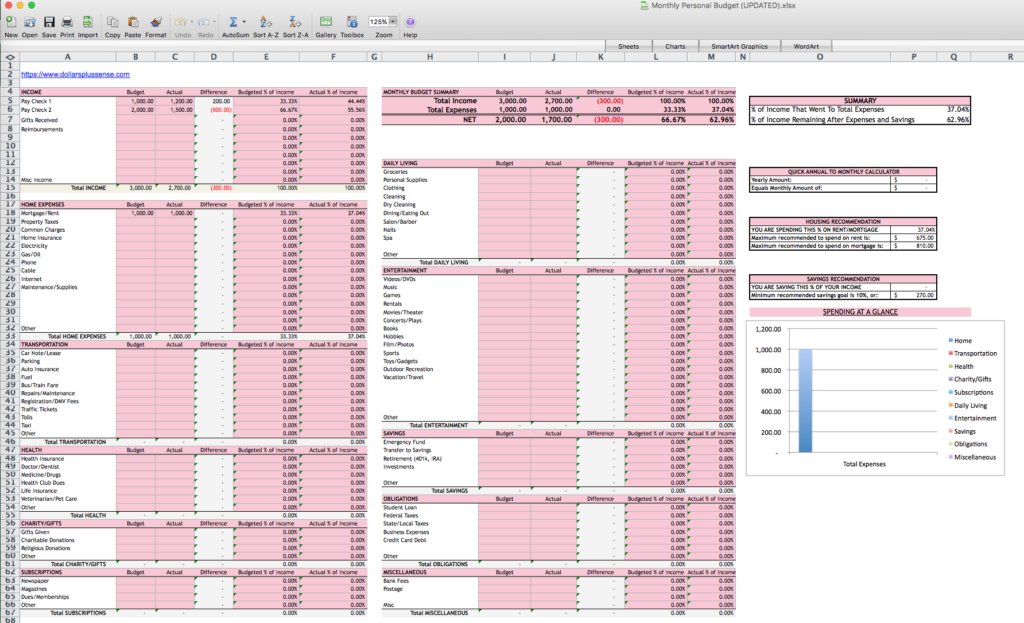

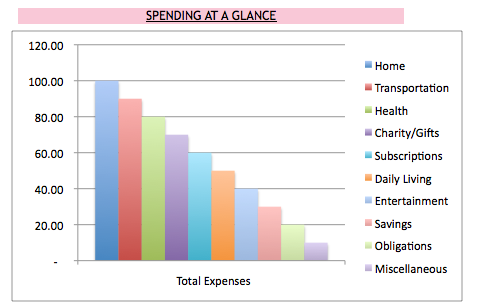

Once all your numbers are plugged into your spreadsheet, the Monthly Budget template will show you the difference between your budgeted spending and your actual spending for the entire month.

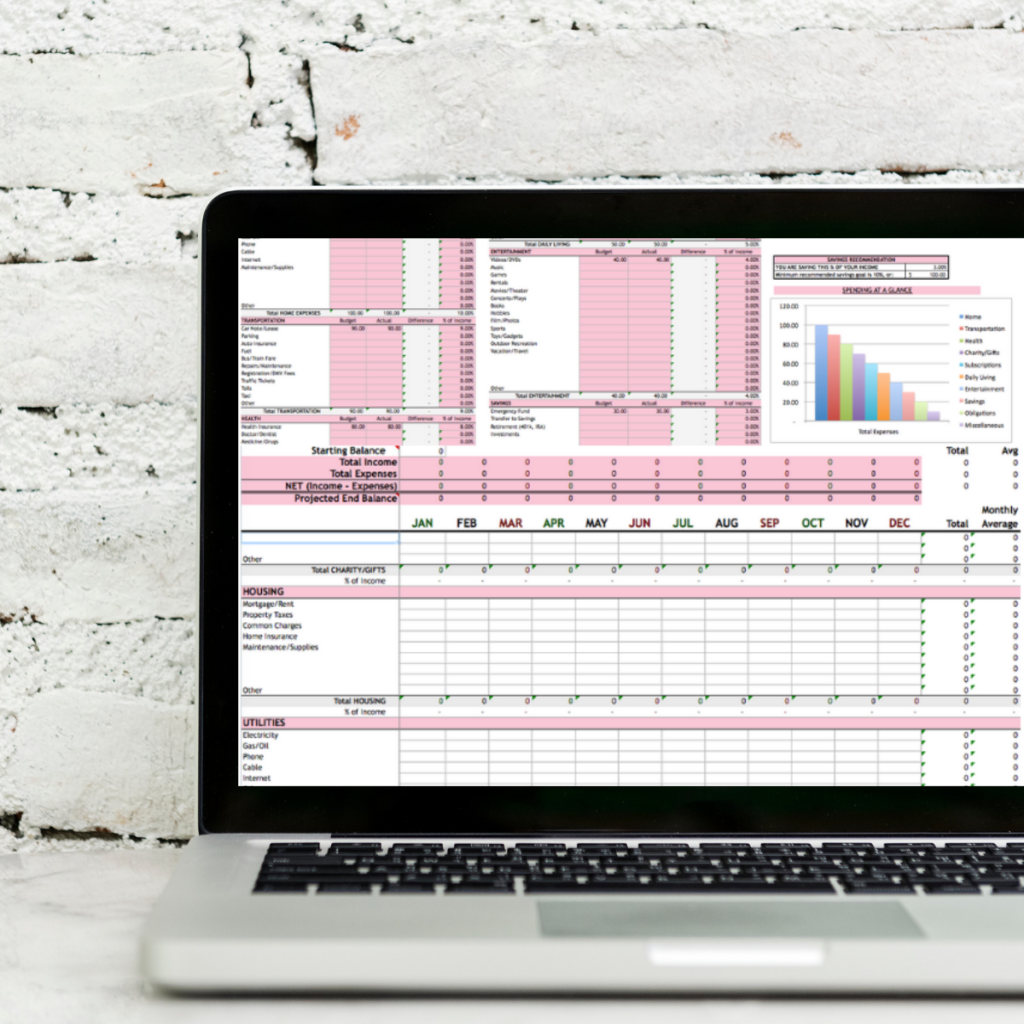

You can also see what percent of your income went to what expenses. Finally, there is a bar graph so you can see your spending at a glance. This bar graph makes it easy to visually see what categories you may be spending excessively.

My budget spreadsheet is very detailed and has 10 general spending categories, which I break up into smaller subcategories. I find that the more detailed your budget is, the easier it is for you to review your spending. This is because everything is accounted for.

The worst thing is to spend a lot of time making a budget, and you still don’t know where your money went because too many things ended up in the general “Miscellaneous” category.

It is important to take a step back and see how you did each month. Did you stay on budget? What areas did you spend much more than you planned? Are there too many things falling into the “miscellaneous” category? If so, consider editing your budget to make a new subcategory.

Finally, use the Yearly Budget spreadsheet to get a bird’s eye view of your overall spending. I recommend doing a check-up every three months to make sure you’re still on track to meet your financial goals.

Whatever method you use, it is important to have a system in place for budgeting and tracking your spending. The most important part of using a budget spreadsheet is making sure you’re reviewing your spending and make adjustments accordingly.

Why Do I Need A Monthly Budget Spreadsheet?

You need a monthly budget spreadsheet because it’s the best way to help you keep track of your income and expenses.

A budget spreadsheet makes it easy to have all of your monthly income and expenses in one place. This way you can easily follow the money coming in vs the money going out, identify opportunities for savings, and see where you are greatly overspending in some areas.

Why Is It Important To Also Have A Yearly Budget Spreadsheet?

It’s important to not just have a monthly budget, but you also need a yearly budget as well.

A yearly budget helps you get a good overall view of your spending. This way you don’t need to go through every single monthly budget spreadsheet to see how you’re doing. You can simply look back at your annual budget when reviewing your spending for that year.

So download the Monthly and Yearly Budget Spreadsheet I made for you and let’s get started!

Here’s a quick video so you can see what it looks like inside:

Summary

You need a budget to meet your financial goals. Start by determining your take-home pay and your monthly expenses. Then determine how much of your money you want to allocate to each spending category. Finally, you can use my templates to track and review your spending.

By using these budget templates, you will get much closer to achieving your financial goals.

I hope sharing my personal system was helpful to you. If you are interested in using any of my budget templates you can find them HERE. Remember, don’t fall into that statistic of not having a detailed budget!

Related Articles:

- Save More Money With The Ultimate Personal Finance Binder

- My Simple 5-Step Formula For How I Saved $300,000 In 4 Years

- How To Budget A Variable Income: 3 Steps

- How To Make A Financial Binder: Supplies List

- A Simple Biweekly Budget Template That Matches Your Pay Schedule

If you want to remember this article, post it to your favorite Pinterest board.

Great, informative post! Love your spreadsheets. I find that organization and a clear picture of my finances are key to handling my money.

Thanks Ana. Me too! I love the calculators to see what my targets are…and graphs to make it really easy to see where my money is going. Thanks for the comment 🙂

How do I purchase the excell spreadsheet?

Hi Rachael. I’m glad you love the spreadsheet as much as I do. You can purchase it at https://dollarsplussense.com/budget-templates-checkout-page/

Thanks for sharing this informative article. It has really nice information.

This spreadsheet is exactly what I needed! It’s so easy to get overwhelmed trying to track both monthly expenses and yearly goals, but this layout brings everything together so clearly. Love how it’s beginner-friendly yet detailed enough for serious budgeting. Thanks for creating and sharing such a practical tool!