Are you finally ready to get out of debt, but you don’t know which debt repayment method to use? In this article, let’s compare the debt snowball vs. debt avalanche method. Find out the difference between the two, and decide which method is best for you.

Jump Ahead To:

What is the Debt Snowball Method?

Money guru, Dave Ramsey, made the debt snowball method famous. It is where you pay off your debts from smallest balance to largest balance, regardless of the interest rates.

To use this method, you start by listing your debt from the lowest to highest balance. Your goal is to pay off your smallest loan balance first. So you pay only the minimum monthly payment on your higher balance debt, while you put any extra money you have towards paying off your smallest balance first.

Once you have paid off one debt completely, take the money that is now freed up and apply it to the next debt in line. You do this until that debt is completely paid off, and then repeat again.

Debt Snowball Calculator

Want to know how long it will take you to pay off your debt using the debt snowball method? You can check out my Debt Payoff Spreadsheet. It calculates your debt-free date, so you know exactly when you’ll be out of debt.

What is the Debt Avalanche Method?

With the debt avalanche method, you pay your debts off from the highest interest rate to the lowest interest rate, regardless of the amount.

To use this method, start by listing all of your debt from highest to lowest interest rate. Next, you pay off the debt with the highest interest rate first (even if it is the debt with the highest amount).

For your lower interest loans, pay only the minimum monthly payment while you put any extra money you have towards paying down your highest interest rate debt. Once you have paid off your highest interest rate debt completely, take the funds that are now freed up and apply them to the next debt in line. Do this until that loan is completely paid off, and then repeat again.

Debt Avalanche Calculator

Check out my Debt Payoff Spreadsheet to see how long it will take you to pay off your debt if you choose to use the debt avalanche method. You can also use this calculator to compare the debt snowball vs. debt avalanche with your own numbers.

Debt Snowball vs Debt Avalanche

Now that you know the difference between the debt snowball and the debt avalanche methods, let’s go over the pros and cons of each.

Pros Of The Debt Snowball Method:

Dave Ramsey recommends this method because it tends to make your debt less overwhelming. As a result, it will probably motivate you to continue on your debt-free journey and not give up.

If you see that you’re paying off a debt rather quickly, you start to feel like you’re actually making progress and want to keep going. Also, by the time you start paying down your larger loans, you will probably be more disciplined about paying off debt. As a result, you will stick with this new habit you’ve formed.

Cons Of The Debt Snowball Method:

Although a lot of people love the debt snowball method, it does come with a big flaw. The biggest con of using the debt snowball method is it can cost you more in interest payments.

Mathematically speaking, it’s not the best debt payoff method if you’re trying to pay the least amount of interest on your debt. Making only the minimum payment on a loan with a 19% interest rate and a high balance can add up to a lot more in interest payments than if you paid only the minimum on an 8% interest loan that has a smaller balance.

Let me give you an example to prove my point:

Let’s say you have two debts totaling $10,000 you want to pay off: 1) a personal loan of $3,000 with an interest rate of 8%, and 2) a credit card debt of $7,000 with an interest rate of 19%. Assume you pay a total of $500 every month towards your $10,000 debt.

If you use the debt snowball method, it would take you 22 months to become debt-free and you would pay a total of $1,961 in interest payments.

If you use the debt avalanche method, it would take you 21 months to become debt-free and you would pay a total of $1,444 in interest payments. As a result, by choosing the debt snowball method, you’re paying $517 more and it will take you an extra month to become debt-free.

Pros Of The Debt Avalanche Method:

The biggest pro of the debt avalanche method is if you stick with it, you will pay the least amount of interest possible and possibly pay off your debt faster. Because of this, it makes the debt avalanche method, the most logical method to choose when paying off debt.

Cons Of The Debt Avalanche Method:

Although the debt avalanche method ensures that you pay the least amount of interest possible, it does have what some would consider a major downside. The biggest con to the debt avalanche method is you may have to wait a long time to feel the joy and satisfaction of paying off a debt — especially if your highest-interest debt is also the largest.

If you start by paying off your biggest debt first (because it has the highest interest rate), you may feel like you’re not making any progress because it’s taking so long to get rid of this debt. When you feel like you’re not making any progress, you will be more inclined to quit.

You also might feel overwhelmed if your highest interest debt is really large — and just give up. If you quit too early, you won’t allow this new habit of paying off your debt to form, and it will make getting out of debt much harder.

Should I Do Debt Snowball Or Avalanche?

So now that you know the difference between the debt snowball vs debt avalanche, and their pros and cons, you might have a hard time deciding which loan payoff method is better.

Mathematically, it makes more financial sense to use the debt avalanche method. You will pay less interest if you pay off your highest-interest debt first. However, staying motivated is more important than saving money on interest.

If you choose to use the debt avalanche method but feel overwhelmed and quit, then what’s the point?

Personally, I chose the debt avalanche method when I was paying off my debt. Because getting out of debt quickly and saving as much money on interest as possible was enough of a motivator for me to keep going. However, I would recommend the debt snowball method for you if:

- You thrive more off of instant gratification,

- You can easily get overwhelmed when you look at your big debts, or

- You feel like you have too many little debts lying around and you want to eliminate those payments.

Debt Payoff Action Plan

Okay, so you finally decided between debt snowball vs debt avalanche and chose the method that’s best for you. Now, let’s make an action play to actually achieve your goal of getting out of debt.

1. Make A Budget

Before you get started on your debt repayment plan, you need to have a budget first. Having a budget allows you to see how much you’re spending every month, and where you can cut your expenses. Cutting your expenses will free up more money for you to put towards you debt.

If you’re just starting out, you can download my FREE Monthly Budget Worksheet.

However, if you want something a little more sophisticated, you can get my Budget Template. This is the template I actually use to help me save over 50% of my income every month.

If you want to learn more about exactly how I use this Excel spreadsheet, you can read my detailed article “How I Use My Monthly And Yearly Household Budget Spreadsheet.”

Once you have your budget set up, we can now focus on ways to pay off your debt.

2. Prioritize Your Debt

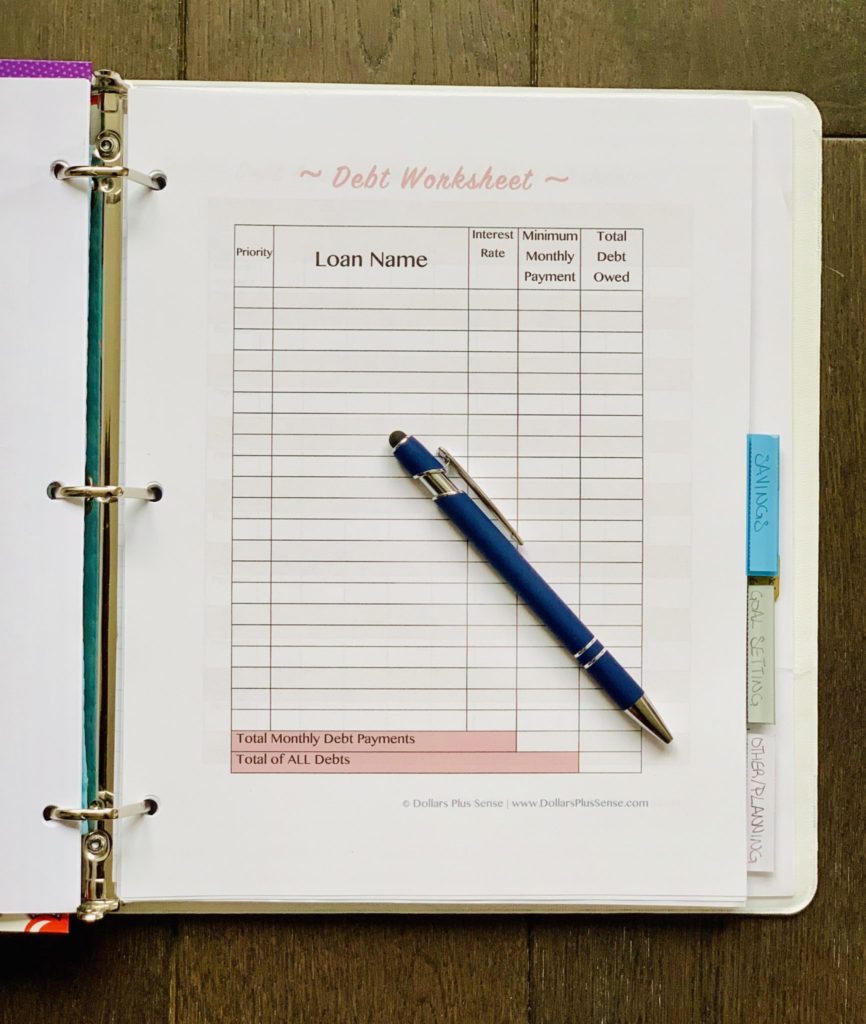

Regardless of the method you choose, you can use my Debt Worksheet in my Shop to help you get organized and prioritize which bills you will pay first.

Sometimes having too many different bills coming in can certainly be overwhelming and hard to keep track of. Therefore, use my Debt Worksheet to help you keep track of this.

Start by listing ALL the debt you’re currently paying. Write down the loan name, the interest rate, the minimum monthly payment, and the total balance of the debt owed.

If you use the debt snowball method, put the #1 next to the debt with the smallest total debt owed under the “Priority” box. Put #2 next to the second lowest total debt owed, and so on.

If you use the debt avalanche method, put the #1 next to the debt with the highest interest rate under the “Priority” box. Put #2 next to the second highest interest rate, and so on.

By using my Debt Worksheet, you will be much more organized and prioritize your payment plan.

3. Use Software To Help

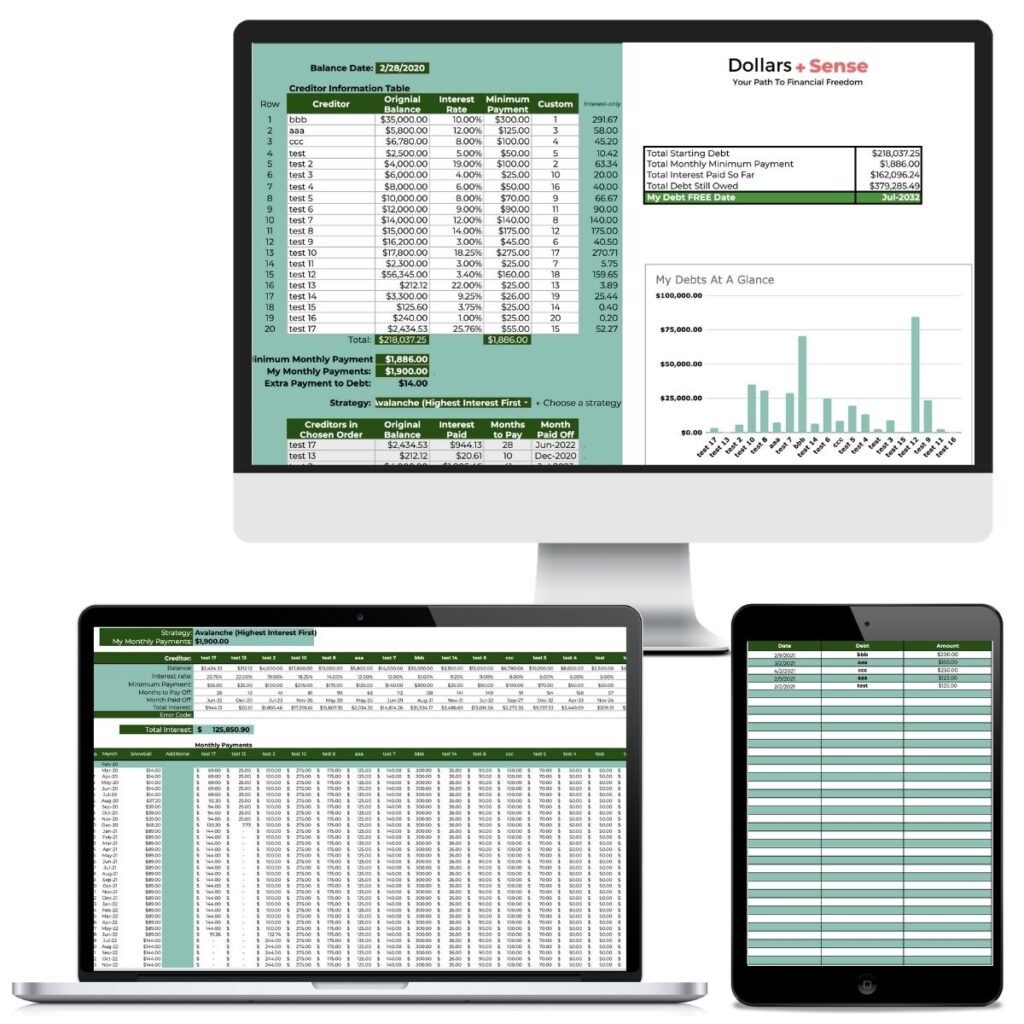

Paying off debt can feel overwhelming, especially when juggling multiple balances, interest rates, and due dates. That’s why having the right tool can make all the difference.

My Debt Payoff Spreadsheet simplifies the process by organizing all your debts in one place, helping you compare the Debt Snowball vs. Debt Avalanche methods to see which will save you the most money, and tracking your progress so you stay motivated. It even calculates your debt-free date, so you know exactly when you’ll be out of debt.

Instead of manually tracking everything or feeling lost in the process, let the Debt Payoff Spreadsheet do the heavy lifting for you.

4. Speed Up Paying Off Your Debt

If you’re eager to become debt-free faster, there are a few strategies that can help you speed up the process. First, look for ways to free up extra cash—this could mean cutting unnecessary expenses, negotiating bills, or using windfalls like tax refunds or bonuses to make extra payments.

Another powerful tactic is the side hustle strategy—earning even a little extra money each month can make a big difference in how quickly you pay off debt.

Finally, consider making biweekly payments instead of monthly ones. This small shift results in an extra full payment each year, which can reduce both your balance and the interest you pay over time. The more you can put toward your debt, the faster you’ll reach financial freedom!

Summary

Deciding whether to use the debt snowball vs debt avalanche method is really based on personal preference. If you’re a numbers person (like me), and want to save as much money as possible, go with the debt avalanche method. However, if your finances are more emotionally based go with the debt snowball method.

Related Articles:

- Paying Debt Vs. Saving: Which Is Best?

- Cutting Your Monthly Expenses: Why It Is Absolutely Necessary

- How I Saved $300,000 In 4 Years

If you want to remember this article, post it to your favorite Pinterest board.

3 Comments on Debt Snowball Vs. Debt Avalanche: Which Method is Best?