Sometimes we have so many financial goals that we don’t know what’s the best way to achieve them. I know when I started my financial journey, I struggled with deciding on if I should pay off my debt first or start saving for the future. In this article we will look at paying debt vs. saving to see which is best.

Jump Ahead To:

Paying Debt Vs. Saving

So which one should you do first? Pay down debt or save for the future? The answer is it depends on your personal financial situation. Let’s go over some possible situations where we compare paying debt vs. saving.

If you don’t have money set aside for emergencies, you need to focus on saving first. I recommend you have at least $1,000 saved before you even think about paying off your debt.

Ideally, you should have 3-6 months worth of living expenses in your emergency fund. I recommend saving three months worth of living expenses if you have relatively strong job security. I recommend six months (or more) if you have some instability in your employment or if finding another job could take you a long time.

When I say “living expenses” I mean only necessities, such as rent and groceries—I don’t mean shopping, entertainment, dining out, or vacations. If you are ever in a situation where you lose your job, so you have to rely on your emergency fund, you shouldn’t be taking vacations or dining out anyway.

- Related Article: How To Build An Emergency Fund

When You Should Focus On Paying Down Debt

If you have an emergency fund, I think you should focus on paying only high interest debt before saving for other financial goals. I consider any debt with an interest rate above 8% to be “high interest.”

The reason why I would pay off any debt with an interest rate above 8% is because the stock market has returned about 8% over the long haul. Paying off a debt with an interest rate greater than 8% is the equivalent to getting a guaranteed return of more than 8% on an investment. Therefore, paying off your high interest debt above 8% will most likely give you a better return on your money than investing in the stock market.

Which Debts Should I Pay Off First?

Before you get started on your debt repayment plan, you need to have a budget first. Having a budget allows you to see how much you’re spending every month, and where you can cut your expenses. Cutting your expenses will free up more money for you to put towards you debt.

If you’re just starting out, you can download this FREE Monthly Budget Worksheet.

However, if you want to get serious with your savings and need something a little more sophisticated, you can get my Budget Template. This is the template I actually use to save over 50% of my income and it is the same template I use to this date.

Once you have your budget set up, we can now focus on ways to pay off your debt.

When deciding which debt to pay off first, I always recommend you pay off your highest interest debt first. This method is called the debt avalanche method. However, for some people, the debt snowball method may work better.

I will go into more details below so you can figure out which method is best for you.

Debt Snowball vs. Debt Avalanche

In my opinion, you should always pay off your highest interest debt first. You will pay less interest if you pay off your highest interest debt first. Therefore, this is the method I have used when getting out of debt, and the method I recommend.

However, some people like the debt snowball method better. The debt snowball method is a debt repayment strategy made famous by money guru Dave Ramsey. It is where you pay off your debts from smallest balance to largest balance, regardless of the interest rates.

Dave Ramsey recommends this method because it is less overwhelming and will probably motivate people to continue on their debt free journey. If you see that you’re paying off a debt rather quickly, you start to feel like you’re actually making progress and want to keep going.

By the time you start paying off your larger debts, you will probably more disciplined about paying off debt and will stick with this new habit you formed.

Mathematically, it makes more financial sense to use the debt avalanche method. However, if you think you’re going to struggle with staying motivated and consistent, then I would go with the debt snowball method. In that case, staying motivated is more important than saving money on interest.

Regardless of the method you choose, you can use this FREE Debt Worksheet found in my Resource Library to get organized and prioritize which bills you will pay first. Sometimes having too many different bills coming in can certainly be overwhelming and hard to keep track of. Therefore, use the FREE Debt Worksheet to help you keep track of this.

Debt Repayment Tools

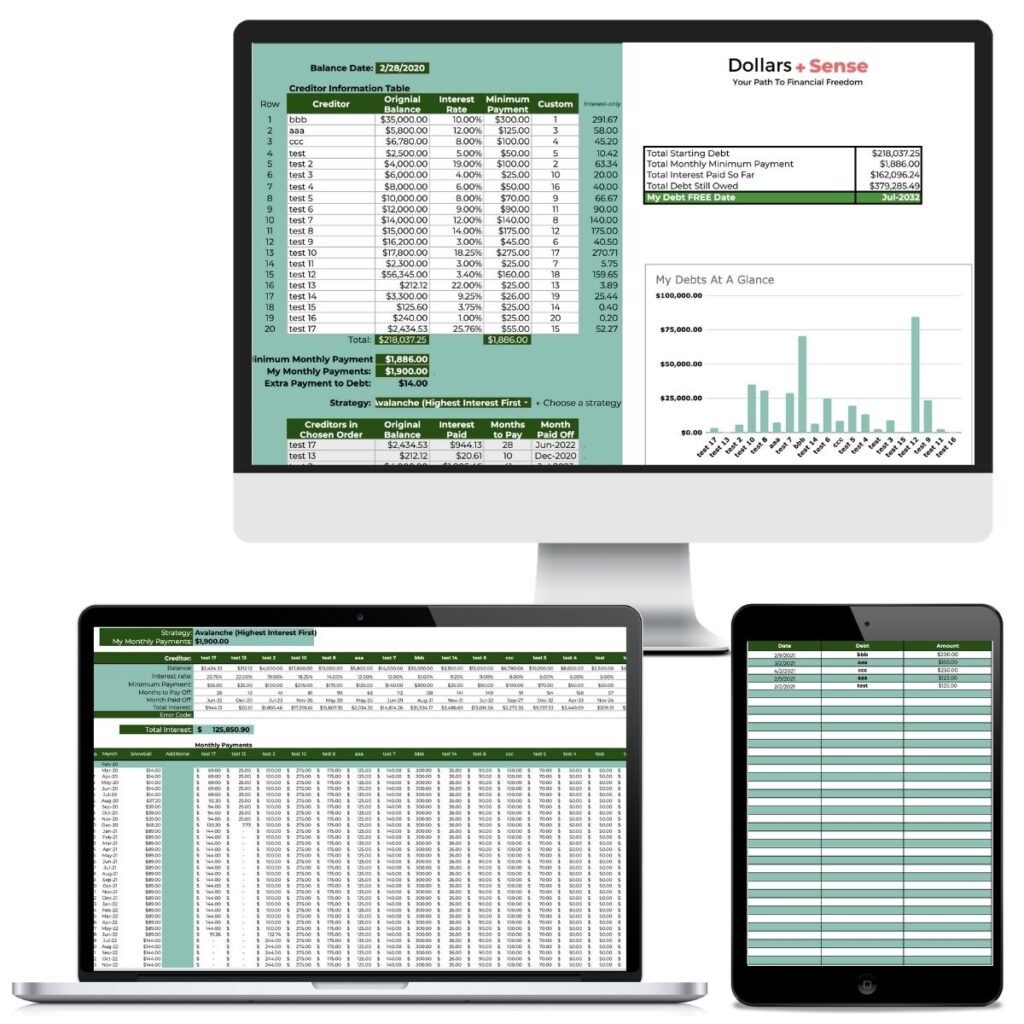

If you’re like me, you like to use paper and software to help you with your financial journey. For those of you interested in using technology to help with your debt repayment plan check out my Debt Payoff Spreadsheet. This spreadsheet will help you create a fully custom debt payoff plan that keeps you motivated…so you can get out of debt and STAY OUT of debt forever.

The Debt Payoff Spreadsheet also easily calculates your debt-free date with just the click of a button. With this spreadsheet you will have a clear roadmap to follow that will get you out of debt faster than you ever thought possible.

- Related Article: How To Pay Debt Faster (Even If You Have No Money And A Low Income)

When You Can Focus On Both

Now that we’ve looked at paying debt vs. saving, there are some times when you need to focus on both. Some situations when I think people should focus on saving and paying down debt are:

- If your employer matches your retirement contribution

- The interest rate on your debt is lower than you would expect to get in the stock market.

Retirement

Regardless of your debt, you should contribute the maximum amount your employer match to your 401(k) or similar plan. If you don’t you’re leaving FREE money on the table! After you contribute the maximum amount to your employer match to your retirement account, all extra money should be put towards debt payoff.

Low-Interest Debt

Focus on paying down debt and saving/investing at the same time if I have only low-interest debt. I personally don’t think ALL debt is bad debt, like some money gurus out there. I like to put my money in the place I think it works best for me.

So for example, I have a student loan with an interest rate of 2.23%. I could completely pay off this student loan in full if I wanted to, but I will get a higher rate of return on my money if I save or invest it instead.

My bank account is giving me a 2.45% return on my money and the stock market on average gives you an 8% return in the long run. So to me, it’s a no brainer to also save/invest while I pay off that debt.

I understand that some people like having the peace of mind knowing they don’t have any debt, and want to pay off all their debt no matter what. If that’s what makes you sleep well at night, then, by all means, do that. Sometimes money isn’t all about math, and we have to do what makes us feel comfortable.

Summary

We’ve looked at paying debt vs. saving, and as you can see, deciding to pay down debt or save is really based on your personal situation. If you do not have a fully funded emergency fund, you should focus on saving more money. Once you have a fully funded emergency fund, you should focus on paying down high interest debt. To pay down your high interest debt, you need to:

- Have a budget; and

- Get organized and prioritize your repayment strategy.

Sign up for your FREE Budget Binder to have all the tools you need to set up a budget.

You can also use tools such as the Debt Payoff Spreadsheet to help you with your debt repayment plan.

Finally, you should focus on saving and paying down debt if your employer matches your retirement contribution; and if the interest rates on your debt is lower than you would expect to get in the stock market.

Related Articles:

- Cutting Your Monthly Expenses: Why It Is Absolutely Necessary

- How I Saved $300,000 In 4 Years

- How To Set Realistic Financial Goals You Can Actually Accomplish

If you want to remember this article, pin it to your favorite Pinterest board.

Want more help with this? The Demolish Your Debt picks up right where this post leaves off — or start smaller with the Debt Payoff Spreadsheet.

I took a rather unpopular approach and saved while I paid down debt. Once I learned about emergency funds, I did ensure that I had enough on hand to cover an unexpected expense however!

Glad to hear you got that emergency fund up! Thanks for your comment! 🙂