Are you currently drowning in debt? If so, I can personally relate to how it feels to be buried in debt. I struggled with a 6-figure debt (from medical bills, credit cards, and student loans) that I had to dig myself out of—and I can show you how you can too. So keep reading to find out how to pay off debt fast with a low income.

Jump Ahead To:

Is It Better To Pay Off Debt Or Save Money?

Before we get started, I want to address whether you should even be paying off debt or if you should be saving money. If you do not have at least $1,000 in an emergency fund, you need to focus on saving money.

I recommend you have 3-6 months’ worth of an emergency fund, but $1,000 is the bare minimum you should have before even considering paying off your debt.

You don’t want to meet your financial goals, and then get thrown off by an emergency. You should have enough cash available to help you through emergencies without having to rely on high-interest loans.

I purposely put the step of paying off debt after saving because creating an emergency fund should be a top priority. This needs to be established before you start paying off debt.

Once you have accomplished building your emergency fund, you should use any additional money towards paying down your high-interest debt.

Also, if you already have an emergency fund set up, I would focus on paying off high-interest debt before saving for other financial goals (such as saving for a house or your child’s education).

- Related Article: Paying Debt Vs. Saving: Which Is Best?

How Do I Pay My Debt If I Live Paycheck To Paycheck?

If you have a low income and are living paycheck to paycheck, you have to be very mindful of your money. So the first thing you need to do is create a budget that works.

1. Create A Budget

Having a budget allows you to monitor your spending and see where your money is going. This will give you valuable information on what areas you can cut back on spending.

If you’re just starting out, you can download this FREE Budget Binder.

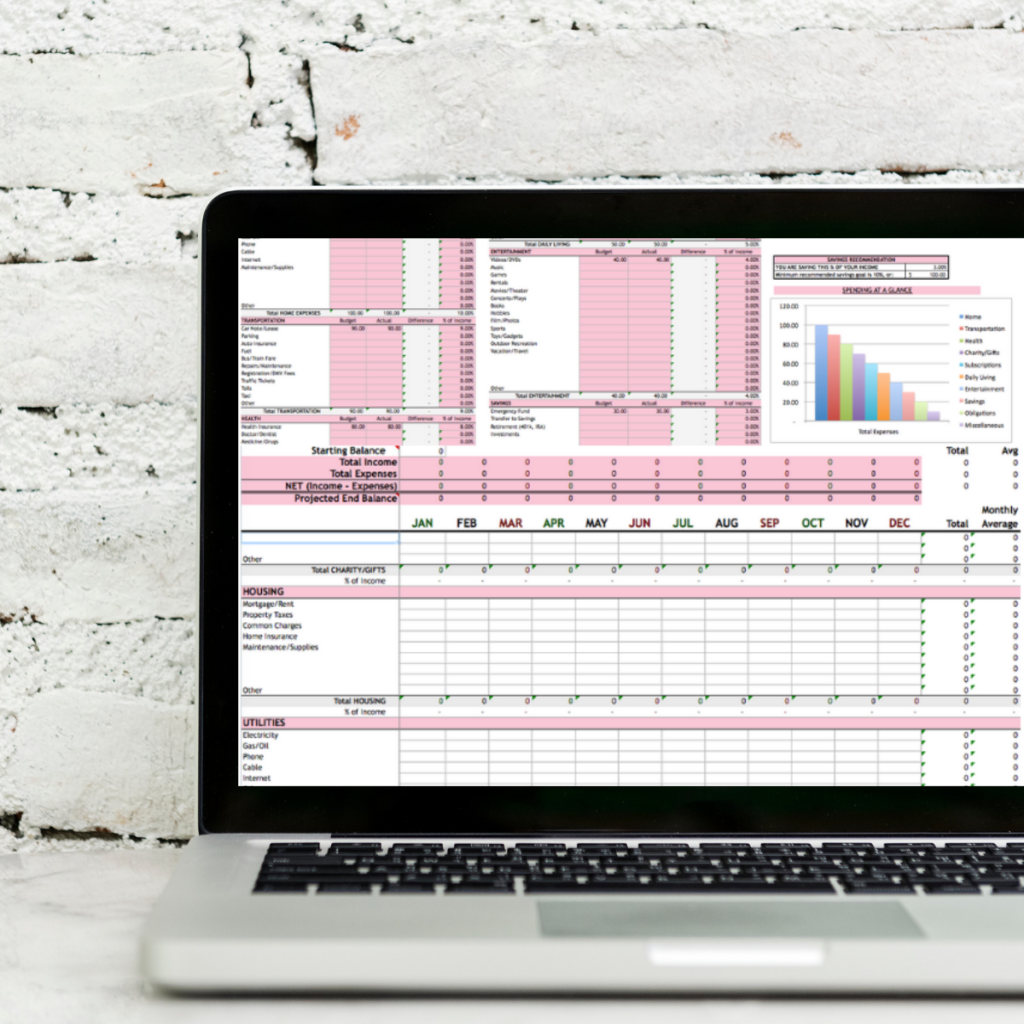

However, if you prefer spreadsheets or need something a little more sophisticated, you can get the Monthly Budget Template. This is the template I actually used to save over 50% of my income, and it is the same template I use to this date.

If this is your first time trying to create a budget, follow these 5 simple steps to set up your budget:

- Determine your net income (take-home pay)

- Determine your monthly expenses

- Determine how much you want to allocate to each spending category

- Track and review your spending

- Make adjustments where necessary.

If you need more help setting up a budget that actually WORKS, read my step-by-step article “How To Make A Budget For Beginners: 5 Simple Steps” where I go into more detail.

2. Track Your Spending

Once you make your budget, you need to track your spending regularly. Tracking your spending will help you make sure you’re still on track with your budget.

Track your spending by keeping receipts and writing down all of your purchases. You cannot rely on your memory to keep track of your spending.

You can use this Daily Expense Tracker found in my FREE Budget Binder to help you with that. Print out multiple sheets (one for each spending category or sub-category). Then put all your sheets in one place (like a binder or folder).

If you hate logging your spending, I recommend you try Empower to help you track your spending. Empower is a free online platform that automatically tracks your spending by linking your credit cards and bank accounts.

All of your transactions are loaded to your Empower account, and you can see all of your finances in one place. The only disadvantage is that you have to manually enter any transactions where you used cash.

It takes about 15-30 minutes to set it up in the beginning (depending on how many bank accounts and credit cards you have), but once you set it up, you can forget it.

When you have a working budget and you’re tracking your spending, it should be clear what areas you tend to overspend. Therefore, make a conscious effort to cut expenses in that area if you’re trying to pay down debt fast with a low income.

3. Cut Expenses

If you want to pay off your debt faster with a low income, you have to cut some of your expenses. This will allow you to free up some money and put it towards your high-interest debt.

Focus On Cutting The Largest Expenses First

When trying to figure out where to cut expenses, I would focus on cutting your largest expenses first. By focusing on the larger parts of your spending, you are able to make the most impact when deciding to cut back.

For example, let’s say you have an income of $2,000/month and 30% of your income (that’s $600) goes to housing and 10% of your income (that’s $200) goes to food every month.

If you can reduce your housing expenses to 25% of your take-home income, that’s $500. So right there, you have a savings of $100/month. You would have to cut your food budget in half just to have that same amount of savings—and that’s much harder to do.

So take a second to figure out what are the three budget categories you spend the most in?

At this point, it should be easy for you to answer this question because you can refer to your budget.

This Monthly Budget Template makes it clear how much of your income goes to what expense. It shows you exactly what percent of your income is being spent on each budget category. This makes it very simple for you to decide where you need to cut back at a glance.

For most of us, our three largest budget categories are housing, transportation, and food. I recommend putting all my energy in trying to get those expenses as low as possible.

Keep in mind, I’m not saying you should not focus on the smaller categories at all. I’m just saying you should focus on cutting your expenses in your high spending categories before you turn to cut your small expenditures.

Next, Focus On Small Expenditures

After you reduce your expenses as much as possible in your three largest budget categories, see if there are any ways you can cut back on the smaller things.

An easy way I like to save money on my smaller expenses is by using online coupons and rebate sites. This helps me to save money any time I shopped in-store or online.

My favorite cashback website is Rakuten. Every quarter they will send you a check or you can get paid through PayPal. When you sign up right now and purchase something through Rakuten you will get $40. If you don’t have an account, sign up right now! It is literally FREE money.

Another option you can use is the Fetch Rewards app. Fetch is a free app that rewards you just for snapping pictures of your receipts. You get free rewards no matter where you shop (from big box stores, mom and pop corner shops, drugstores, liquor stores, and hardware stores – it’s all fair game). No hoops to jump through. No pre-selecting offers, no scanning barcodes, no surveys, no ads…you scan your receipts and you’ll earn points!

If you’re doing your shopping online, you can even scan email receipts by securely connecting your email accounts and Amazon account, to Fetch, and it will instantly scan all of your online receipts for points. Use code “EN9VM” to redeem 1K points!

How Can I Pay Off My Debt If I Have No Money?

At this point, you’ve made a budget, tracked your spending, and cut your expenses as much as possible. By doing these three things, you should have freed up some money that you can put towards your debt. However, if after doing all of these things you still don’t have money, the only other option is to earn more money.

Earn More Money

In order to pay debt fast on a low income, you need to try and earn more money and increase your income.

For example, you can increase your income by:

- Making more money in your current job;

- Moving to a company that may offer more room for advancement;

- Finding a part-time job;

- Starting a side hustle or part-time business; or

- Establishing passive income.

Check out this article where I give you 5 Ways To Increase Your Income Streams.

How Can I Pay Off Debt Fast With A Low Income?

If you have an extremely high debt or interest rate, to the point that you feel like you are not making any progress, I would work towards reducing your debt and/or your interest rates. Here are some steps you can take to reduce your debt or interest rate so you can pay off debt faster:

1. Balance Transfer

If you are faced with a mountain of high-interest debt, consider doing a balance transfer or taking out a personal loan. This strategy can be a powerful tool, but only if used correctly.

I must warn you that if you do not have a plan in place, instead of getting out of debt, you may end up damaging your credit. Therefore, you MUST have a plan before taking this option.

With many balance transfer offers, you can secure 0% APR for up to 15 months. But, you might need to pay a balance transfer fee of around 3% for the privilege. However, it is possible to find a credit card company that does not charge a balance transfer fee.

You can find a list of the best balance transfer credit cards HERE.

Instead of transferring all your debt, only transfer the amount of debt you are confident you can pay off completely during the 0% grace period.

If you do not think you can pay off your debt completely during the 0% grace period, I would still consider transferring your balance under the following circumstances:

- If there is no balance transfer fee, and

- The interest rate with the new credit card company is lower than your current credit card company after the grace period has expired.

Before doing a balance transfer, consider things like:

- The length of your credit history,

- How many recent inquiries you’ve had, and

- What your credit utilization ratio looks like.

All of these things impact your credit score. If you have an extremely low credit score, doing a balance transfer might not be an option.

2. Take Out A Personal Loan

If a low credit score prevents a balance transfer from being an option, consider taking out a personal loan. You can use an unsecured personal loan to consolidate debt.

An unsecured loan means you do not have to put up any collateral, like your house or car.

Consolidating higher-interest debts using a personal loan can save you money in the long run. It brings all of your debt under one new (and preferably lower-interest) umbrella. There’s also the convenience factor of only having to make one monthly payment.

Online lenders typically let you apply for a debt consolidation loan without a “hard inquiry” on your credit.

Hard inquiries will affect your credit score. Therefore, make sure you apply with lenders that use a soft credit pull so you don’t inadvertently impact your credit score in the process.

3. Negotiate A Lower Interest Rate

If you can’t do a balance transfer or take out an unsecured personal loan, you can call your creditor to negotiate a lower interest rate. If you have a good history of paying your bills on time, there is a good possibility that they will grant your request and lower your interest rate.

Don’t just assume your creditor will not cooperate. Take a chance and ask for a lower interest rate. The worst that can happen is they say “no,” and you are in the same position as before. You have nothing to lose and so much to gain by negotiating a lower interest rate.

4. Negotiate A Lower Debt Balance

If the amount of debt you owe is just too high and overwhelming, therefore you cannot afford to pay it, no matter how much your creditors reduce the interest rate, consider negotiating a lower debt balance with your creditors.

You can read some strategies for negotiating with creditors HERE.

This is a great article because it gives you advice on how to negotiate with the particular type of creditor you may have—for example, mortgage companies, car loans, student loans, credit card companies, back taxes, etc.

What Is The Fastest Way To Pay Off Debt?

After you have completed working towards reducing your debt and/or your interest rates, it’s time to turbo-charge your debt pay-off plan. Here are the fastest ways to pay off debt with a low income:

1. Stop Spending

If you really want to get out of debt, you first have to stop spending.

If you have a spending problem, I suggest you stop using your credit cards for your discretionary spending and use cash with the envelope method or pre-paid cards.

Cut up your credit cards—but don’t close your account—if the temptation to spend is too much for you to handle.

Another method you can use is freezing the cards in a cup of ice. By the time you are able to access them again, hopefully, you will have changed your mind about spending.

2. Target Your High-Interest Debt

Debt is a drain on your finances and slows down your achievement of financial freedom. As a result, you want to pay off any high-interest debt first and as quickly as possible.

I consider any debt with an interest rate above 8% to be “high interest.”

The reason why I would pay off any debt with an interest rate above 8% is because the stock market has returned about 8% over the long haul. Paying off a debt with an interest rate greater than 8% is equivalent to getting a guaranteed return of more than 8% on an investment.

Therefore, paying off your high-interest debt above 8% will most likely give you a better return on your money than investing in the stock market.

I suggest you start by paying off the debt with the highest interest rate (even if it is the debt with the highest amount). This is because it makes the most financial sense and you pay less in interest.

For your lower-interest debt, pay only the minimum monthly payment while you are focusing on paying down your highest interest rate debt.

Once you have paid off one debt completely, take the funds that are now freed up and apply it to the next debt in line until that is completely paid off, and then repeat again.

This method is commonly called the debt avalanche system.

Once you pay off all your debt with an interest rate above 8%, it’s up to you if you want to pay off your lower-interest debt or make your money work for you in other ways.

How To Use The Debt Avalanche System To Pay Off Debt

Gather all your debt together, such as your student loans, medical bills, credit cards, tax debt, car note(s), etc. Determine how much you owe and at what interest rate. Write it down and make a list of your debt from highest to lowest interest rate.

For example, let’s say you have the following outstanding debts, which I listed from highest to lowest interest rate:

- Credit Card: $5,000 (20% interest rate) – assume $200 minimum monthly payment

- Student Loans: $30,000 (10% interest rate/10-year loan) – assume $400 minimum monthly payment

- Car Note: $15,000 (8% interest rate/5 year loan) – assume $300 minimum monthly payment

- Student Loans: $10,000 (7% interest rate/10-year loan) – assume $100 minimum monthly payment

- Mortgage: $250,000 (6% interest rate/30-year loan) – assume $1,500 minimum monthly payment

I will presume you reduced your expenses and increased your income; therefore, you have $500 leftover after paying the minimum monthly payment for all your debt. You should apply that extra $500 towards your debt as follows:

- Credit Card: $5,000 (20% interest rate) – $200 minimum monthly payment plus an extra $500 per month ($700 total monthly payment)

- Student Loans: $30,000 (10% interest rate/10-year loan) – $400 minimum monthly payment

- Car Note: $15,000 (8% interest rate/5 year loan) – $300 minimum monthly payment

- Student Loans: $10,000 (7% interest rate/10-year loan) – $100 minimum monthly payment

- Mortgage: $250,000 (6% interest rate/30-year loan) – $1,500 minimum monthly payment

After 8 months, you would completely pay off your credit card bill. Once you pay off your credit card bill, you should pay off your remaining debt as follows:

- Student Loans: $30,000 (10% interest rate) – $400 minimum monthly payment plus $700 that you used to pay off your credit card bill ($1,100 total monthly payment)

- Car Note: $15,000 (8% interest rate) – $300 minimum monthly payment

- Student Loans: $10,000 (7% interest rate) – $100 minimum monthly payment

- Mortgage: $250,000 (6% interest rate) – $1,500 minimum monthly payment

After 2 years and 8 months, you would completely pay off your high-interest student loans. Then you could use this same method to pay off your car note, student loans, or mortgage if you choose.

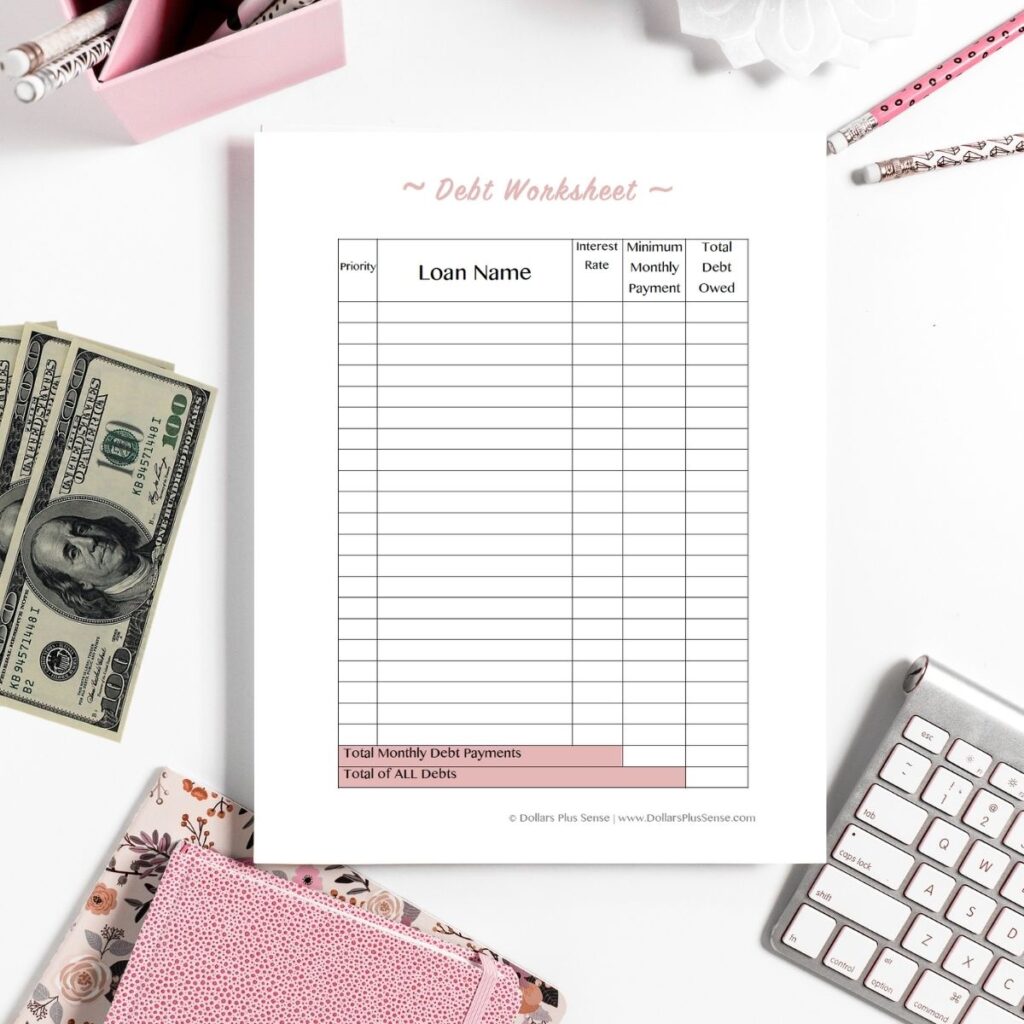

You can use this Debt Worksheet to help you stay organized while you make your debt payoff plan.

Start by listing ALL the debt you’re currently paying. Write down the loan name, the interest rate, the minimum monthly payment, and the total balance of the debt owed.

Put the #1 next to the debt with the highest interest rate under the “Priority” box. Put #2 next to the second-highest interest rate, and so on.

By using this Debt Worksheet, you will be much more organized and prioritize your payment plan.

3. Use Software To Help

If you’re like me, you like to use paper and software to help you with your financial journey.

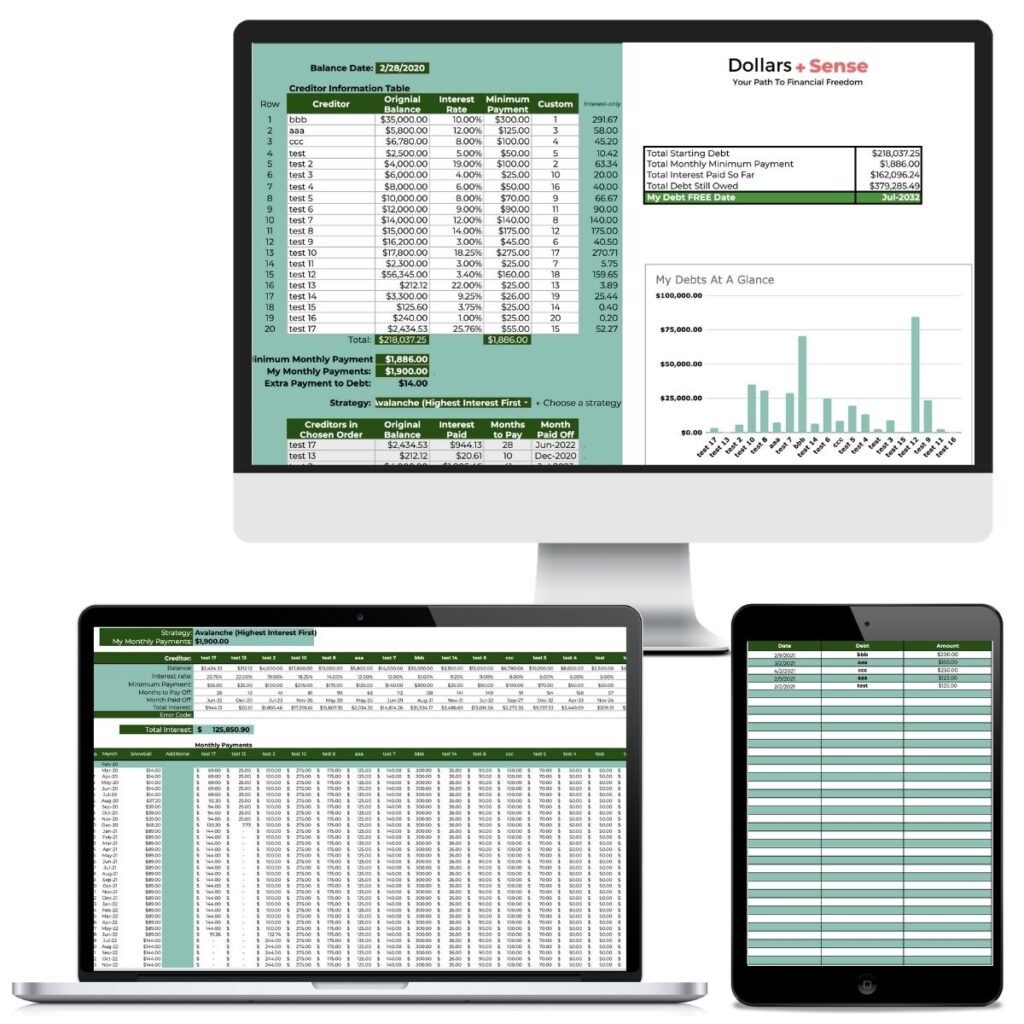

For those of you interested in using technology to help with your debt repayment plan check out my Debt Payoff Spreadsheet. By making a plan for my money, I was able to eventually get rid of my 6-figure (non-mortgage) debt.

This spreadsheet is designed to help you create a custom plan for eliminating your debt so you can pay down balances faster. It also includes a calculator to show you your debt-payoff date and help you stay on track.

You can easily create a debt repayment plan based on the popular debt snowball method (paying the lowest balance first), the debt avalanche method (paying the highest interest first), or experiment with your own custom strategy. So definitely check out my Debt Payoff Spreadsheet.

Summary

Now you know how to pay off debt fast with a low income. However, before you consider paying off your debt, make sure you have an emergency fund set up. When starting your debt repayment plan, try to reduce your debt and/or interest rates. By making a budget, cutting expenses, and increasing your income, you can pay off your debt faster.

No matter how much debt you have, it is crucial to make a plan to find your way out. Getting out of debt certainly will not happen overnight, but you will eventually be debt-free if you make a plan and stick with it. If I could get out of a 6-figure (non-mortgage) debt, you can too! Read more about my inspiring story HERE.

Related Articles:

- Debt Snowball vs. Debt Avalanche: Which Debt Payoff Method Is Better?

- How I Use My Monthly and Yearly Household Budget Spreadsheet

- The Best Way To Prioritize And Achieve Your Financial Goals

If you want to remember this article, pin it to your favorite Pinterest board.

Want more help with this? The Demolish Your Debt picks up right where this post leaves off — or start smaller with the Debt Payoff Spreadsheet.

7 Comments on How To Pay Off Debt Fast With Low Income