Do you feel overwhelmed and don’t know where to start with your financial freedom journey? You might have multiple financial goals that you want to achieve, and ask yourself, “Should I start saving money first? Or should I pay down debt? When should I be investing and saving for retirement?” I understand that it could be overwhelming at first. Find out the step-by-step plan to help you be financially free.

Jump Ahead To:

Step-By-Step Plan For Financial Freedom

In most cases, I recommend following these steps in the exact order presented as you work toward financial freedom.

The only exception is if I suggest skipping a step based on your personal situation. If that happens, consider it a temporary skip—you’ll still want to circle back and complete those steps later on.

Now, let’s get started!

Step 1: Make A Budget

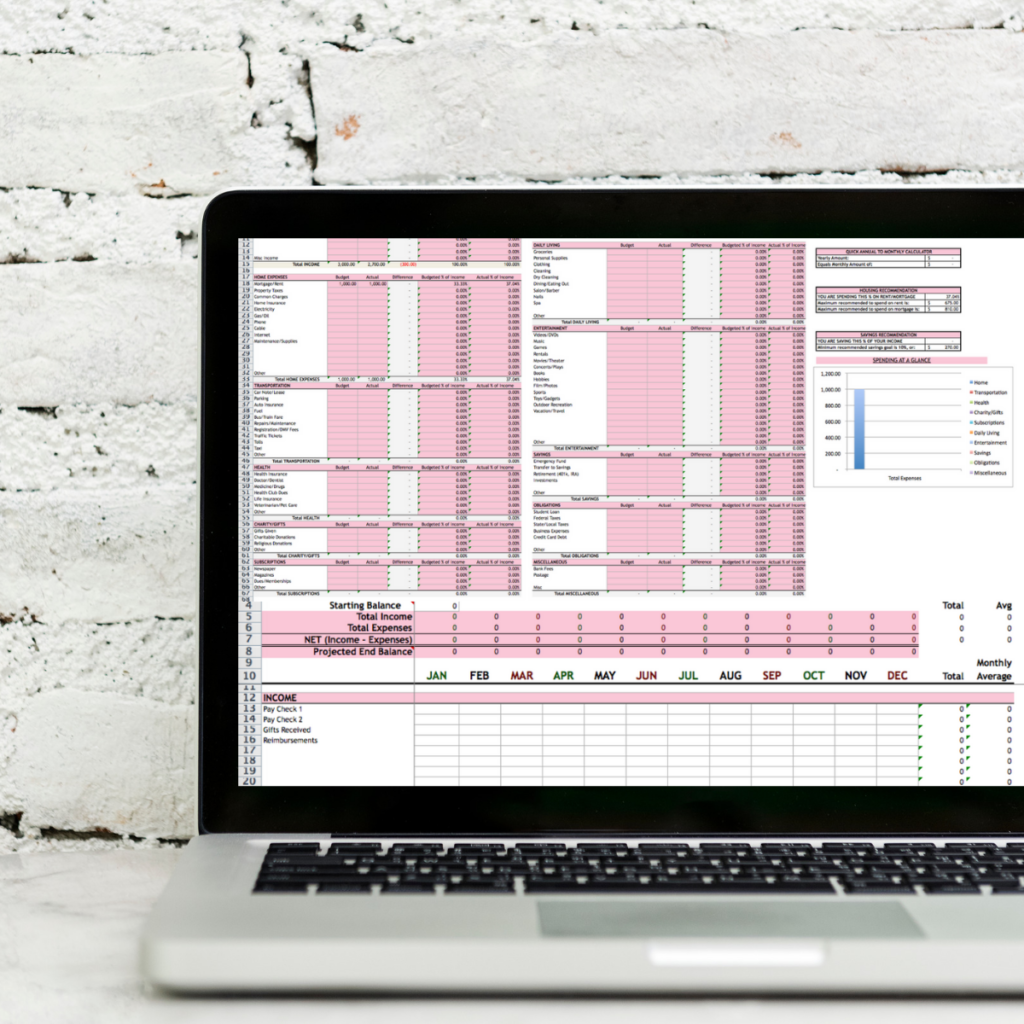

This is absolutely the most important and first thing you need to do. Having a budget is essential to your financial success. You don’t have to budget like I do, but you definitely need to have a spending plan. You can get started with this FREE Budget Binder.

If you have a budget, but you’re ready to take it to the next level, I recommend you use my Budget Templates.

It is the system I currently use when budgeting, and it has helped me save over 50% of my income. It is very detailed and will help you make sure no spending category gets forgotten about.

If you want to know step-by-step exactly how I use my household budget spreadsheet to manage my money, you can read “How I Use My Monthly and Yearly Household Budget Spreadsheet.”

- Related Article: How I Saved $300,000 In 4 Years

*NOTE: If you do not have any money left over after making your budget, skip down to Step 9 and Step 10 before continuing to Step 2.

Step 2: Calculate Your Net Worth

It is important to calculate your net worth because you need to know where you currently stand financially. How will you know if you’re making progress towards your financial goals if you don’t know where you’re starting?

Calculating your net worth is a simple formula—subtract your liabilities from your assets (what you OWN – what you OWE). Find out your net worth quickly and easily with this Net Worth Worksheet.

Calculate your net worth now and recalculate it once or twice a year to check your progress.

Step 3: Set Financial Goals

At this point, you know where you stand with your money and should be thinking about all the things you want to accomplish financially.

Is it paying off debt? Saving for a down payment on a home? Funding your children’s college fund? Saving for a car? Or maybe saving for retirement? It can be some or all of these things.

Ask yourself, “What are ALL the things I want to accomplish financially?” Then write down all of your financial goals.

Once you have all your goals listed in one place, allocate how long you think it will take you to accomplish these goals. Break them down into three different categories: long-term goals, mid-term goals, and short-term goals.

Break Down Financial Goals

A long-term goal takes 10 or more years to achieve. Some long-term goals may be saving for retirement, saving for your child’s college tuition, or paying off a mortgage.

A mid-term goal takes approximately 3-10 years to achieve. Some mid-term savings goals may be saving to buy a car, saving for a down payment on a house, or paying off your high-interest debt.

A short-term goal usually takes less than 2 years to achieve. Some examples of short-term goals are funding your emergency fund, paying down high-interest debt, or saving for a wedding or vacation.

Read “How To Save For Different Financial Goals” to learn the best strategies to save for your different financial goals. You can also use this FREE Daily Goal Planner to take daily action steps towards your goals.

If you want to achieve some of these financial goals faster, skip down to Step 9 and Step 10 before continuing to Step 4.

Step 4: Fully Fund Your Emergency Fund

Saving for an emergency should be one of your financial priorities. An emergency fund is money set aside to cover large unexpected expenses or to help you through hard financial times—like a job loss.

Preparing for the unexpected is necessary if you want to be financially free. You should have enough cash available to help you through emergencies without having to rely on high-interest loans.

Read “How To Build An Emergency Fund” if you need help figuring out how much you need in your emergency fund and how to set it up.

If you already have an emergency fund in place, you can skip to Step 5.

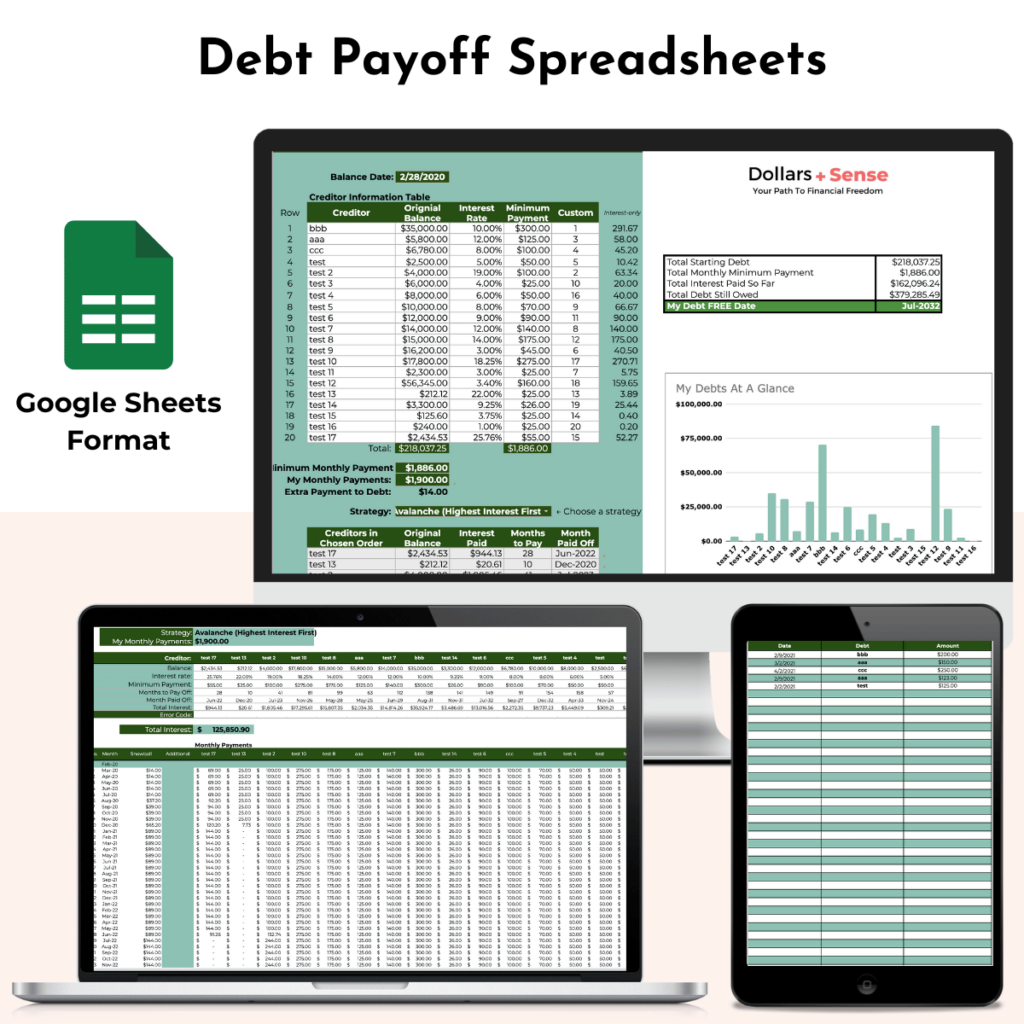

Step 5: Pay Off High-Interest Debt

Once you have fully funded your emergency fund, I would focus on getting rid of any high-interest debt. I consider any debt with an interest rate above 8% to be “high interest.”

The reason why I would pay off any debt with an interest rate above 8% is because the stock market has returned about 8% over the long haul. Paying off a debt with an interest rate greater than 8% is equivalent to getting a guaranteed return of more than 8% on an investment.

Therefore, paying off your high-interest debt above 8% will most likely give you a better return on your money than investing.

You can use this Debt Payoff Spreadsheet to help you organize your debt and prioritize your payment plan. It does the hard work for you—automatically calculates your totals, helps you choose the best payoff method, tracks your progress over time, and even shows you your projected debt-free date so you can stay motivated and on track.

If you do not have any debt, or the debt you currently have is 8% or less, I would move on to Step 6.

Step 6: Save For Retirement

I want to start this section off by saying anyone who is in a position to both payoff debt and fund their retirement plan should do so.

As the generation of baby boomers enters retirement, the payroll taxes that they’ve contributed to the system throughout their careers will turn to withdrawals in the form of retirement benefits.

The amount of money that has been set aside is not enough to cover the long-term expenses of baby boomers that will occur. As a result, it is estimated that social security will run out of money by 2034.

That’s just in time for people around my age to get ZERO when we decide to retire. Therefore, it is imperative that you save for your own retirement and not expect to rely on the government.

I love the Retirement Planning Calculator by Empower. If you want to attain financial freedom, you should definitely use this tool to map out your financial future.

You can upload all of your retirement accounts so you can see it, and manage your finances all in one place. Check in regularly to see how your progress is going—and it’s FREE!

Take Advantage Of Your Employer Match

Saving for retirement is extremely important, and you want to start saving as soon as possible. Regardless of your debt, you should contribute the maximum amount of your employer match to your 401(k) or similar plan.

For example, if your employer will match 50% of your contributions up to 6% of your pay (meaning a maximum matching employer contribution of three percent of your salary)—which is a typical arrangement—then you should contribute 6% to max out the employer match.

That means if you have a salary of $50,000, you will need to contribute $3,000 (6%) to get your employer’s maximum contribution of $1,500 (3%).

I believe even those who are struggling financially can pay off debt and save for retirement—but you have to do so while prioritizing one over the other.

For example, let’s say that you’re carrying a large amount of debt. If you’re struggling to make the payments, then you will need to prioritize paying these off.

But that doesn’t mean that you have to abandon making retirement contributions altogether. You can continue to contribute to your retirement, but do so at some minimal level.

Take Advantage Of The Power Of Compounding

The reason why you want to start saving for retirement as soon as possible is that the sooner you begin saving, the more time your money has to grow and compound.

Compounding is a powerful wealth-building tool because your interest gains interest.

For example, say you have $1,000 invested that gains 10% interest. At the end of the year, you will earn $100 in interest and have a total of $1,100.

If you don’t touch that money and allow your interest to compound, you will earn 10% on $1,100 (not $1,000); therefore, at the end of year two, you will earn $110 in interest.

Let me give you another example to show you the power of compound interest. Assume that at the age of 35, you invest $1,000, which gives you an 8% return annually. To make the math easier, also assume you don’t add any more money to this account.

When you are ready to withdraw from this account during your retirement years, let’s say at the age of 65, your $1,000 will be worth $10,063. However, if you made the same deposit at the age of 25, and withdrew the money at 65, your $1,000 will be worth $21,725!!

You would make more than DOUBLE the amount just by investing 10 years earlier.

If you find you don’t have ANY money to contribute to your retirement while paying down debt, I would skip down to Step 9 and Step 10 before moving on to Step 7.

Step 7. Figure Out Your Investment Strategy

Once you have paid off your high-interest debt and started saving for retirement, you should be focusing on investing.

You cannot only save your way to financial freedom, because that would take forever. You HAVE to invest your money.

There are so many ways you can invest your money. Some ways include investing in stocks, bonds, real estate, and/or a business. You want to invest in things that produce income and increase in value.

I like to invest in real estate and the stock market because, in the long term, it will increase in value over time. It can also produce an income through cash flow and dividend payments.

If you’re considering real estate as part of your wealth-building strategy, my new course, Beginner’s Guide to Buying a House, will help you figure out if homeownership is the right move for you right now—and walk you through the entire buying process step by step.

Investing in real estate and the stock market has helped me achieve financial freedom more quickly than if I were to just save money.

I personally use Robinhood to purchase individual stocks. I like this website and app because you can buy and sell stocks for free—there are no commissions or fees. Sign up today, and you and I can get a free stock like Apple. With Robinhood you also don’t need a minimum account balance, so you can get started right away.

If you are new to investing and really have no clue what stocks to choose, I would recommend using a robo-advisor. A robo-advisor is an online automated advisor. They will invest your money for you based on your specific goals using computer algorithms.

Since robo-advisors are cheaper than what you would pay a human financial advisor, it is a great low-cost option for investing.

A great option to use if you’re just getting started is Acorns. I recommend Acorns for beginners because of its round-up feature. The way it works is you link your checking accounts and credit cards to Acorns and they will round every transaction up to the nearest dollar and invest it.

So let’s say you spent $9.17 at lunch. Acorns will round up that transaction to $10 and invest the $0.83. All your spare change starts to add up, and before you know it, you’re saving and investing. This is perfect for the person who also has trouble saving.

- Related Article: Best Ways To Start Investing For Beginners: Investing 101

Step 8: Protect Your Financial Future

Insurance

You worked hard to get to this step, and you need to protect your assets. Disasters can happen to anyone, even at no fault of your own.

Your car or home can be damaged, someone sues you, a family member gets sick, you become disabled, or someone dies. In events such as this, you want to make sure you have enough insurance to protect you and your family.

You don’t want one of these disasters to be the reason you can’t achieve financial freedom, or you lose the financial empire you’ve built.

Make sure you have ample medical, disability, life, home/rental, and auto insurance. The Chief Mom Officer wrote an excellent article that goes over the different types of insurance you need.

Have A Will And General Power Of Attorney

Finally, you need a Will and a general power of attorney.

You may think, “Do I need a Will if I have no assets?” The answer is “yes!” A will does more than distribute your assets. It can have other functions, such as assigning guardianship to minors.

Even if you have no assets now, suppose you die in a car accident caused by a drunk driver, your estate may have a wrongful death suit that awards them millions of dollars. This will be divvied up by the state if there’s no will.

When someone dies intestate—without a legal will—the estate goes into probate, a judicial proceeding that decides the rightful heirs and the distribution of assets.

Going through probate can eat up more money than the cost of creating a will, or offer a less-than-perfect split of assets. Splitting things equally among family members may not be fair in some cases.

A power of attorney is a legal document that designates another person to act on your behalf to make decisions. A power of attorney is useful if you are not able to act on your own behalf due to mental or physical incapacity.

The person you designate (your agent) may be called upon to make financial decisions to ensure your well-being and care. These may include paying bills or selling assets to pay for medical expenses.

You can detail the scope and extent of what you wish your agent to do in the power of attorney.

BONUS STEPS

These Bonus Steps are not a MUST for some people, but it will definitely speed up and supercharge everyone’s path to financial freedom.

I recommend implementing these next two steps if you want to achieve financial freedom faster or you find you don’t have money left over to save and invest.

Step 9: Find Ways To Cut Expenses

You need to embrace frugality in order to achieve financial freedom quickly. Cutting expenses is important because the less you spend, the less money you will need overall to achieve financial freedom.

An additional benefit to spending less money is you can save more. The more you save, the faster you can achieve your financial goals.

A lot of financial experts would recommend you review your budget and eliminate all small unnecessary expenditures; however, I think you need to first focus on cutting larger expenditures.

The reasoning is since most of our money goes towards the larger budget categories—such as housing, transportation, and food—those are the areas where you can make the biggest impact and recapture the most dollars.

Keep in mind, I’m not saying you should not focus on the smaller categories at all, I’m just saying I would focus on cutting my expenses in my high spending categories before I turn to cutting my small expenditures.

One easy way I would save money on my small expenditures is by using online coupons and rebate sites. A great website I use is Rakuten.

If you don’t have an account, sign up right now! It is literally FREE money. When you sign up right now and purchase something, you will get a $30.00 bonus from Rakuten.

My favorite rewards app is Fetch. Fetch Rewards is a FREE app that rewards you just for snapping pictures of your receipts. That’s really it. Free rewards no matter where you shop (even if you shop online).

Sign up for Fetch Rewards now and use code EN9VM to redeem 2K points! Once you have enough points, you can redeem them for gift cards from popular US-based retailers..

- Related Article: Cutting Your Monthly Expenses: Why It Is Absolutely Necessary

Step 10: Work On Building Other Streams Of Income

To be truly financially free, you need to build multiple streams of income.

This is important for several reasons. First, it creates diversity and protects you if one stream of income “dries up.”

Second, the more streams of income you have, the more money you make—the more money you make, the faster you can become financially free.

You can build other streams of income by getting a part-time job, starting a side hustle or part-time business, or having investments that give you passive income.

If you’re looking for some ways to increase your income or build other streams of income, read my detailed article “5 Ways To Increase Your Income.”

Summary

To become financially free, you first need to create a budget and calculate your net worth. Next, set some financial goals and focus on fully funding your emergency fund and paying off any high-interest debt. Finally, make sure you’re saving for retirement, investing, and protecting your financial future.

As an added bonus to achieve financial freedom faster, try to embrace frugality and work on adding other streams of income. If you follow these tips, you will be well on your way to financial freedom.

I know this was a lot to take in, so download your Financial Freedom Checklist found in my FREE Resource Library, where I outline all of these steps for you! I specifically designed this checklist with you in mind to simplify your steps to financial freedom. It will keep you organized as you start and progress through your financial freedom journey.

There’s nothing more motivating than checking each box off as you make progress. Keep this list as a daily reminder of what you need to do to become financially free.

Now that you know what you have to do, print the checklist and take action today!

If you want to remember this article, pin it to your favorite Pinterest board.

5 Comments on Step-By-Step Plan Every Beginner Needs For Financial Freedom