Are you ready to get your finances under control? If so, it’s so important you try not to make these 21 common money mistakes. These mistakes can end up costing you more money in the long run, or slow down the progress towards your financial goals. Find out 21 financial mistakes to avoid when starting your financial journey.

Jump Ahead To:

What Is A Financial Mistake

A financial mistake is anything that holds you back from achieving your financial goals. Whenever you make a financial mistake, it ends up costing you more money and stress in the long run.

Here are some common financial mistakes you should try to avoid at all cost.

21 Most Common Financial Mistakes To Avoid

1. Not Changing The Way You Think About Money

The first and biggest financial mistake people make is they don’t change the way they think about money. A lot of people don’t realize this, but in order to achieve your financial goals, you have to change your money mindset to have a more positive relationship with money.

The way you feel and think about money impacts how you make financial decisions every day. For example, if when you think about money, it causes negative emotions — such as fear, despair, scarcity, and overwhelm — it seems easier to just ignore your finances because the challenge seems impossible.

However, with a positive money mindset, you look at money from a place of abundance. You don’t focus on how bad your financial situation is; instead, you look at what you can do to change your situation and focus on the path moving forward.

So it’s very important to make sure you have a positive money mindset when trying to achieve any financial goals. If you want to learn how to change your money mindset, you can read my detailed article “How To Change Your Money Mindset So You Can Have More Money.”

2. Not Having A Budget Or Spending Plan

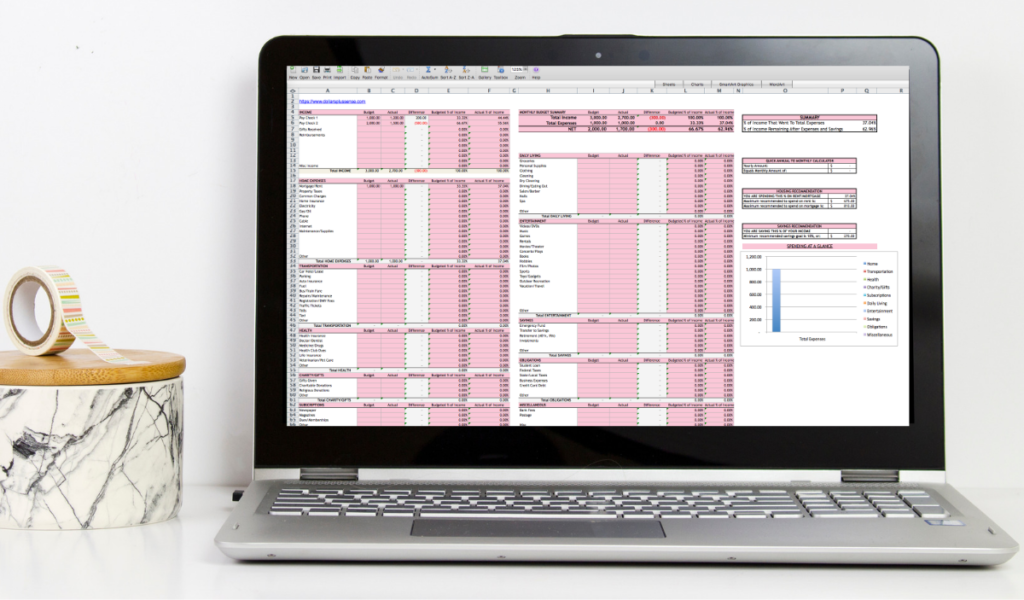

The next biggest financial mistake you can make is not having a budget. Your budget or spending plan is the absolute most important step you need to take when getting control of your finances. No matter where you are financially, a budget will most likely improve your financial situation.

If you’re just getting started, you can use this FREE Monthly Budget Printable or use one of my budget excel templates to start budgeting today.

This budget spreadsheet is how I was able to save over 50% of my income. If you want to learn more about exactly how I use this excel spreadsheet, you can read my detailed article “How I Use My Monthly And Yearly Household Budget Spreadsheet.”

3. You Don’t Have An Emergency Fund

An emergency fund is money set aside to help you through hard financial times (like a job loss). Having an emergency fund will make sure you can still cover your bills if you fall on hard financial times. This is one of the most important things you should have and should be a financial priority.

You should have 3 months’ worth of living expenses if you have relatively strong job security. I recommend 6 months (or more) if you have some instability in your employment or if finding another job could take you a long time.

Since an emergency can come at any time, it’s very important to have quick access to your money. Therefore, I recommend you open a high yield savings account to an online bank account. You get two benefits of banking online:

- They usually pay higher interest on your money than a brick and mortar bank; and

- It reduces impulse purchases because your money is a little harder to access. With online banks, it usually takes a few business days for the money to be transferred to a physical bank where you can withdraw cash.

The bank that I recommend is CIT Bank. CIT Bank is a good online bank to try because it:

- offers competitive interest rates (one of the nation’s top rates),

- has no monthly maintenance fees, and

- you only need $100 to open an account.

Related Article: How To Build An Emergency Fund

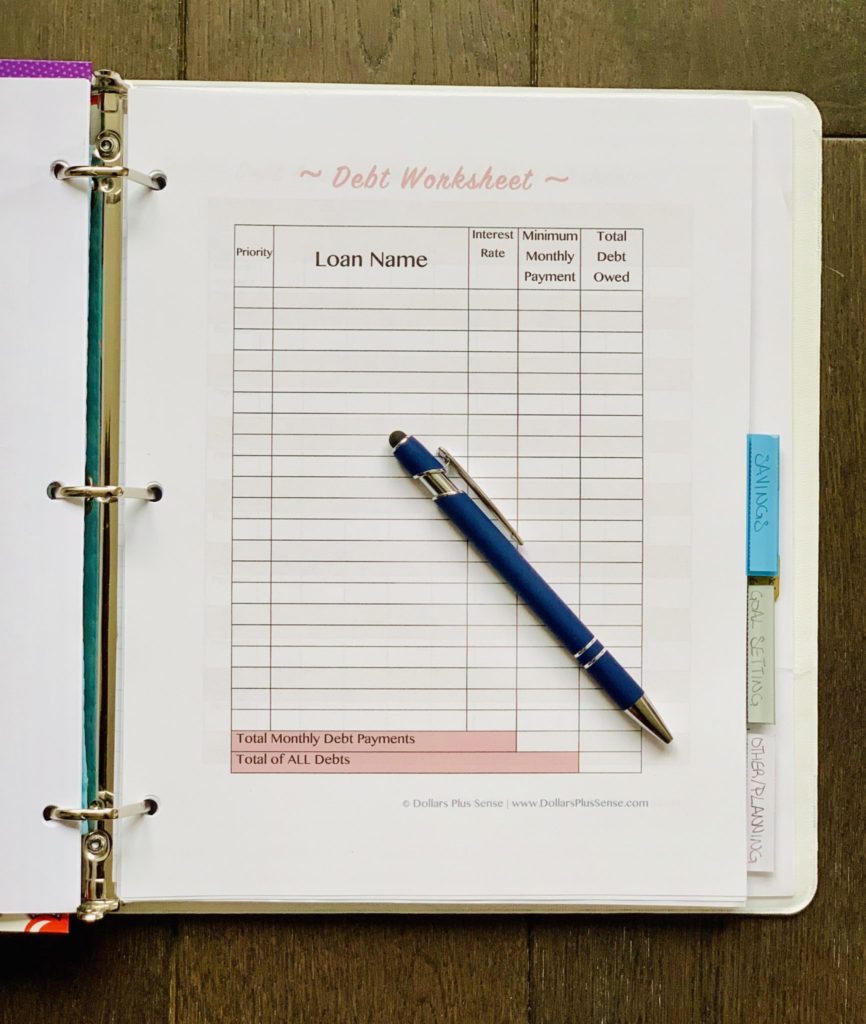

4. Not Making A Debt Repayment Plan

Debt is a drain on your finances and slows down your achievement of financial freedom or any other financial goals. That’s why not making a plan to pay off your debt quickly is one of the biggest financial mistakes you can make.

I recommend you pay your debts off from highest interest rate to lowest interest rate, regardless of the amount. This is because you will pay less interest if you pay off your highest-interest debt first. Use this FREE Debt Worksheet in my Resource Library to help you prioritize your debts.

You can use an app like Tally to pay down your debt faster. Tally is an automated debt manager that makes it easy to save money, manage your cards and pay down balances faster. It’s absolutely free to download, and they don’t charge any fees to use the app.

The way Tally works is they monitor your balances, APRs, and due dates on each credit card you register. Tally’s smart technology will determine which cards to pay first, based on factors such as APRs and utilization.

Finally, consider refinancing your high-interest debt. Right now, interest rates for loans are extremely low. So consider getting a personal loan at a lower interest to pay off your credit card debt, or refinancing your student loans at a lower rate. Now is a good time to look into refinancing your debt because you can potentially save a LOT of money.

5. Not Getting Cashback On Your Purchases

It’s too easy to get cashback nowadays with your purchases. So if you’re not taking advantage of that, you’re making a big financial mistake. Here are 4 of my favorite ways to get cashback on my everyday purchases:

- Rakuten is best for general online shopping. Every quarter they will send you a check or you can get paid through PayPal. When you sign up right now and purchase something through eBates you will get a $10.00 gift card and can choose from a few different stores.

- Ibotta can be used for online purchases, but it is the best for in-store purchases as well. You get paid via PayPal, Venmo, or you can buy a gift card with your earnings. If you sign up right now, you will get a $10 welcome bonus after your first purchase.

- Drop is a free cashback app that’s giving out millions in cash rewards for the spending you do every day. This is great if you do a lot of shopping from your cell phone. So you should definitely download the Drop app and save some money.

- Fetch Rewards app is a free grocery savings app that rewards you just for snapping pictures of your receipts. That’s really it. Free rewards no matter where you get your groceries (from big box stores, mom and pop corner shops, drugstores, liquor stores, and hardware stores – it’s all fair game).

Just scan your receipts and collect your rewards. Sign up for Fetch Rewards now and use code “APREWARDS” to redeem 3K points!

6. You’re Saving And Not Investing

Just saving your money alone is one of the biggest financial mistakes you can make — you have to invest your money so it can grow. Saving your money in a bank alone will take too long for it to grow, and you might even be losing money every year thanks to inflation.

Invest your money so that it makes more money. I like to invest in things that give me an income and increase in value. Therefore, I invest in things such as the stock market and real estate. Historically, the stock market and real estate have offered better returns on your money than if you were to save it in a bank account.

I personally use Robinhood to purchase individual stocks and ETFs. This website is great because you can buy and sell stocks for free—there are no commissions or fees. Most other brokerage firms charge at least a $4.95 fee per trade, and some have hidden fees.

Sign up today and you can get a free stock like Apple or Facebook. With Robinhood you also don’t need a minimum account balance, so you can get started right away.

If you are new to investing and relly have no clue what stocks to choose, I would recommend using a robo-advisor. A robo-advisor is an online automated advisor. They will invest your money for you based on your specific goals using computer algorithms.

Since robo-advisors are cheaper than what you would pay a human financial advisor, it is a great low-cost option for investing.

A great option to use if you’re just getting started is Acorns. I recommend Acorns for beginners because of its round-up feature. The way it works is you link your checking accounts and credit cards to Acorns and they will round every transaction up to the nearest dollar and invest it.

So let’s say you spent $9.17 at lunch. Acorns will round up that transaction to $10 and invest the $0.83. All your spare change starts to add up and before you know it you’re saving and investing. This is perfect for the person who also has trouble saving.

7. Not Valuing Your Time

Rich people value their time because they realize it’s the one thing none of us can ever get back. So when deciding how to pay (time or money) successful people usually choose to pay in money. The reason why they pay in money is because money is a renewable resource, whereas their time and effort they can NEVER get back.

You may be thinking to yourself “of course they pay with money because they have a lot of it.” But stop and think to yourself why they have a lot of money. Rich people will pay someone to do things like clean their house, cook their meals, and drive their car—not because they’re lazy, but because their time is so valuable. They use that time to make WAY more money than what they pay their cleaner, chef, or driver.

So if you’re not valuing your time and wasting it on tasks that won’t put you in a better place financially, you’re making a huge financial mistake. You are losing money by engaging in activities that are not productive or don’t produce money.

You should always take into consideration the value of your time. Always look at how much time and effort versus how much money it will cost you to complete a task. Also, stop wasting time trying to figure something out on your own when you can pay an expert. Since you know you have to pay either way, you should choose to pay in money.

8. You Don’t Ask For Help

Rich and successful people also have no problem hiring a professional. They don’t try to figure things out on their own that are not in their expertise—because they would waste too much time trying to do that. Successful people recognize that they don’t know everything, and they don’t mind asking for help.

This is usually in the form of some kind of professional advisor. The rich usually ask for help for anything they don’t know. That’s why they hire professionals like lawyers, accountants, and financial advisors. It would cost them too much time trying to figure out all the things that they don’t know—so they hire a professional for guidance.

You might not have a team of people you can hire to answer your questions like the rich, but the Internet can provide answers to some of your questions. Do a Google search, post your question in a forum, or buy a book on the topic you want to learn more about.

For example, when it comes to personal finance, there are so many resources out there. You can hire a personal coach or buy tools to help make managing your money so much easier. If you’ve been wasting a lot of time trying to figure things on your own, it’s probably time to ask a professional.

If you’re not asking for help, you’re making a big financial mistake. So don’t be afraid to invest in yourself and speed up the process of reaching your financial goals.

9. You Don’t Establish Other Streams Of Income

It is so important to have an additional source of income because it protects you in case one source “dries up.” A loss of income is the biggest threat to your financial future. Therefore you cannot rely on only one source of income — this is a financial mistake you can’t afford.

You can add other sources of income by:

- Finding a part-time job

- Starting a part-time business or side hustle

- Establishing passive income

If you want to learn more about increasing your streams of income, you can read my detailed article “5 Easy Ways To Increase Your Income Streams.”

10. Not Automatically Saving Money

If you want to achieve any financial goal, you need to be disciplined with saving. You should always “pay yourself first” and automate your savings. Paying yourself first means you put money in your savings account before you start to pay your other bills. When you automate your savings it makes saving easy.

Automating your savings makes it easier to save because you’ll never be tempted to skip saving. The money just goes into your savings account automatically before you can get a chance to spend it. If you’re not automatically saving your money, you’re making a big financial mistake.

You can automate your savings by setting reoccurring transfers to an online bank such as CIT Bank. CIT Bank is a good online bank to try because it:

- offers competitive interest rates (one of the nation’s top rates),

- has no monthly maintenance fees, and

- you only need $100 to open an account.

I recommend you use an online bank because it makes it harder for you to access your money (compared to a brick and mortar bank) in case you get tempted to spend it.

11. Not Being Organized

If you are not organized you are probably losing and spending more money than you need to. By not being organized you’re prone to higher interest rates, late fees, spending more money, and even fraud.

If you don’t know what’s going on with your finances, you almost certainly spend thoughtlessly. You often don’t look for the best deals because you’re doing last minute shopping and don’t have time to shop around.

Sometimes you might forget to pay your bills on time, which results in late fees and higher interest rates. You may even become a victim of fraud because you weren’t aware that someone hacked into your accounts.

It is extremely important to be organized to make sure you’re getting the best use of your money. I use this Personal Finance Binder to help me stay organized with my money. It allows me to see all my finances in one place so I can plan for any expenses that are coming up and track my financial progress.

You can read more about how to set up a personal finance binder in my article “Save More Money With The Ultimate Personal Finance Binder.”

12. Putting Off Saving For Retirement

One of the most common financial mistakes people make is they wait to start saving for retirement. This is a big mistake because you don’t get the benefit of compounding interest. Compounding is a powerful wealth-building tool because your interest gains interest.

The reason why you want to start saving for retirement as early as possible is the sooner you begin saving, the more time your money has to grow and compound. Let me give you an example to show you the power of compound interest.

Assume at the age of 35 you invest $1,000 that gives you an 8% return annually. To make the math easier, also assume you don’t add any more money to this account. When you are ready to withdraw from this account during your retirement years, let’s say at the age of 65, your $1,000 will be worth $10,063.

However, if you made the same deposit at the age of 25, and withdrew the money at 65, your $1,000 will be worth $21,725!! You would make more than DOUBLE the amount just by investing 10 years earlier.

So as you can see, saving for retirement (and starting early) is super important. If you’re not already doing so, you need to start saving for retirement as soon as possible.

Check out Personal Capital’s Retirement Planning Calculator. You should definitely use this free tool to map out your financial future. Simply link all your retirement accounts to Personal Capital so you can see all your accounts in one place and track your progress.

If you sign up today and link at least one of your investment accounts (with a balance of more than $1,000), you’ll get $50. That’s FREE money for keeping track and staying on top of your finances (something you should be doing anyway)!

13. Not Having Enough Insurance

Disasters can happen to anyone, even at no fault of your own. You’ve worked so hard to get what you have and you need to protect your assets. So if you don’t have enough insurance, you’re making a major financial mistake.

Your car or home can be damaged, someone sues you, a family member gets sick, you become disabled, or someone dies. In events such as this, you want to make sure you have enough insurance to protect you and your family.

You don’t want one of these disasters to be the reason you lose the financial empire you’ve built.

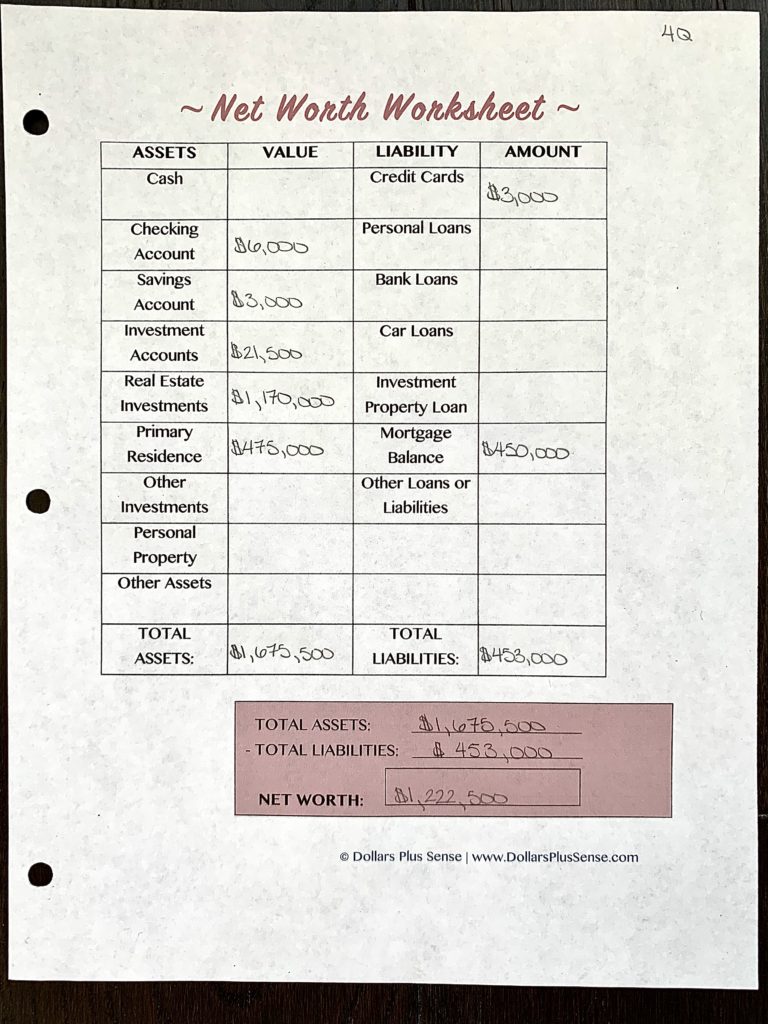

14. Not Calculating Your Net Worth

If you don’t know your net worth, you’re making one of the common financial mistakes. Knowing your net worth is extremely important when starting your financial journey. Calculating your net worth lets you see where your starting point is.

If you know where your starting point is, you can see how far you need to go to achieve your financial goal. If you know how far you need to go, you can make a better plan on how to achieve those goals.

In addition, knowing where you started lets you see if you have made any progress towards your goals. Calculate your net worth now, and recalculate it once or twice a year to check your progress. There’s nothing more motivating than seeing the progress you’re making towards your financial goals.

Calculating your net worth is a simple formula — subtract your liabilities from your assets.

Net Worth = What you OWN – What you OWE

You can find out your net worth quickly and easily with my FREE Net Worth Worksheet found in my Resource Library. My FREE Resource Library is loaded with more than 20 pages of easy to print worksheets, checklists, and money-saving tips.

15. You’re Not Putting Yourself First

I know, you’re a nice person and you love to help others. However, when it comes to your finances you should put yourself first. It’s like the instructions they give you when on an airplane “in case of an emergency make sure your oxygen mask is on first before trying to assist others.” It only makes sense because you can’t help others if you can’t breathe.

The same thing applies when it comes to your money. It is very important that you take care of your own financial security before helping family, friends, and others. If you don’t, you will soon need help yourself and won’t be able to help the people who rely on you.

16. Not Owning A Home

Did you know that homeowners have a net worth over 40x more than that of a renter? There are several reasons for that:

- Homeownership is a form of “forced savings.” Every time you pay your mortgage you are contributing to your net worth.

- Homeowners gain wealth through appreciation.

- The monthly cost of having a mortgage is fixed and does not go up over the years.

- There are a ton of tax benefits of owning a home.

Now, I know there are advantages to renting (I’m currently a renter) — such as the flexibility to move frequently and not having to do any repairs yourself — but there are more financial advantages to owning property over the long run. Because of this, I also own investment property although I rent.

17. You Pay Too Many Fees

One of the common financial mistakes people make is they pay too much in fees. A lot of us are diligent about making sure we don’t pay things like ATM fees, late fees on bills and credit cards, and checking account fees — that’s good. However, one of the places we neglect to pay attention to fees is our investment accounts.

Americans pay more than $600 billion in investment fees every year. Individually, we will lose about one-third of our retirement savings to fees. So I would contact your investment firm and have them explain exactly how much it’s costing you to manage your portfolio.

If you’re also investing outside your retirement account, I recommend you check out Robinhood. I personally use this platform to purchase individual stocks and ETFs. I love using Robinhood because there are no commissions or fees.

18. You Borrow Too Much Money

Unfortunately, we live in a consumer society. It’s too easy to get a credit card or approved for a mortgage that’s way more than you can afford. Because of this, a lot of people make the financial mistake of borrowing too much money.

When you have so much money at your disposal it makes it hard not to spend it. Therefore you find yourself drowning in debt. Don’t make the mistake of borrowing too much money just because you qualify for It.

19. Not Getting Educated About Your Finances

Getting and staying educated about your personal finances is so important. You are making a huge financial mistake if you don’t take the time to learn about money. You probably already see the value in getting educated, because you’re reading my blog right now.

Books

Some of my favorite personal finance books I think you should read are:

The Money Book for the Young, Fabulous, and Broke

This book by Suze Orman addresses financial problems for young people who may need help to dealing with finance issues and making a financial plan for the first time.

This book by Dave Ramsey is a complete guide to saving fund, saving for a rainy day, paying off your debt and reaching financial prosperity in your life. He is a big proponent of paying off ALL debt (yes, including mortgages) and debt free living.

Millions have read this book by George S. Clason. It discusses the keys to success when managing your money and financial advice told through ancient parables.

This book by David Bach will make you understand how much of your money goes to waste through the well-known “Latte Factor.” This book will help you identify where you unconsciously waste money and how those little expenses can add up to a huge financial loss. It will also show you how automation is the easiest and most effective way to build wealth.

This book by Thomas J. Stanley and William D. Danko identifies seven common traits of those who have accumulated wealth.

Most of the truly wealthy in this country don’t live in Beverly Hills or on Park Avenue-they live next door. They also don’t drive a fancy car or buy designer clothes. It shows that anyone can be a millionaire if you live below your means and invest well.

Since I think you should read, and read often, sign up for the FREE Kindle Reading App. Most books I’ve purchased are cheaper if you buy the Kindle version of it, instead of the paper version. You don’t need a Kindle E-Reader to access Kindle books. The Kindle app is available for iPhone, iPod Touch, Android, Windows Phone, Blackberry, Android Tablet, and iPad.

Also, consider signing up for a Kindle Unlimited Plan. It’s a subscription plan that gives you unlimited reading from over 1 million eBooks, and unlimited listening to thousands of audiobooks.

Most of the books I just recommended are free to read if you have a Kindle Unlimited Plan, or at a much lower cost. You can try it out for FREE your first month and see if it is valuable to you. If you don’t like, just cancel your subscription.

I have personally read 6 all of these books, so I highly recommend them.

Audiobooks

If you don’t have the time or don’t like to read, consider listening to audiobooks or podcasts. I listen to audiobooks and podcasts when I’m commuting to work or when I don’t have the time to sit down and read.

Try audible and get 2 FREE audiobooks. The first month is FREE and after that you pay a monthly subscription fee. With audible you get:

- 1 audiobook and 2 Audible Originals each month.

- Exclusive audio-guided fitness programs.

- Roll over any unused credits for up to 5 months.

- Easy exchanges—swap any audiobook you don’t love.

- Cancel anytime, your audiobooks are yours to keep.

So give audible a try, and if you don’t like it you can cancel and still get to keep your two free books!

20. Not Taking Care Of Your Credit Score

Having a good credit score can save you thousands of dollars in interest over your life. The better your score, the better the rate of interest you’re offered when you borrow money for things like cars, homes, and personal loans.

Make sure you’re checking your credit score regularly. Don’t pay for your credit report because you’re entitled to one free report every twelve months from each of the three major reporting agencies. Because the reports can differ due to errors, it’s a good idea to order all three.

21. Not Checking Your Progress Regularly

Finally, the last of the financial mistakes to avoid is not checking your progress regularly. I think it’s very important to check your progress regularly during your financial journey.

Checking your progress allows you to see if you are moving at the pace you planned, or if you need to make some adjustments. You will also stay motivated when you see progress is being made.

Remember, people who identify their goals and work towards them usually accomplish their goals and accomplish them quicker. So, make sure to periodically check your financial progress.

How Do You Recover From A Financial Mistake?

After reading this article, you might have identified some financial mistakes you’re making. So you might be wondering “how do I recover from a financial mistake?” If you made any of these common financial mistakes, this is what you should do moving forward:

- Accept the setback, let go of it, and commit to moving forward.

- Make a financial goal and develop your plan.

- Take action on your plan.

You can also look into getting professional help to help you make a plan to get back on the right track. Sign up for a FREE 15-minute consultation to learn more about how I work with my clients!

Summary

As you can see, there are many financial mistakes that people commonly make. If you avoid these mistakes you will save more money in the long run, and speed up your progress towards your financial goals.

Related Articles:

- The Secret To Wealth Creation (That You Didn’t Know)

- How To Accomplish Your Financial Goals

- Net Worth By Age: How Do You Compare?

If you want to remember this article, post it to your favorite Pinterest board.

3 Comments on 21 Worst Financial Mistakes To Avoid (And Actionable Tips)