Do you have a ton of financial goals you’re trying to accomplish at once? Having multiple financial goals all at once can get overwhelming. Find out the best way to prioritize your financial goals so that you can achieve financial freedom quicker.

Jump Ahead To:

What Are Financial Goals?

Financial goals are the things you hope to achieve with your money. They aren’t one size fits all, because everyone has different hopes and priorities when it comes to their money. However, if you don’t set your financial goals, you’ll probably stay stuck in the same place financially.

What Are Good Financial Goals?

It’s hard to say what a “good” financial goal is because everyone is in different stages of their financial life. So I would just say a good financial goal is one that puts you in a better position to have more wealth than you had before.

Why Are Financial Goals Important?

Having financial goals are important because people who make goals usually achieve them, and achieve them much faster than those who do not set any financial goals. The reason for that is because goals give you more focus, allows you to track your progress, and help you stay motivated to achieve your task.

For example, say your goal is to save for a house. You might cut back on your shopping trips and use that money you save to put towards your house fund instead. Without establishing that goal, you’re more likely to continue spending as usual without putting anything towards savings.

So in other words, having financial goals help influence your actions today to ensure you have a better financial future tomorrow.

Examples Of Financial Goals

Here are some examples of financial goals to help inspire you set some goals of your own:

- Create And Stick To A Budget

- Increase My Net Worth

- Save At Least 10% Of My Income

- Have A Fully Funded Emergency Fund

- Buy A House

- Develop At Least One Stream Of Passive Income

- Make More Money Than I Did Last Year

- Pay Off At Least One Of My Credit Cards

- Spend Less Money Than I Did Last Year

- Increase My Credit Score

- Break Bad Spending Habits

- Increase or Start Investing

- Pay For My Wedding In Cash

- Save For My Vacation To Jamaica

- Start A Business

This list is just to help give you ideas, so think about what’s important to you as you begin to set your goals. It’s completely normal to have several goals, and for them to change over time.

3 Different Types Of Financial Goals

1. Short-Term Financial Goals

Short-term financial goals are usually goals you wish to accomplish in less than 3 years. Some common examples of short-term goals are building your emergency fund, paying down high-interest debt, or saving for a wedding or vacation.

2. Mid-Term Financial Goals

Medium-term financial goals usually take about 3-10 years to achieve. Some examples of mid-term financial goals may be saving to buy a car, saving for a down payment on a house, or paying off your high-interest debt.

3. Long-Term Financial Goals

Long-term goals usually take more than 10 years to achieve. Some examples of long-term goals may be saving for retirement, saving for your child’s college tuition, or paying off a mortgage.

How Do You Write Financial Goals?

It is important to write down your financial goals. But there’s a specific way to do it to be successful and actually accomplish what you want. You can’t just say, “I want to (fill in the blank)” and expect it to happen.

So, start by making a list of all the things you hope to accomplish, but make sure your goals are SMART. SMART stands for: Specific, Measurable, Achievable, Relevant, and Timely.

SMART Goals:

- You want to make your goals as specific as possible;

- Measurable so that you can track your progress and know when you’ve achieved your goal;

- You want to make your goals realistic and achievable;

- Your goals should be relevant to your overall plans in life; and

- Finally, you want your goal to have a time limit where you set an end date to achieve your goal.

By making your goals SMART, it pushes you further to get really specific, gives you a sense of direction, and helps you actually reach your goals.

How To Save For Different Financial Goals

Start by listing all of your financial goals. Next, determine how much money you will need to achieve each goal and when do you want to accomplish these goals.

Next, categorize each goal as a short-term, medium-term, or long-term goal. Keeping your timeline in mind, you can use the following saving strategies for each of your goals:

Saving For Short-Term Goals

Short-term goals take no more than 3 years to achieve.

For short-term goals, I recommend you put your money in a savings, money market account, or a CD. In a short period of time, the amount you save is much more important than the interest rate you earn.

For short-term goals, you need to make sure that your money will be there when you need it, so play it safe and keep it in a bank account.

Saving For Medium-Term Goals

Mid-term goals take approximately 3-10 years to achieve.

For mid-term goals, it is a little more difficult to determine where to put your money. If your mid-term goal is closer to the short-term end of the spectrum, like 3-5 years, I would be more conservative and invest in CDs, money market funds, and bond index funds.

If your mid-term goal is closer to the long-term end of the spectrum like 6 years or more, I would invest more in stock index funds and balanced mutual funds.

Saving For Long-Term Goals

Long-term goals usually take more than 10 years to achieve.

Since your long-term goals are more than 10 years away, you can take on more risk and invest more heavily in the stock market or real estate.

The reason why you can take on more risk with your long-term goals is that you have time on your side. If we have a temporary dip in the market, the odds are you are likely to see that investment recover and make money over a long period of time.

I personally use Robinhood.com to purchase individual stocks and ETFs. This website is great because you can buy and sell stocks for free—there are no commissions or fees.

Most other brokerage firms charge at least a $4.95 fee per trade, and some have hidden fees.

Sign up today, and you can get a free stock like Apple or Facebook. With Robinhood, you also don’t need a minimum account balance, so you can get started right away.

If you are new to investing, I would recommend using a robo-advisor. A robo-advisor is an online automated advisor. They will invest your money for you based on your specific goals using computer algorithms.

Since robo-advisors are cheaper than what you would pay a human financial advisor, it is a great low-cost option for investing.

A great option to use if you’re just getting started is Acorns. I recommend Acorns for beginners because of its round-up feature. The way it works is you link your checking accounts and credit cards to Acorns, and they will round every transaction up to the nearest dollar and invest it.

So let’s say you spent $8.17 at lunch. Acorns will round up that transaction to $9 and invest the $0.83. All your spare change starts to add up, and before you know it, you’re saving and investing. This is perfect for the person who also has trouble saving.

- Related Article: Best Ways To Invest In The Stock Market For Beginners

Historically, stocks and real estate have been consistent long-term winners. You don’t want to only invest in safer investments (such as CDs, bonds, etc.) for the long-term because your money will not grow fast enough to accomplish your financial goals.

As a general rule, when saving for your different financial goals, the shorter your goal timeline, the less risk you can take; the longer your goal timeline, the more risk you can take.

How To Prioritize My Financial Goals?

Okay, so I know you probably have a TON of goals you would like to achieve, but you can’t try to achieve everything all at once. You have to decide what is MOST important to you.

When you first start your financial journey and set your various SMART financial goals, you might have a hard time deciding what’s most important to you. It may feel like everything is equally as important. So, here is the order I think you should prioritize your financial goals:

1. Make A Budget

Before trying to achieve any of your other financial goals, it is crucial that you have a functioning budget first. Creating a budget can help you feel more in control of your finances and let you save money for your financial goals. If you want to improve your finances, the first thing you need to do is know where your money is going.

If you’re just getting started with making a budget, you can use this FREE Monthly Budget Printable.

If you want something a little more advanced, I personally use these budget templates every month to track my spending. It is the system I’m currently using for my budget, and it has helped me save over 50% of my income every month.

You can read my detailed article “How To Use A Monthly and Yearly Household Budget Spreadsheet” to learn more about how to set up a budget that actually works.

2. Build An Emergency Fund

Once you have a solid budget in place, I would focus on building an emergency fund.

An emergency fund is money set aside to cover large unexpected expenses or to help you through hard financial times—like a job loss. This is a hard lesson everyone should’ve learned with the recent government shutdown and coronavirus pandemic.

Preparing for the unexpected is necessary if you want to meet your other financial goals. You don’t want to make progress with your other financial goals, and then get thrown off by an emergency.

You should have enough cash available to help you through hard financial times or emergencies without having to rely on credit cards or take out other high-interest loans.

- Related Article: How To Build An Emergency Fund

How Much To Put In Your Emergency Fund

I recommend saving 3 months’ worth of living expenses if you have relatively strong job security. If you have some instability in your employment or if finding another job could take you a long time, I recommend 6 months (or more).

What I mean when I say “living expenses” is the necessities (not luxuries like dining out and entertainment). However, no matter what your job situation is, I think everyone should have at least $1,000 set aside in case of an emergency.

Once you decide how much you want in your emergency fund, set a monthly savings goal. Next, automate your savings by setting recurring transfers to your bank. Once you have established a suitable size emergency fund, you can feel more secure knowing you are prepared for the unexpected.

I recommend you use an online bank to hold your emergency fund because it makes it harder for you to access your money (compared to a brick-and-mortar bank) in case you get tempted to spend it.

Automating your savings makes it easier to save because you’ll never be tempted to skip saving. The money just goes into your savings account automatically before you can get a chance to spend it.

3. Pay Off High-Interest Debt

Once you have at least $1,000 in your emergency fund, you can focus on paying off high-interest debt. Debt is a drain on your finances and slows down your achievement of financial freedom or any other financial goals.

I recommend you pay your debts off from the highest interest rate to the lowest interest rate, regardless of the amount. This is because you will pay less interest if you pay off your highest-interest debt first.

Speed Up Paying Off Your Debt

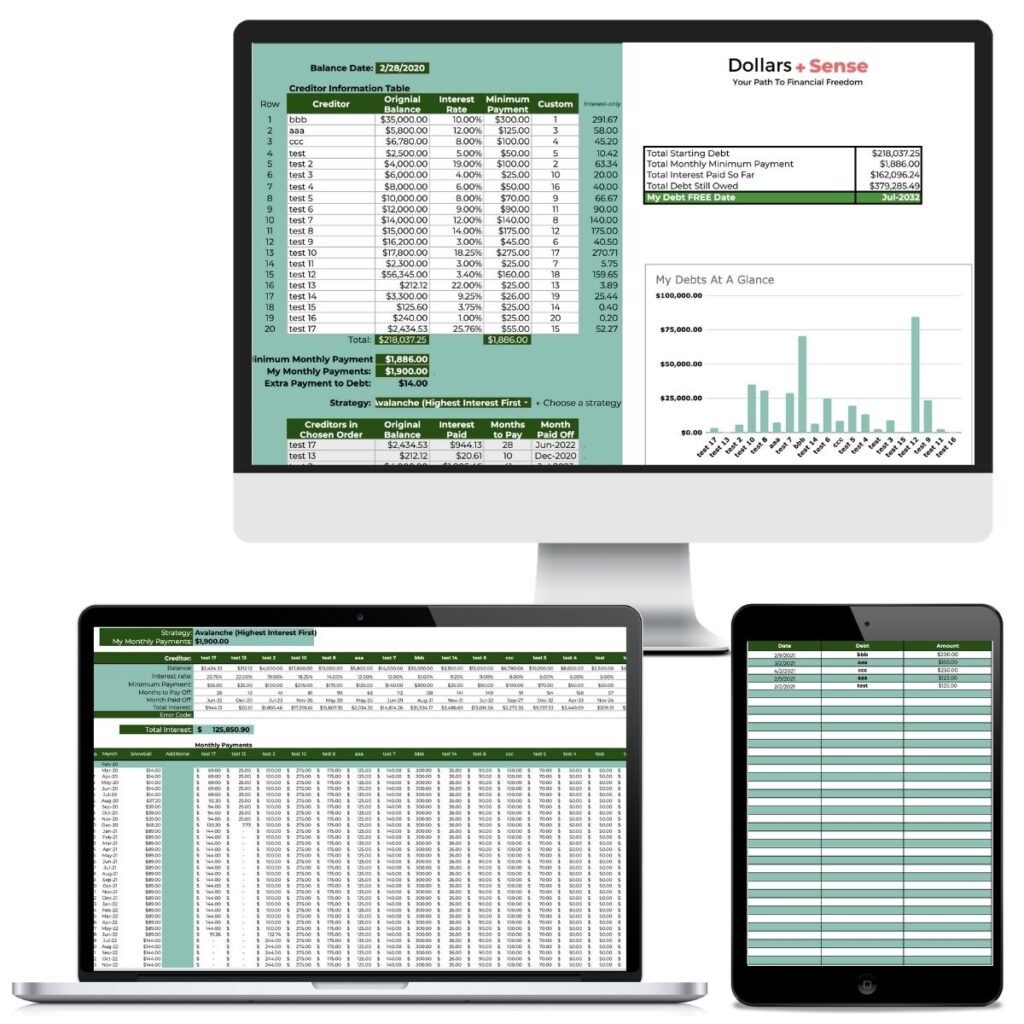

Once you have a debt repayment plan, you can use the Debt Payoff Spreadsheet to pay down your debt faster. This spreadsheet will help you create a fully custom debt payoff plan that keeps you motivated…so you can get out of debt and STAY OUT of debt forever.

The Debt Payoff Spreadsheet also easily calculates your debt-free date with just the click of a button. With this spreadsheet, you will have a clear roadmap to follow that will get you out of debt faster than you ever thought possible.

The way it works is with this spreadsheet, you can easily create a debt repayment plan based on the popular debt snowball method (paying the lowest balance first), the debt avalanche method (paying the highest-interest first), or experiment with your own custom strategy.

4. Save For Retirement

I want to start off by saying anyone who is in a position to both pay off debt and fund their retirement plan should do so. As the generation of baby boomers enters retirement, the payroll taxes that they’ve contributed to the system throughout their careers will turn to withdrawals in the form of retirement benefits.

The amount of money that has been set aside is not enough to cover the long-term expenses of baby boomers that will occur. As a result, it is estimated that Social Security will run out of money by 2034.

That’s just in time for people around my age to get ZERO when we decide to retire. Therefore, it is imperative that you save for your own retirement and not expect to rely on the government.

Take Advantage Of Your Employer Match

Saving for retirement is extremely important, and you want to start saving as soon as possible. Regardless of your debt, you should contribute the maximum amount your employer matches to your 401(k) or similar plan. If you don’t, you’re leaving FREE money on the table!

For example, if your employer will match 50% of your contributions up to 6% of your pay—which is a typical arrangement—then you should contribute 6% to max out the employer match.

That means if you have a salary of $50,000, you will need to contribute $3,000 (6%) to get your employer’s maximum contribution of $1,500 (3%).

Take Advantage Of The Power Of Compounding

You need to start saving for retirement as soon as possible. The reason why you want to start saving for retirement as early as possible is that the sooner you begin saving, the more time your money has to grow and compound.

Compounding is a powerful wealth-building tool because your interest gains interest.

For example, say you have $1,000 invested that gains 10% interest. At the end of the year, you will earn $100 in interest and have a total of $1,100. If you don’t touch that money and allow your interest to compound, you will earn 10% on $1,100 (not $1,000); therefore, at the end of year two, you will earn $110 in interest.

Let me give you another example to show you the power of compound interest.

Assume that at the age of 35, you invest $1,000, which gives you an 8% return annually. To make the math easier, also assume you don’t add any more money to this account. When you are ready to withdraw from this account during your retirement years, let’s say at the age of 65, your $1,000 will be worth $10,063.

However, if you made the same deposit at the age of 25 and withdrew the money at 65, your $1,000 will be worth $21,725!! You would make more than DOUBLE the amount just by investing 10 years earlier.

So as you can see, saving for retirement (and starting early) is super important. Try to put something towards retirement (especially if your employer is willing to match any contributions), even if you’re paying down high-interest debt.

I think paying off high-interest debt trumps saving for retirement (except for the cases where you have an employer match)—so most of your money should go towards paying off high-interest debt. Once you’ve paid off your high-interest debt, take all that extra money and try to catch up with your retirement savings.

5. Save For Other Financial Goals

Finally, once you have an emergency fund, paid off your high-interest debt, and started saving for retirement, you can focus your energy on some of your other long-term financial goals.

Some of your other long-term financial goals might be buying a house, investing outside of your retirement account, or paying for your children’s education.

At this point, you should have a solid financial foundation and can work towards building wealth. I wouldn’t prioritize any other financial goals before having an emergency fund, getting rid of high-interest debt, or saving for retirement.

How To Make Time To Do It All?

Now that you have made your SMART goals and decided how to prioritize your financial goals, you may be wondering how you will ever get everything done. I know firsthand that it takes time to put together a budget that WORKS and to make a plan to pay off debt.

On top of that, you need to figure out how much to contribute towards retirement and your other financial goals. Sometimes it may be very overwhelming, and you feel like giving up. But trust me, you can push through and accomplish your dreams.

So, how are you going to be able to do it all and achieve your financial goals? By becoming more organized and increasing your productivity.

Being more organized and productive allows you to make the most of the hours in your day. You will have more time to keep track of your finances and your progress. It will also allow you to have more time to focus on earning extra money if you choose.

If you struggle with getting everything done in a day, I recommend you download this FREE Daily Goal Planner. It will help you make a simple To-Do List and prioritize your goals for the day.

Another resource that I found to be very helpful is my Financial Goal Planner. The Financial Goal Planner is a carefully curated planner filled with printables to help you make a plan for financial success and crush your financial goals.

With this planner, you can set up your budget, save more money, and make a clear plan to get out of debt faster than you ever thought possible. This goal planner has everything you need to be productive, manage your time wisely, organize your finances, and set money goals.

I highly recommend you check out the Financial Goal Planner because the value is AMAZING, and it has made a difference in my life! You will save money because you never have to buy another planner again. Keep the files for life and reprint the pages you need—or keep it in the digital format and use it with a note-taking app as I do.

Having an action plan in place allowed me to be financially free in 6 short years (I initially thought it was going to take me 15 years—so I was able to meet my goal in less than HALF the time).

How To Track Your Financial Progress

It is so important to track your financial progress so you can analyze what actions are successful and what actions need improvement. Here are the 3 things you should be doing to track your progress and see if you’re getting closer to your financial goals:

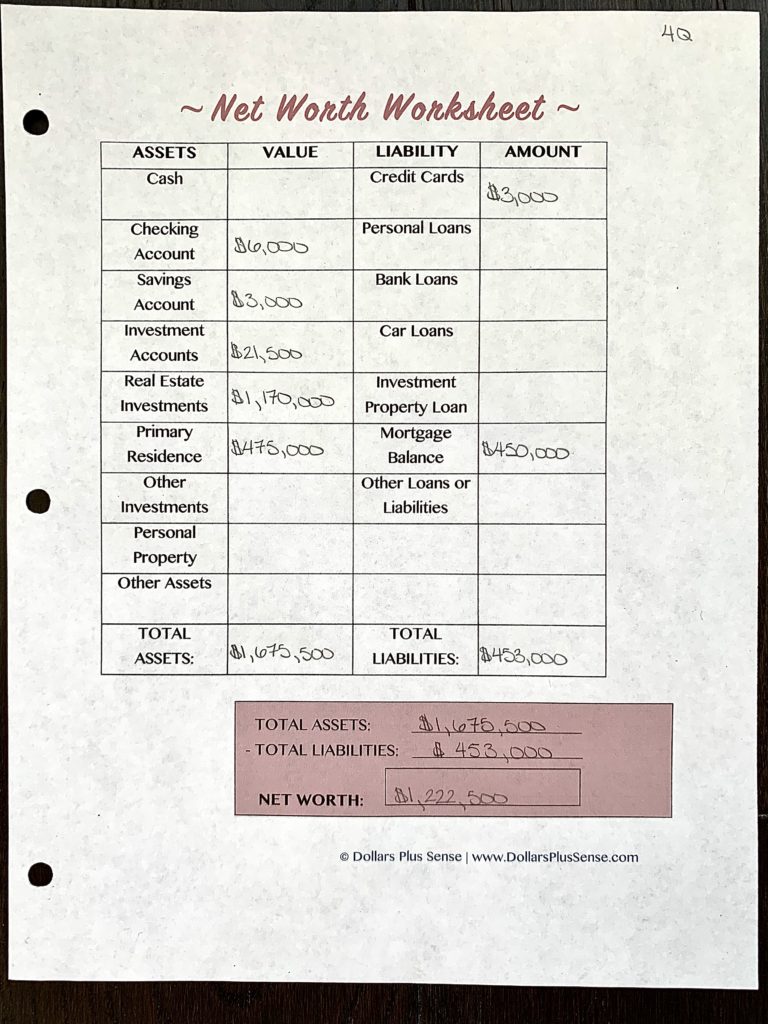

1. Calculate Your Net Worth

You want to start by calculating your net worth. Your net worth is simply your assets (everything you own) minus your liabilities (everything you owe).

Net Worth = Assets – Liabilities

By calculating your net worth first, you can see where your starting point is, and it helps you track your financial progress.

Use my Net Worth Worksheet to get started.

Once you know what your net worth is, you know how far you need to go to achieve your financial goals. Knowing how far you need to go on your financial journey also helps you plan on how to achieve those goals.

Don’t be afraid to find out what your net worth is, or be disappointed by the number. I started with a negative net worth (6-figures worth of debt to be specific), but I used this as motivation.

I got serious and made a plan to turn my financial situation around. Then I worked every day towards my goal. So I want you to use the number on your Net Worth Worksheet as motivation and start working towards your goal today.

2. Check Your Spending

The next thing you should be doing to track your financial progress is monitoring your spending.

I recommend you use a website like Empower to see all your accounts and spending in one place. Empower is a FREE online platform where you can link all of your accounts (i.e. – bank accounts, loans, credit cards, investment accounts) to monitor your income and expenses.

After you link all your accounts, you can see all your accounts in one place to have better money oversight. I like to visit Empower at least once a week to make sure there are no unauthorized transactions in my bank accounts or on my credit cards.

Since I use Empower as a way to track my spending, I also visit to log any cash spending I may have done. At the end of the month, I take my spending information from Empower and plug it into my Monthly Budget Template to see how I did that month.

I compare what my budgeted spending was versus what my actual spending was. If my actual spending was over my budget, I will make the necessary adjustments to improve my progress next month.

If you sign up with Empower today and link at least one of your investment accounts (with a balance of more than $1,000), we’ll each get $50. That’s FREE money for keeping track and staying on top of your finances (something you should be doing anyway)!

Another great FREE tool is Empower’s Retirement Planning Calculator. You should definitely use this tool to map out your financial future. Simply link all your retirement accounts to Empower so you can see all your accounts in one place and track your progress.

3. Have Quarterly Reviews Of Your Finances

You shouldn’t stop at just checking your monthly spending, you should also have quarterly reviews. During your quarterly reviews, you should analyze your data to see if you’re on schedule to accomplish your financial goals.

The way I personally do my quarterly reviews is I take the numbers from my Monthly Budget and plug them into my Yearly Budget Template. This allows me to compare my progress from one month to the other.

Finally, you should recalculate your net worth every year to see if your overall net worth has grown. Revisit your Net Worth Worksheet from last year, and compare it to your numbers this year.

Did you pay down your debt? Have your investments grown? Did you purchase more assets? By reviewing your finances periodically and answering these questions, you’re able to determine if you’re making any financial progress.

Summary

Now that you know how to prioritize your financial goals, the one thing I want you to take away is that you can’t accomplish everything all at once. I’m not saying you can’t save for multiple goals at the same time, but you definitely have to prioritize what means the most to you. Put more of your resources towards the goals that matter the most.

The order I recommend you prioritize your financial goals is:

- Make a budget;

- Build an emergency fund;

- Pay off high-interest debt;

- Save for retirement; and

- Save for other financial goals.

Focus most of your energy and resources on your main goal, and work your way down. Get organized so you can be more productive and accomplish your goals faster. Finally, make sure you’re keeping track of your financial progress.

Related Articles:

- How To Accomplish Your Financial Goals

- How To Be Productive At Work Without Burn Out

- 5 Ways To Be More Productive: The Ultimate Productivity Bundle

If you want to remember this article, post it to your favorite Pinterest board.

6 Comments on The Best Way To Prioritize And Achieve Your Financial Goals