Curious about the 50/20/30 budget rule and how it works? Find out if the 50/20/30 budget is a good strategy to help you budget your money better.

Jump Ahead To:

What Is The 50/20/30 Budget Rule?

The 50/20/30 budget rule is a simpler way to budget that doesn’t involve a lot of detailed budgeting categories. Instead, you spend 50% of your income (after tax) on needs, 20% on savings or paying off debt, and 30% on wants.

The 50/20/30 budget rule was first made famous by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi. They co-authored a book called All Your Worth: The Ultimate Lifetime Money Plan, where they go into more detail about this budgeting method.

In essence, the 50/20/30 budget rule is very similar to a reverse budget where the emphasis is on saving first and doing what you want with the money that’s left.

What Is A Reverse Budget?

A reverse budget is where you build your spending plan AFTER you have set aside money for saving. You pay yourself first, and what’s left over, you can spend on your expenses. Once you set up your spending plan, you don’t have to track your spending or allocate where your money is going.

A reverse budget, or a 50/20/30 budget, is excellent for people who hate budgeting. You don’t have to track your spending and can spend as you like once your savings requirement is met.

The only difference between a 50/20/30 budget and a reverse budget is the 50/20/30 budget breaks down how much should go to wants, needs, and savings. Whereas the reverse budget only specifies how much money should go to savings—how you spend the rest of your income is up to you.

How To Use The 50/20/30 Budget Rule

The 50/20/30 budget rule is perfect for those who hate budgeting. Once you set up your spending plan and put aside money for savings, you don’t have to allocate in detail where your money is going. The breakdown of your after-tax income is 50% to needs, 20% to savings or paying off debt, and 30% to wants.

50% To Necessities

According to the 50/20/30 budget, 50% of your after-tax money should go to your necessities. Necessities include things such as food, housing, utilities, basic transportation, and so forth.

If you live in an expensive city like me, where housing alone may take up 50% of your income, you need to reduce your housing expenses or other necessities.

If you can’t reduce your housing expenses or other necessities, reduce the percentage of your wants. But whatever you do, try not to reduce your savings and debt repayment percentage.

20% To Savings and Debt Repayment

Next, 20% of your after-tax money should go to your savings or debt repayment. To make saving simple, automate your savings and “pay yourself first” before you pay your bills. When people save first, they have less money to spend, and tend to use the remainder on things they need.

This is because the money is just not easily available to spend. So you should automatically transfer 20% of your paycheck to an online savings or retirement account.

I recommend you use an online bank because it makes it harder for you to access your money (compared to a brick-and-mortar bank) in case you get tempted to spend it.

Automating your savings makes it easier to save because you’ll never be tempted to skip saving. The money just goes into your savings account automatically before you can get a chance to spend it.

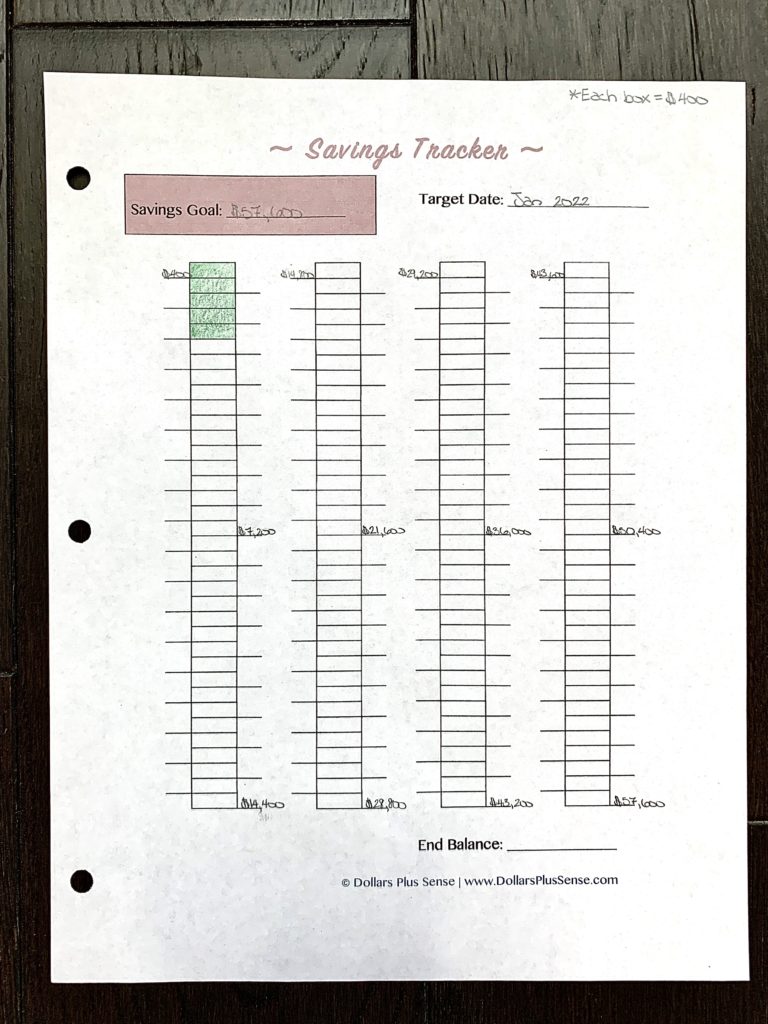

If you would like a fun way to track your savings, download this Savings Tracker. I love this tool because I’m a visual person, and I stay motivated when I can see the progress I make.

Here’s an example of how I use the Savings Tracker below:

Saving vs. Debt: Which Should I Do First?

If you don’t have money set aside for emergencies, you need to focus on saving first. I recommend you have at least $1,000 saved before you even think about paying off your debt.

If you do not have an emergency fund that is fully funded yet, I would only pay the minimum balance on my debt and put the remainder of the 20% toward funding my emergency fund.

Ideally, you should have 3-6 months’ worth of living expenses in your emergency fund. You should have 3 months’ worth of living expenses if you have relatively strong job security. You should have 6months (or more) if you have some instability in your employment or if finding another job could take you a long time.

When I say “living expenses,” I mean only necessities, such as rent and groceries—I don’t mean shopping, entertainment, dining out, or vacations. If you are ever in a situation where you lose your job, so you have to rely on your emergency fund, you shouldn’t be taking vacations or dining out anyway.

You can read more about figuring out how much you need in your emergency fund, and how to set it up in my article “How To Build An Emergency Fund.”

Once you have your emergency fund established and fully funded, you can then put the entire 20% to debt repayment. I would first focus on only paying off high-interest debt (interest rate higher than 8%). Once you have paid off your high-interest debt, you can either:

- Save and invest the entire 20%, or

- Split 10% to go towards low-interest debt and 10% to saving and investing.

In my opinion, I would save and invest the entire 20% if the rate of return on your investment is higher than your debt interest rate.

In other words, if you invest your money in the stock market, and get on average a 6% return on your money, but your mortgage interest rate is 4%, I personally would not rush to pay off my mortgage. I would continue to invest because I am getting a higher return on my money.

But that’s a decision for you to make for yourself. Some people hate debt no matter the interest rate, and just want to get rid of it no matter what—and that’s okay.

- Related Article: Paying Debt Vs. Saving: Which Is Best?

30% To Wants

Finally, under the 50/20/30 budget, 30% of your after-tax income should go towards your wants. Wants included things like entertainment, vacation travel, dining out, clothing beyond the essentials, cable, internet, etc. The remainder 30% of your income should go towards things in this category.

You MUST Do This If You Hate Budgeting

If you want your 50/20/30 budget or your reverse budget to work, you cannot spend money that you don’t have. Do not rely on your credit cards to make up for any overspending.

If you save first, but then use your credit cards to “make up the difference,” then you’re not truly saving as much as you think you are, and the whole system will collapse. If you have trouble with overspending, try only using cash.

- Related Article: How To Use The Cash Envelope Method

I personally think nothing is better than tracking your spending in a monthly budget, but this method is a good alternative for people who hate budgeting.

A 50/20/30 budget doesn’t require you to categorize every expense or keep a detailed record of your spending. It will also ensure that you’re saving some of your income. So, just make a decision about how much you’re going to save every month and stick to it.

Summary

In summary, if you hate budgeting and tracking your spending, try the 50/20/30 budget. With this method, 20% of your monthly after-tax income goes to savings, 50% to necessities, and 30% to wants. Automate your savings so you’re not tempted to spend it.

Finally, if you decide to use this method, you need to stay with it and don’t rely on credit cards to make up for any overspending.

Related Articles:

- 17 Reasons Why Your Budget Doesn’t Work

- How To Choose The Right Budgeting Method

- How To Save 50 Percent Of Your Income

If you want to remember this article, pin it to your favorite Pinterest board.

Want more help with this? The Budget Starter Toolkit picks up right where this post leaves off. Prefer to start free? The Printable Budget Binder has you covered.

3 Comments on What Is The 50/20/30 Budget Rule And How Does It Work?