Almost 70% of Americans don’t have a detailed household budget according to a Gallup study. If you want to see different results with your money, you need know how to make a budget. Find out how to make a budget worksheet for beginners in 5 easy steps.

Jump Ahead To:

How Do You Create A Budget For A Beginner?

Making a budget when starting your financial journey can seem really intimidating. If this is your first time trying to create a budget, you can make a budget using these 5 simple steps:

- Determine your net income (take-home pay)

- Determine your monthly expenses

- Determine how much you want to allocate to each spending category

- Track and review your spending

- Make adjustments where necessary.

So let’s go over each step in more detail so you know exactly what to do…

FREE Printable Budget Worksheet For Beginners (Monthly Budget Worksheet PDF)

Before we get started with making your budget, I want you to download this FREE Monthly Budget Worksheet. This free printable monthly budget pdf will make it much easier for you to make a budget as a beginner.

How Do You Fill Out A Budget Worksheet?

Now that you have your free Monthly Budget Worksheet, let’s go over how you fill out a budget worksheet.

Step 1: Determine Your Net Income (Take Home Pay)

First, you need to determine how much money you take home every month after taxes. If you have automatic deductions from your paycheck, add those back to your net income.

For example, add deductions for a 401(k) or other retirement accounts, savings, or health and life insurance. Adding those deductions back gives you a true picture of your savings and spending.

If you have earned income from an employer where taxes are automatically deducted, this is easy to establish. However, if you have other types of income—such as self-employment or other outside sources of income—be sure to subtract obligations to determine your take-home pay.

For example, you want to subtract things like taxes and business expenses.

Your final take-home pay is called net income, and that is the number you should use when creating a budget.

Step 2: Determine Your Monthly Expenses

The next step to making a budget worksheet for beginners is you need to determine your monthly expenses.

Write down a list of all your expected expenses for the month. If you are not sure what your expenses are, start by looking at where you spent money in the past three months.

You can find this information by reviewing your past credit card and bank statements, or a third-party website like Empower.

I like using Empower because once you set it up, you can see all of your spending in one place (instead of having to log into multiple websites). Unfortunately, you will not be able to account for the areas where you spent cash. However, it will provide you with a rough outline of your spending.

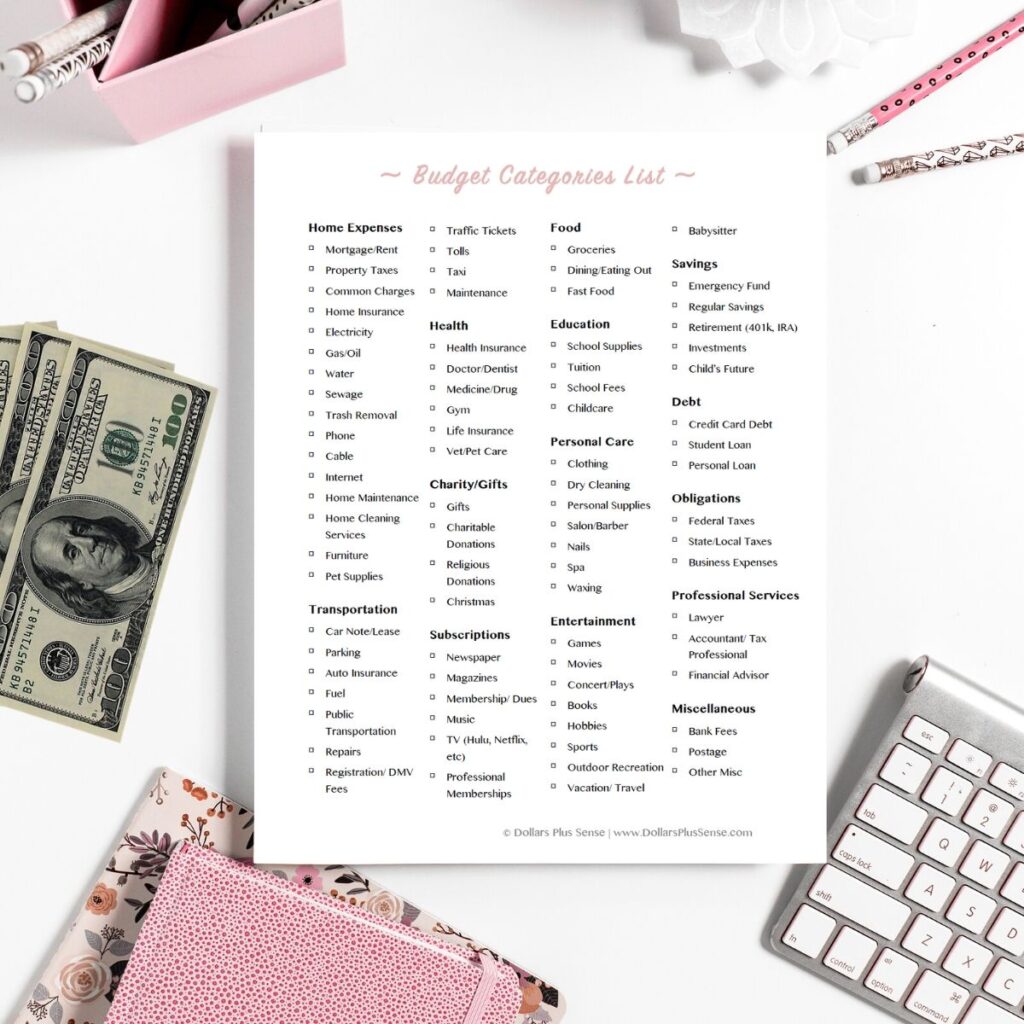

You can download this list of over 80 budget subcategories to make sure you include everything in your budget. A lot of people often go wrong when making a budget because they accidentally leave out categories that will require money at some point. That can throw your whole budget off.

This list is designed to cover as many personal budget categories as possible. Don’t get overwhelmed by this list, because not every category will apply to you. Go through the checklist, and put a check next to each item you spend money on. Then include those categories in your budget.

Once you make your list, start writing how much you normally spend in that area. Unfortunately, you will not be able to account for the areas where you spent cash. However, it will provide you with a rough outline of your spending.

If there are any spending categories that you can’t figure out how much you spent, just take a guess of what you think you spent. Make sure to include a “miscellaneous” category as a catch-all for any expenses you may have forgotten to list.

Be prepared to devote some time to this task. It can be very tedious, but it’s important not to skip this step. This is the foundation of making a real budget that will work. The good news is that once you do this, you rarely have to do this again because you usually spend money in the same categories every month.

Step 3: Determine How Much Of Your Money You Want To Allocate To Each Spending Category

After establishing your monthly income and expenses, hopefully, the end result shows more income than expenses. If you are showing a higher expense column than income, you need to make some changes.

Start by determining your short-term financial goals. For example, do you want to cut spending, pay down debt, or save more? What are your priorities?

After you have done that, start determining how much money you can allocate to each spending category. Lastly, figure out where you can cut back so that you have money to put towards your goals.

If you’re having a hard time figuring out how much you should be spending in each expense category, read my article “How Much Should I Be Spending?” This article will give you a general idea of how much of your income you should allocate to each spending area.

Step 4: Track and Review Your Spending

Once you have your budget worksheet set up, it’s essential to review your budget on a regular basis to make sure you are staying on track. You can use this FREE Daily Expense Tracker to help you with that.

I personally recommend recording your spending every day, or at the very least, once a week. Print out multiple sheets of your Daily Expense Tracker (one for each spending category or sub-category). Then put all your sheets in one place (like a binder or folder).

If you track your spending every day, you should write down what you spend as you go. Make a note on your phone or on a small piece of paper as you spend throughout the day. Then write the numbers in your expense tracker at the end of the day.

If you decide to track your spending every week instead, you can go online to your credit card, bank’s website, or a third-party website like Empower to see your spending for the week. You can then write down those transactions in your daily expense tracker.

Remember to also keep track of any cash you may have spent, since this will not be on your bank statements.

If the hardest part of budgeting for you is tracking your spending, read my detailed article “3 Ways To Track Your Spending When You HATE Tracking Your Spending.” I personally use the first tip in this article because I don’t like tracking my spending either.

Once you have recorded your spending for the month, plug in the numbers from your daily expense tracker (or whatever other method you use to track your spending) into your monthly budget.

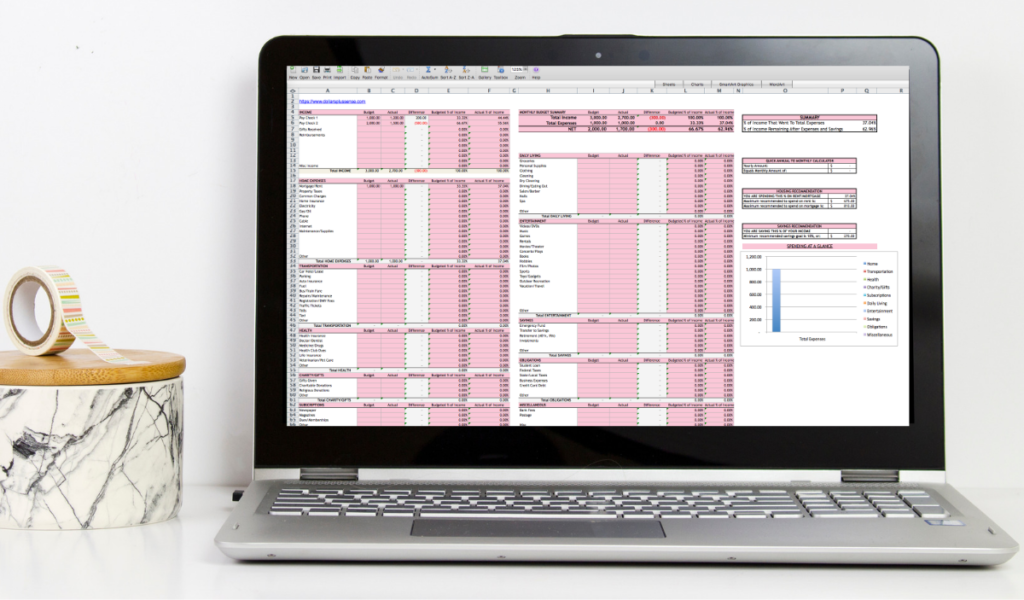

My Monthly Budget template is also a great tool that makes it easy for you to see exactly where your money is going and what percent of your income is going to what expenses. This makes it simple for you to compare your spending to the recommended averages I give you in the How Much Should I Be Spending article.

If you want to know step-by-step exactly how I use my household budget spreadsheet to manage my money, you can read “How I Use My Monthly and Yearly Household Budget Spreadsheet.”

Now that you have all of your numbers plugged into your budget, take a minute to sit down and compare the actual expenses versus what you planned for your budget. This will show you where you did well and where you may need to improve.

You should not let a month pass without reviewing your budget.

Step 5: Make Adjustments Where Necessary

Having documented your income and spending, see where you may be falling short and make the necessary adjustments. Are you saving enough money? Are there any areas where you can cut back?

If you spend more than you budgeted in a particular area, figure out why you spent more. Maybe your budget in that particular area is not realistic, and you need to make adjustments, or maybe you need to figure out ways to cut your expenses in that area.

- Related Article: How To Make A Financial Binder: Supplies List

Summary

Now you know how to make a budget worksheet for beginners. In summary, to make a budget that works, you need to determine your take-home pay and monthly expenses. Next, you need to know how much of your income you plan to spend in each expense category. Make sure to track and review your spending frequently. Finally, make changes in your budget when necessary.

Remember, your income, expenses, and priorities will change over time; therefore, your budget is constantly evolving as life changes. So it’s okay to adjust your budget accordingly—but always make sure you have a budget and review it regularly.

Related Articles:

- How To Make A Budget With Irregular Income: 3 Simple Steps

- How To Make A Budget When You HATE Budgeting

- Best Way To Budget On One Income

- How To Change Your Money Mindset So You Can Have More Money

If you want to remember this article, pin it to your favorite Pinterest board.

Want more help with this? The Budget Starter Toolkit picks up right where this post leaves off. Prefer to start free? The Printable Budget Binder has you covered.

Maybe you can do a blog on how to use your budget template? Maybe a step by step plan that really breaks it down how it works.

Thanks for the comment! That’s a great point, and I Will definitely have a post about that 🙂

If some one desires expert view on the topic of blogging and site-building afterward i advise him/her to pay a visit this web site, Keep up

the fastidious job.

Thank you!