Do you want to become financially free at an early age? If so, you have to learn how to save aggressively. So you may be wondering “how much to save monthly?” Find out how saving 30 percent of your income every month is possible.

Jump Ahead To:

How Much To Save Monthly?

There really is no fixed amount you should save monthly. How much you should save every month really depends on your financial goals. So you have to ask yourself “what do I want to achieve and how long will I give myself to achieve it?”

There are three timelines you should consider:

- Short-term goals (under 3 years).

- Mid-term goals (3-10 years).

- Long-term goals (more than 10 years).

By knowing: 1) what you want to accomplish, 2) how much you will need to accomplish it, and 3) when you want to accomplish it by, will help you determine how much to save monthly.

Most financial experts recommend saving at least 10% of your income every month. I think that’s a good place to start, but you should definitely work on trying to increase your savings to more than that.

If you’re like me and want to be financially free or retire early, I would aim to save 30% – 50% of your income.

How To Save At Least 30 Percent Of Your Income Every Month

Saving 30 percent or more of your income is very possible and easier than you think. The key to saving a significant amount of your monthly income is to focus on reducing your biggest expenses.

For most of us, the four biggest expenses we have are: 1) housing, 2) transportation, 3) food, and 4) utilities. However, for some, your four largest spending categories might be different.

By having a budget and tracking your spending regularly, you will be able to easily identify your largest spending categories.

Do You Have A Budget?

Before you try to figure out how to save at least 30 percent of your income, you need to have a budget first. Having a budget allows you to see how much your expenses are and track if you’re making progress with cutting your expenses.

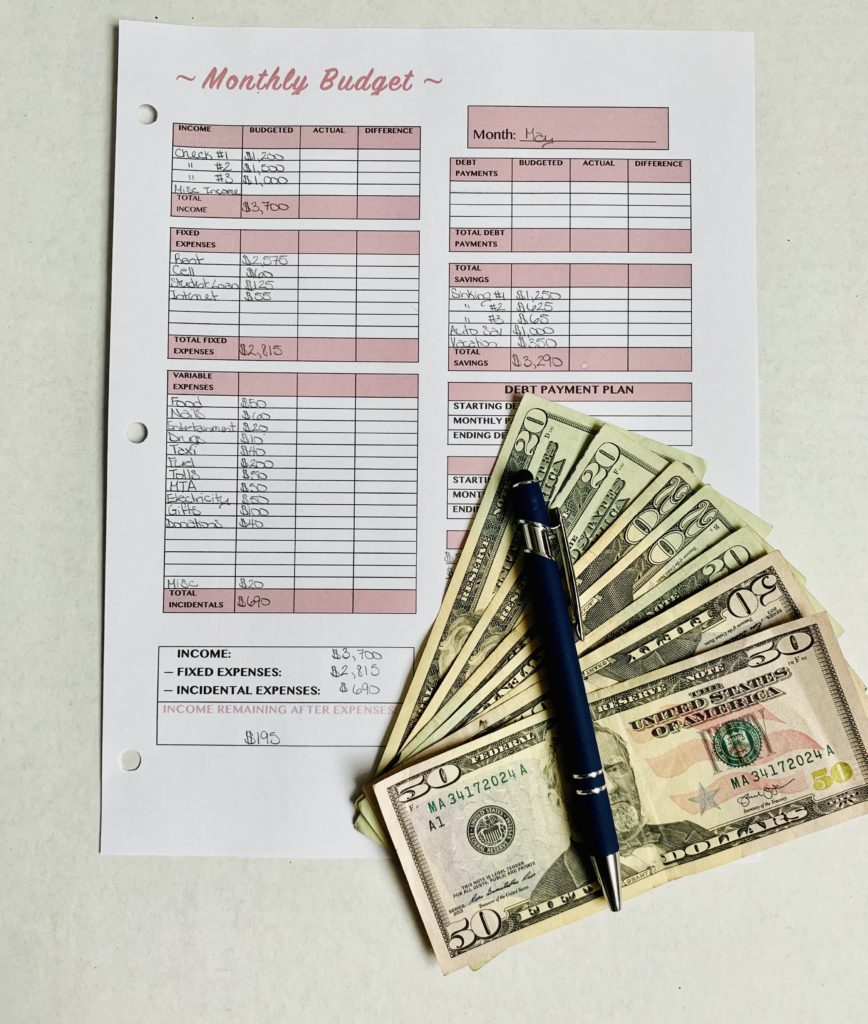

If you’re just starting out, you can download this FREE Monthly Budget Worksheet.

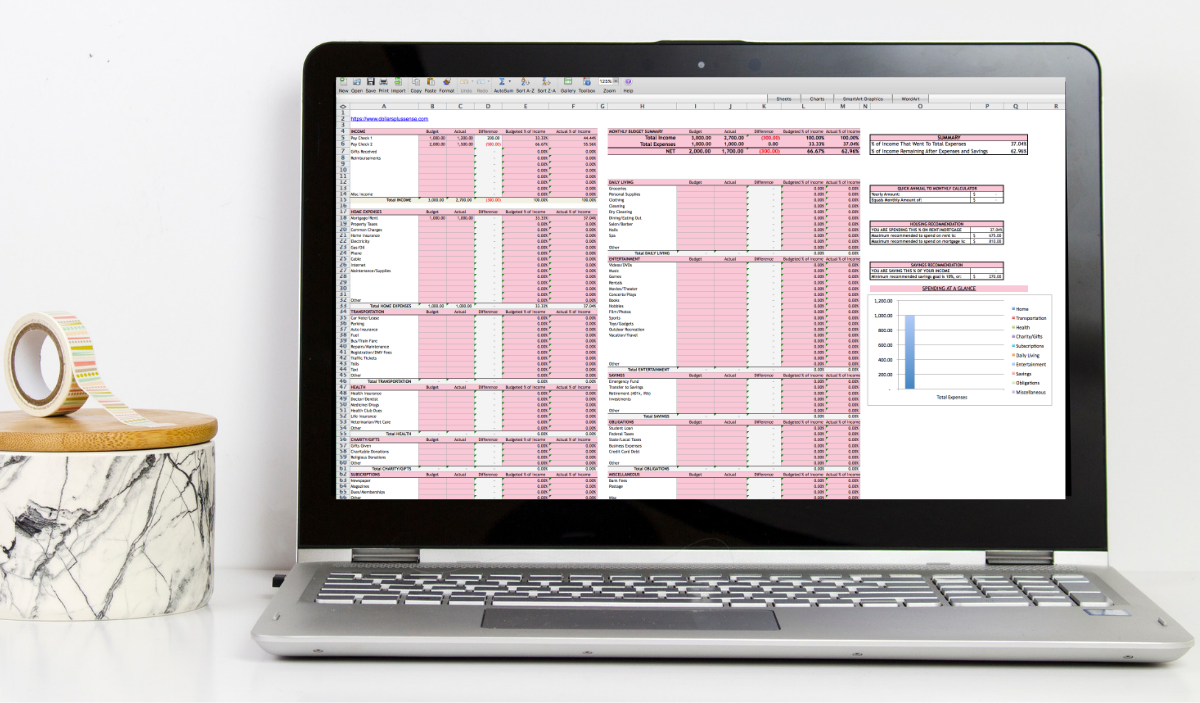

However, if you want to get serious with your savings and need something a little more sophisticated, you can get my Budget Template.

My template makes it easy to see exactly what percent of your income you’re saving. It also shows you what percent of your money you are spending. This is the template I actually used to save over 50% of my income and it is the same template I use to this date.

Track Your Expenses

Once you have your budget set up, you need to track your monthly spending. You can use this FREE Daily Expense Tracker to track your spending throughout the month.

If you HATE writing down what you spend, you can use FREE software like Personal Capital. Personal Capital gives you the ability to track your spending almost instantly by linking your credit cards and bank accounts.

It takes about 15-30 minutes to set it up in the beginning (depending on how many bank accounts and credit cards you have), but once you set it up you can forget it. All of your transactions are loaded to your Personal Capital account, and you can see all of your finances in one place.

The only disadvantage is you have to manually enter any transactions where you used cash.

At the end of the month, plug in the numbers from your daily expense tracker (or whatever other methods you use to track your spending) into your monthly budget.

Once your numbers are plugged in, take a minute to review the numbers. Sit down and compare the actual expenses versus your budgeted expenses.

This will show you where you did well and where you may need to improve. You will also see where all your money went. My Budget Template will make it easy for you to see what percent of your income when to what expense category.

Cutting Expenses

For most of us, housing, transportation, food, and utilities usually make up approximately 50%-70% of our budget. If you cut your spending in these four categories by half—and don’t cut in any other areas of spending—you would be able to save 25%-35% of your income.

I have a few detailed articles that can help you figure out how to cut your housing, transportation, and food expenses:

- 3 Easy Ways To Cut Household Expenses

- 9 Ways to Cut Costs Of Commuting To Work

- How To Reduce Food Budget Expenses: 9 Easy Ways To Save Money

Of course, by cutting expenses in your other low spending categories, you can increase your savings rate even more! So you have to cut expenses if you want to save at least 30 percent of your income.

Besides cutting expenses, you need to stick to your budget. If you do not stay on budget, chances are you will not have a significant amount of money left over to save. You also need to be disciplined with saving.

Get Out Of Debt

Getting out of debt is crucial to saving 30 percent of your income. The more monthly debt payments you have, the more money you need to cover your expenses every month. The more money you need every month, the harder it is to save money.

Start by paying off your highest-interest debt first. I consider any debt with an interest rate above 8% to be “high interest.” By focusing on your high-interest debt, it will reduce how much you pay in interest over the life of the loan.

The reason why I would pay off any debt with an interest rate above 8% is because the stock market has returned about 8% over the long haul. Paying off a debt with an interest rate greater than 8% is the equivalent to getting a guaranteed return of more than 8% on an investment.

Therefore, paying off your high-interest debt above 8% will most likely give you a better return on your money than investing in the stock market.

For your lower-interest loans, pay only the minimum monthly payment while you are focusing on paying down your highest interest rate debt.

Once you have paid off one loan completely, take the funds that are now freed up and apply it to the next debt in line. Do this until that loan is completely paid off, and then repeat again.

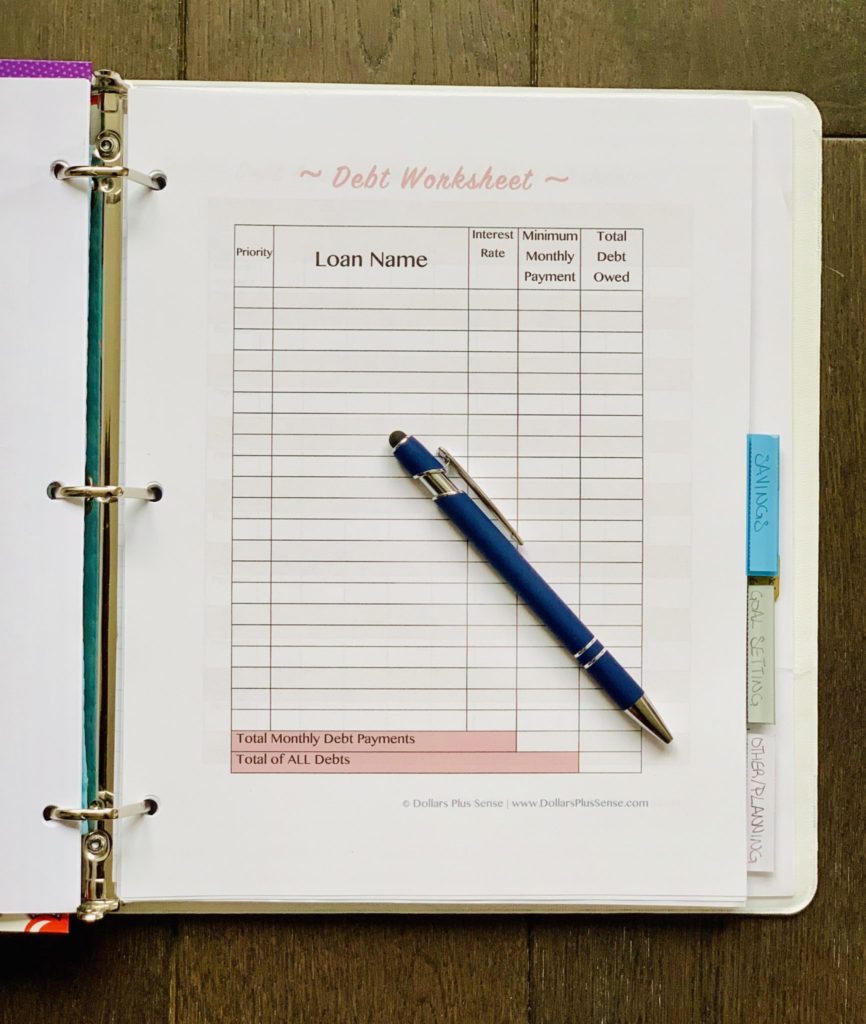

Use this Debt Worksheet found in my FREE Resouce Library to help you become more organized and prioritize your payment plan.

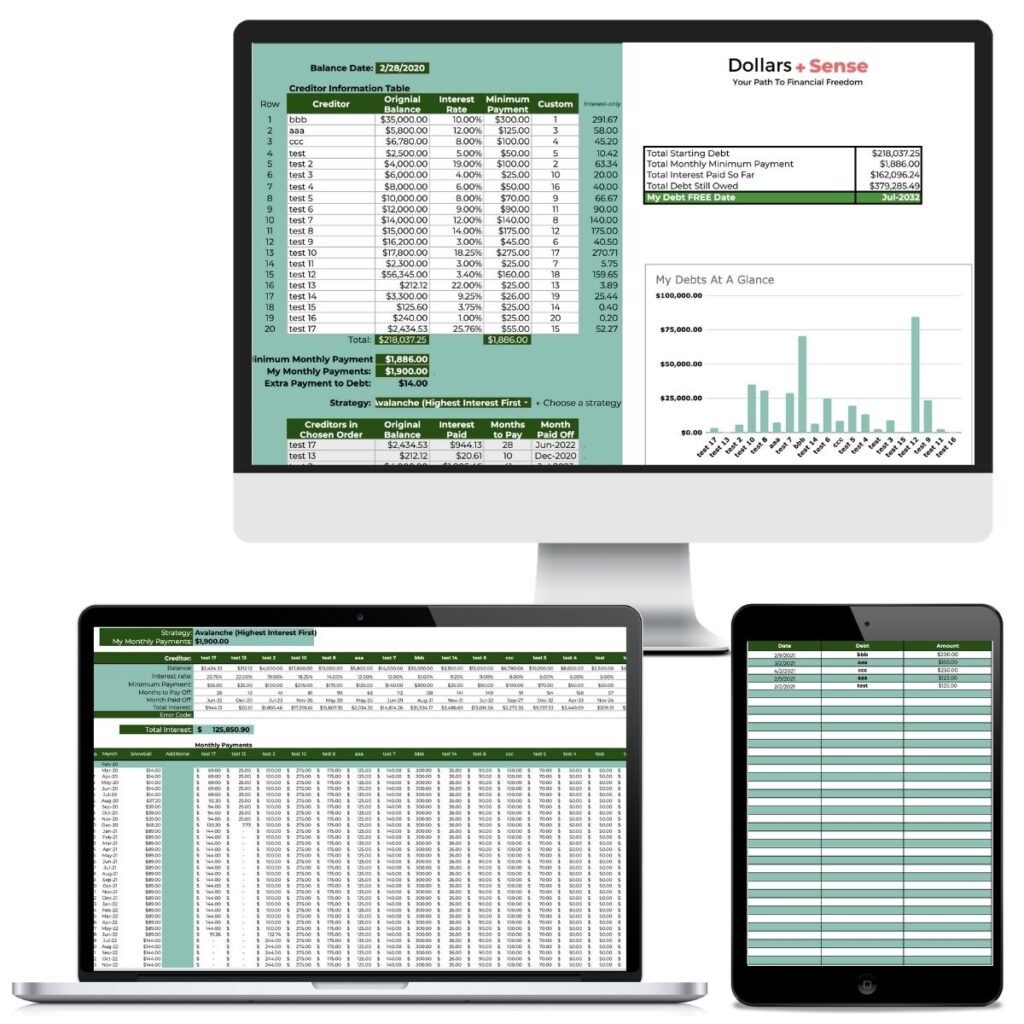

If you want something a little more sophisticated to help you make a debt payoff plan, check out my Debt Payoff Spreadsheet. The Debt Payoff Spreadsheet is an amazing tool for anyone who wants to get out of debt as quickly and painlessly as possible. This easy-to-use spreadsheet will help you establish a repayment plan and calculate your debt-free date so you can stay motivated to keep going.

- Related Article: How To Pay Debt Faster (Even If You Have No Money And A Low Income)

Strategy To Saving 30 Percent Of Your Income

Now that you know how to cut your expenses, hopefully by at least 30%, it is time to save that extra money. Not many of us are born “savers” and find it hard to save sometimes.

To reduce the temptation to spend, I recommend you “pay yourself first” and automate your savings. Paying yourself first means you put money in your savings account before you start to pay your other bills.

I love to shop, and I needed a way to “trick” myself into saving. I find when I put money in savings before I pay my bills I spend less because the money is just not easily available to spend.

You can make saving for your financial goals fun with my FREE Savings Tracker that you can find in my Resource Library. Color in each box as you put money towards your savings goals. Use this visual to motivate you to keep going until you reach your goal!

Use An Online Bank Account

When you save at least 30 percent of your income, I recommend you keep that money in an online bank account for two reasons:

- They usually pay higher interest on your money; and

- Your money is harder to access and therefore reduces the temptation to spend it.

With online banks, it usually takes a few business days for the money to be transferred to a physical bank where you can access the money; therefore it reduces impulse purchases.

A high-yield online savings account that I like is CIT Bank. I like this account because it pays a fairly high interest on your money (compared to other banks).

Also, since it’s an online bank, it’s harder to be tempted to spend your money.

If you want to shop around for some other accounts that might be better for your needs, you can find a list of some of the best high-yield online savings accounts HERE.

Automate Your Savings

Automating your savings is a big way to save at least 30 percent of your income. Automate your savings by setting recurring transfers to your online bank account.

Automating your savings makes it easier to save because you will never be tempted to skip saving. The money just goes into your savings account automatically before you can get a chance to spend it.

I recommend you set an automatic transfer to your online savings account every pay period. Automating the process lets your savings grow unattended.

If you schedule the transfer around the time that you get paid, the money for savings never really mixes with your spending funds. Over time, you may get used to living on that smaller amount, making it easier to let your savings build.

Summary

Hopefully, now you have an idea of how much to save monthly and that saving 30 percent of your income is possible. If you want to get aggressive and save at least 30 percent of your income, you need to cut your spending by reducing your biggest expenses; stick to your budget; open an online savings account, and automate your savings.

If you follow these tips, you will be able to save a significant amount of your income and achieve financial freedom more quickly.

Related Articles:

- How I Use My Monthly and Yearly Household Budget Spreadsheet

- Cutting Your Monthly Expenses: Why It Is Absolutely Necessary

- How I Saved $300,000 In 4 Years

If you want to remember this article, pin it to your favorite Pinterest board.

Want more help with this? The Save $1,000 In 30 Days picks up right where this post leaves off — or start smaller with the 31-Day Savings Challenge.

1 Comment on How to Save At Least 30 Percent of Your Income Every Month