Do you have a hard time making a budget because your income is irregular? I know how you feel because I faced this same challenge when I started budgeting. I am self-employed; therefore, it was very difficult for me to make a budget because my income varies every month. In this article, I discuss how to budget a variable income.

Jump Ahead To:

When I first started working for myself, it was hard determining what my take-home pay was. So I would use the income I made from the previous month as a way to determine what my budget was for the next month.

For example, if my take-home pay were $3,000 for the month of January, I would make a budget where I could not spend more than $3,000 in February. In other words, I would live on last month’s (January) income.

By living off last month’s income, you’re budgeting your month based on realistic figures, not income projections.

Meanwhile, during the month of February, I would deposit my earnings into my regular savings account—not my checking account! At the end of February, I would tally my income for that month. I then use my take-home pay for February and determine what my budget is going to be for March.

Next, I transfer my earnings from February into my checking account to pay all my bills for March. I would repeat this process every month for the first year.

Step 2: One Year of Paychecks

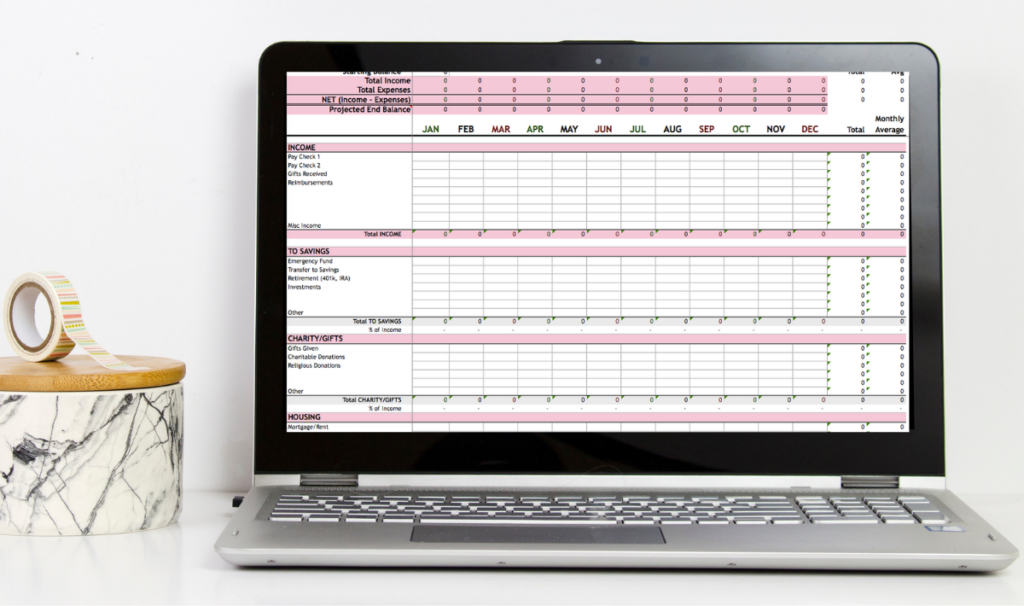

After I was working for myself for approximately a year, I would use my Yearly Budget to determine the average of how much I earned every month.

My budget template made this easy because it would automatically average out my income for me. Based on this average, I got an estimate of how much I could spend.

I’m very conservative when I make my budget. I think this is important for anyone with an irregular income because you don’t have the security of knowing exactly what you will be paid every month.

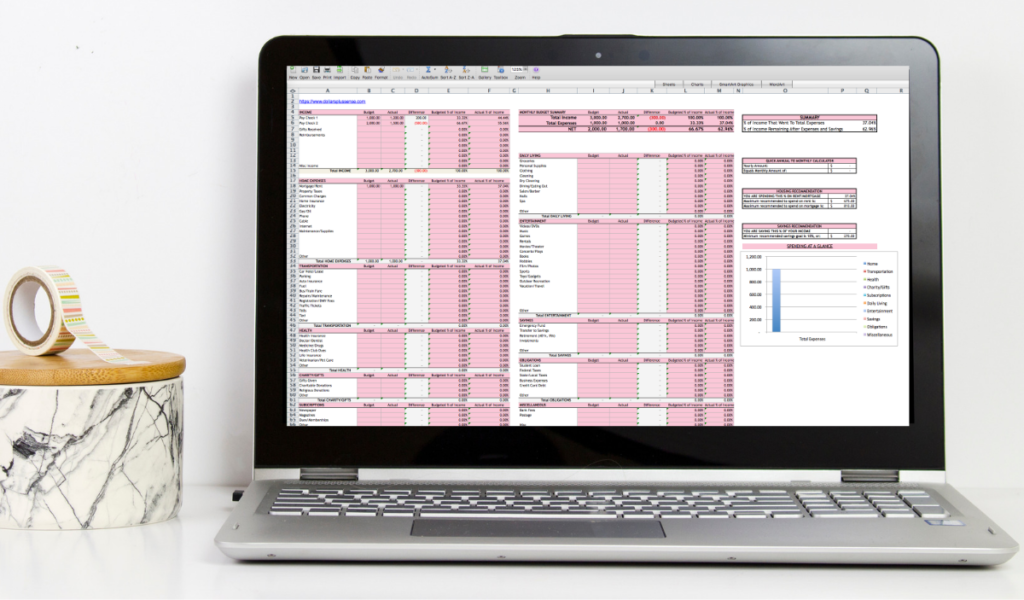

Given that my income varied every month, I had multiple monthly budget templates—low and regular. This is how to budget a variable income:

I would scan my yearly spreadsheet to see what I earned in my worst month. Based on that number, I formulated my “low budget.” What that means, is my low budget only allowed spending for absolute necessities.

Basic necessities that I needed to cover include:

Having a “low budget” provided me with security because I knew I could survive if I had a bad month. I also know exactly what I need to cut out during a low-income month to meet my necessities.

If I did not earn much money the previous month, I would use the low budget. I would also use the low budget if I wanted to save aggressively.

Make A “Regular” Budget

When I make my “regular budget,” I take the average of all my monthly income for the year to determine my income. Based on that number, I formulated my regular budget.

The regular budget included my necessities and discretionary spending. I normally use this budget most of the time.

If I have a good month and make more money than I projected on my “regular” budget, I try not to spend that extra money. This is important if your income varies because you never know when you’re going to have a bad month.

The last step you need to master when learning how to budget a variable income is how to handle your surplus and shortages.

If I happen to earn more than my average income one month, I will put that money towards my emergency fund.

I recommend you have at least a 6-month emergency fund if you are self-employed or a freelancer. Your emergency fund will be there to fill in the gaps on a slow month.

Once your emergency fund is fully funded, you can put your surplus to some other financial goal.

If I have a slow month, I draw from my emergency fund. I only draw from my emergency fund if my income is so low that I cannot even meet my obligations under my “low budget.”

This rarely happens, but it has happened. I like having the security of knowing that I can cover my bills if things get slow at work. That’s why I highly recommend you have an emergency fund as well.

Now that you know how to budget a variable income, I hope you take the time to make a budget for yourself. If you have an irregular income, it is even more important for you to have a budget. Just because your income is unpredictable doesn’t mean your budget needs to be unpredictable too!

Related Articles:

If you want to remember this article, pin it to your favorite Pinterest board.