Did your New Year’s Resolutions even last until February? If not, it’s time to take action to get back on track! Find out 17 easy ways you can turn things around and have better finances this year.

Jump Ahead To:

How To Get Control And Have Better Finances

1. Write Down Your Financial Goals

It is important to have a clear goal in mind so that you know exactly what you are working for and what you need to do to get there. Those with goals are 10x more likely to succeed.

Ask yourself what do you want out of life? Where do you want to be next year, five years, ten years or thirty years from now? Make goals and prioritize them.

I would start by establishing one big long-term goal, and then break it down to smaller more specific goals or milestones. Every day you need to do something that moves you towards your financial goal.

People who identify their goals and work towards them usually accomplish their goals and accomplish them quicker. This is the first thing you need to do if you want better finances.

To achieve your goals, they need to be written out and planned for. Make sure all of your goals are SMART (specific, measurable, achievable, relevant, and timely).

SMART:

- You want to make your goals as specific as possible;

- Measurable so that you can track your progress and know when you’ve achieved your goal;

- You want to make your goals realistic and achievable;

- Your goals should be relevant to your overall plans in life; and

- Finally, you want your goal to have a time limit where you set an end date to achieve your goal.

By making your goals SMART, you have a higher chance of actually achieving them. It makes your goals very clear, and lays out an easy to follow plan to reach them.

If you want more details about how to set SMART goals, you can read my article “How To Set Realistic Financial Goals You Can Actually Accomplish.”

2. Make Sure Those Goals Are Realistic

If you want better finances, you need to make sure your goals are realistic. I said earlier part of your SMART goal is making sure your goal is attainable. If your goals are too unrealistic or not achievable, you will probably give up on that goal in due time.

That’s not to say you shouldn’t set goals that are challenging; however, your goals should be realistic.

3. Know Your Starting Point

Now that you have your financial goals, and you know where you want to be financially, it’s important to know exactly where you are.

Start by calculating your net worth to see where your starting point is. Calculating your net worth is a simple formula. Subtract your liabilities from your assets (what you OWN – what you OWE).

You can find out your net worth quickly and easily with my Net Worth Worksheet found in my Shop.

It’s also very important to see where you’re starting from so you can compare your progress at the end of the year.

4. Know Your Expenses

Next, you need to determine what your monthly expenses. Write down a list of all your expected expenses for the month.

If you are not sure what your expected expenses are, start by looking at what areas you spent money on in the past three months. You can find this information by reviewing your past credit card and bank statements. Unfortunately, you will not be able to account for the areas where you spent cash, but it will provide you with a rough outline of your spending.

If you’re having a hard time figuring out how much you should be spending in each expense category, read my article “How Much Should I Be Spending?” This article will give you a general idea of how much of your income you should allocate to each spending area.

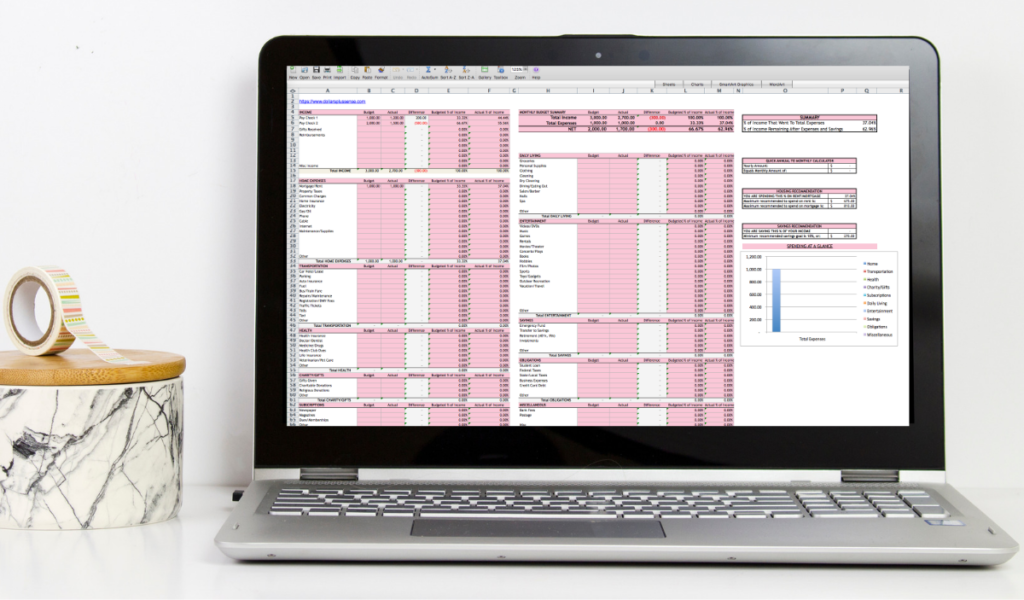

5. Make A Budget That WORKS

You need a budget to help you meet your financial goals and have better finances. Start by determining your take-home pay and your monthly expenses. Then determine how much of your money you want to allocate to each spending category.

Finally, I think you will love my budget templates to track and review your spending. By using these budget templates, you will get much closer to achieving your financial goals.

If you’re just starting out, you can download this FREE Monthly Budget Worksheet. However, if you want to get serious with your savings and need something a little more sophisticated, you can get my Monthly Budget Template.

This is the template I use to save over 50% of my income every month and it’s the same template I use to this date.

- Related Article: How I Use My Monthly and Yearly Household Budget Spreadsheet

6. Track Your Spending

Once you make a budget and allocate where your money is going, you need to track your spending to make sure you are sticking to the plan.

A budget is useless if you don’t follow it. Therefore, it is so important for you to track your expenses so you can make sure you are staying on track with your budget.

I personally recommend recording your spending every day, or at the very least, once a week.

You can download this FREE Daily Expense Tracker to help you. Print out multiple sheets (one for each spending category or sub-category). Then put all your sheets in your finance binder or a folder.

- Related Article: Budget Organization Tools: The Ultimate Personal Finance Binder

If you track your spending every day, you should write down what you spend as you go. You can either keep your receipts, or make a note in your phone or on a small piece of paper as you spend throughout the day. Then write the numbers in your expense tracker at the end of the day.

If you decide to track your spending every week instead, you can go online to your credit card, bank’s website, or third party website like Empower to see your spending for the week. You can then write down those transactions into your daily expense tracker.

Remember to also keep track of any cash you may have spent since this will not be on your bank statements.

Once you have recorded your spending for the month, plug in the numbers from your daily expense tracker into your monthly budget.

Take a minute to sit down and compare the actual expenses versus what you had in your budget. This will show you where you did well and where you may need to improve.

You should not let a month pass without reviewing your budget.

7. Don’t Forget To Have Fun

A lot of people’s budget fail because it’s just too restrictive. The first place we look to cut out expenses is our hobbies and entertainment because it’s not what you would consider a “need.”

The problem with that is if you don’t allocate money to some things you enjoy doing, it’s simply not going to work. It’s like having a strict diet and not allowing yourself to have a cheat meal.

Cutting out all the fun things is going to make you hate budgeting. If you hate budgeting, you’re simply not going to do it and quit. So decide ahead of time how much you’re going to spend on things you enjoy doing—but keep it reasonable. You can still have fun and stay on budget.

- Related Article: How To Have A Social Life On A Budget

8. Pay Yourself First

You should pay yourself first every time you get paid. Whatever’s leftover you can spend on your expenses. This is critical if you want better finances.

Just make sure you do not rely on your credit cards to make up for any overspending. If you do, then you’re not truly saving as much as you think you are, and the whole system will collapse.

9. Plan For Emergencies

Once you have a solid budget in place, I would focus on building an emergency fund. An emergency fund is money set aside to cover large unexpected expenses or to help you through hard financial times—like a job loss.

Preparing for the unexpected is necessary if you want to meet your financial goals. You don’t want to make progress with your financial goals, and then get thrown off by an emergency.

You should have enough cash available to help you through hard financial times or emergencies without having to rely on credit cards or take out other high-interest loans.

Your emergency fund should be 3-6 months worth of necessary expenses, but at the very least $1,000.

You want to also make sure you have adequate insurance. This includes health, renters/home, car, and life insurance. Insurance may seem like too much money when you are struggling to make ends meet, but it’s an absolute necessity.

A car accident can set you back, and any related medical bills can really damage your finances. Insurance protects you from the worst when something awful happens, and can give you the resources you need so that you can get through those moments.

- Related Article: How To Build An Emergency Fund

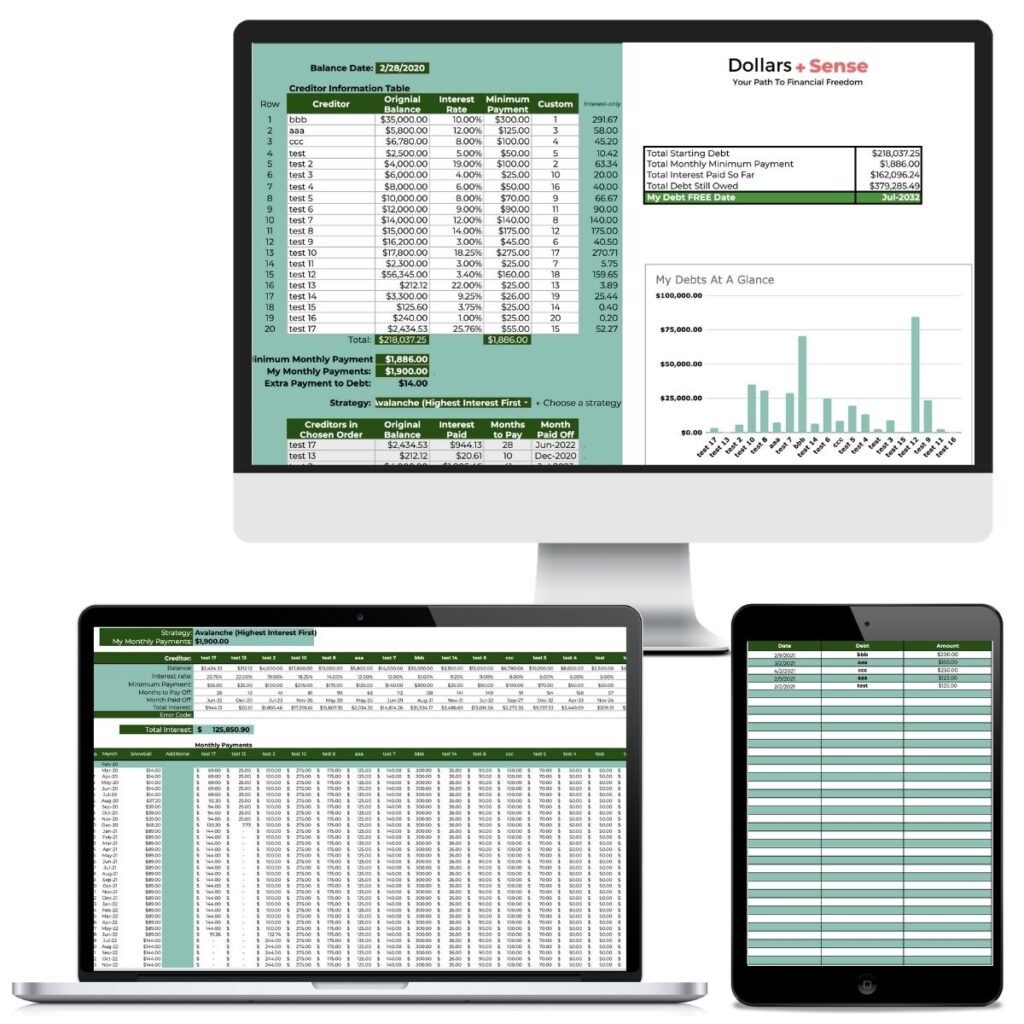

10. Focus On Paying Off Your Debt

Once you have at least $1,000 in your emergency fund, you can focus on paying off high-interest debt. Debt is a drain on your finances and slows down your achievement of financial goals.

You may have heard of the debt snowball method, a debt repayment strategy made famous by money guru Dave Ramsey. It is where you pay off your debts from smallest balance to largest balance, regardless of the interest rates.

I personally recommend you use the debt avalanche method when attacking debt. With the debt avalanche method, you pay your debts off from highest interest rate to lowest interest rate, regardless of the amount.

Mathematically, it makes more financial sense to use the debt avalanche method because you will pay less interest. However, depending on your personality, the debt snowball method can be more effective for you.

Start by listing all of your debt from highest to lowest interest rate. Use this Debt Worksheet to help you keep track of this. Take any extra cash you have and put it towards paying off your highest-interest debt.

For your lower interest debt, pay only the minimum monthly payment while you are focusing on paying down your highest interest rate debt.

Once you have paid off one debt completely, take the funds that are now freed up and apply it to the next debt in line until that is completely paid off—then repeat again.

Speed Up Paying Off Your Debt

If you’re like me, you like to use paper and software to help you with your financial journey.

For those of you interested in using technology to help with your debt repayment plan check out my Debt Payoff Spreadsheet.

The Debt Payoff Spreadsheets will help you get out of debt FAST by creating a fully custom debt payoff plan that keeps you motivated—so you can get out of debt and STAY OUT of debt forever.

The Debt Payoff Spreadsheet makes it easier, more strategic, and even motivating to get out of debt. Instead of guessing which debt to tackle first or struggling to track your progress, this spreadsheet does the work for you.

It gives you a clear breakdown of your balances, interest rates, and payment schedule—so you can see exactly how much you owe and when you’ll be debt-free. Plus, it helps you compare different payoff strategies (like the snowball or avalanche method) to find the one that will save you the most money and get you out of debt faster.

With built-in tracking, you’ll stay motivated as you watch your balances shrink each month. The more clarity and structure you have, the quicker you can pay off debt and regain financial freedom!

11. Increase Your Income

If you’re serious and want to have better finances quickly, you need to increase your income.

There are so many other ways you can make more money. For example, you can increase your income by:

- Making more money in your current job;

- Moving to a company that may offer more room for advancement;

- Finding a part-time job;

- Starting a side hustle or part-time business; or

- Establishing a passive income.

You can read more about increasing your income in “5 Ways To Increase Your Income Streams.”

12. Get Control Of Your Spending

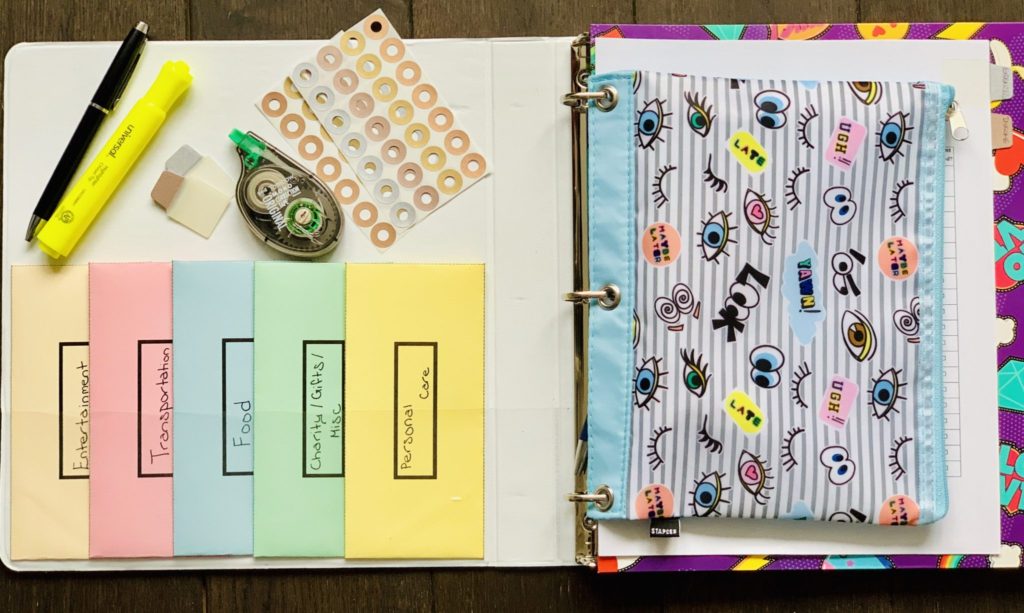

You need to get control of your spending if you want better finances. I highly recommend the cash envelope system if you have a hard time with overspending, sticking to a budget, or staying out of debt.

You may have heard of the cash envelope system made famous by money guru Dave Ramsey, but you might not be sure exactly how it works. The cash envelope system is a budgeting method where you use cash for the different expenses you have each month.

To learn more about the cash envelope method, you can read my detailed article “How To Use The Cash Envelope Method.” If you’re interested in trying this system, you can try taking the Cash Envelope Challenge. The Cash Envelope Challenge is designed to help you control spending, stick to a budget, and save more money by using only cash for certain expenses. This is the method I first used when I started my financial journey—so I highly recommend it.

I sometimes go back to this method to this day if I feel like my spending is starting to get out of control again. Here’s a picture of my cash envelopes that I’m currently using with my Personal Finance Binder.

If you love the idea of the cash envelope method, but don’t love the idea of walking around with cash all the time, you can try the cashless envelope system.

Using the cashless envelope method is pretty much the same as the cash envelope method. But instead of using the amount the money in your envelopes to track your spending, you would need to track your spending manually on an expense tracker. You can also use my FREE Daily Expense Tracker for this.

If you want to learn more about the cash envelope method without cash, you can read my article “How To Use The Cash Envelope System Without Cash.”

However, I would only recommend this system if you’ve been budgeting for some time and have a little more discipline with your spending. If this is your first time trying to stick to a budget, I would recommend you start with the cash envelope method first. Once you’ve mastered that, you can try the cashless envelope method.

13. Automate Your Savings

Sometimes we spend money just because we have it. So, to avoid this I recommend you set an automatic transfer to your online savings account every pay period as soon as you get paid.

Automating the process lets your savings grow unattended. If you schedule the transfer around the time that you get paid, the money for savings never really mixes with your spending funds. Thus, over time, you may get used to living on that smaller amount, making it easier to let your savings build.

Set up an automatic transfer every month to an online bank. This makes accessing your money more difficult, and much harder to spend.

14. Make Investing Part Of The Plan

Once you have gotten into the habit of saving regularly, you want to start focusing on investing. You cannot only save your way to your financial goals because that would take forever. You have to invest your money.

There are so many ways you can invest your money. Some ways include investing in stocks, bonds, real estate, and/or a business. You should invest in things that produce income and increase in value.

I like to invest in real estate and the stock market because in the long term it will increase in value over time, and it can also produce an income through cash flow.

Investing in real estate and the stock market has helped me achieve financial freedom more quickly than if I were to just save money.

When investing in the stock market, I personally use Robinhood.com to purchase individual stocks. I like this website and app because you can buy and sell stocks for free—there are no commissions or fees.

Most other brokerage firms charge at least a $4.95 fee per trade, and some have hidden fees. Sign up today and you and I can get a free stock like Apple, Ford, or Sprint. With Robinhood you also don’t need a minimum account balance, so you can get started right away.

Once you purchase some stocks, use the Stock Investment Tracker found in my Shop to see how your stocks are performing. If you are new to investing in the stock market and want to learn more, read my detailed article “Best Ways To Invest In The Stock Market For Beginners.”

15. Learn From Someone Who’s Where You Want To Be

Find someone who has achieved what you want in life, and look up to them. Put yourself out there and try to learn as much as possible. Do the things they do and try to mirror their success.

Even by being here and reading this blog post, you’re nurturing your own education and taking steps towards improving your financial situation. You’re not waiting for the answer to come to you, but you’re going out there and finding it yourself. So read books, ask questions, and reach out to people who you can learn from directly.

Is there someone in your network who’s doing what you want to be doing one day? If so, reach out to them. If you don’t know anyone, start out by reaching out to me! I’m always eager and willing to help where I can.

16. Ask For Help

Turning your finances around is not easy, and you should ask for help when starting out. Sit down and talk to a financial coach about your goals and current situation. A financial coach can give you advice specific to your situation and give you the tools necessary to achieve your financial goals.

I have mentored dozens of people to help them reach their financial goals. I can help guide you and hold you accountable to go through your financial journey. So, if you would like to work together, contact me to see how I work with my clients.

17. Stay Consistent And Keep Going

Finally, the key to better finances is to stay consistent and keep going. I know it may feel like you’ll never be able to dig yourself out of this hole you created, but you have to stay motivated throughout the process.

The more difficult your financial situation, the more time it will take to turn your finances around. This can be frustrating since you may feel like you have to sacrifice for months or even years to get out of debt and start working toward your goals. But when motivation isn’t enough, that’s when you have to turn to discipline.

There’s nothing special about me or what I did to get to where I am—all I did was not give up and kept going! So if you want to better finances, you have to be willing to do the work.

If you find you’re not motivated enough, disciplined, or just need someone to hold you accountable, I invite you to check out the Budget To Freedom Society.

The Budget To Freedom Society is my exclusive membership group designed to help you take control of your finances, break free from the paycheck-to-paycheck cycle, and build lasting wealth. We have an awesome community where you can connect with like-minded individuals who are on the same financial journey, so you never feel alone.

Summary

As we approach the second half of the year, it’s a chance to go over your finances and get back on track. It’s not too late to turn your situation around and have better finances!

Allow yourself to imagine for a moment how you’re going to feel at the end of the year when you look back and see all the progress you’ve made. What is that financial future worth to you today? Take action today, and don’t be afraid to ask for help along the journey. Cheers to your success!

Related Articles:

- 10 Reasons Why You Should Make A Budget

- 17 Reasons Why Your Budget Doesn’t Work

- 9 Reasons Why Sticking To A Budget Is So Hard (And How To Change That)

If you want to remember this article, pin it to your favorite Pinterest board.

Want more help with this? The 30-Day Budget to Freedom Challenge picks up right where this post leaves off.