One of the most important aspects of financial planning is setting goals. But what are examples of good long-term financial goals? In this blog post, we will go over examples of some common long-term financial goals and how you can meet them!

Jump Ahead To:

What Are Financial Goals?

Financial goals are aspirations that you want to achieve with your money. Whether it’s buying a house, paying off student loans, or retiring at age 55, financial goals are the things that you aim to achieve with your money.

Different Types Of Financial Goals

There are different types of financial goals that you may have. You can break your financial goals down into three different categories: short-term financial goals, mid-term financial goals, and long-term financial goals.

Short-Term Financial Goals

Short-term goals are goals that usually take less than one year to achieve. These goals include things like saving for a wedding or vacation.

Mid-Term Financial Goals

Mid-term financial goals are things that usually take between one and five years to achieve. Examples of mid-term financial goals include building up an emergency fund with three months’ worth of expenses or saving to buy a car.

Long-Term Financial Goals

Long-term goals are things that usually take five years or more to achieve and include examples like paying off your credit card balance in full, maxing out your 401(k) contributions, and building an emergency fund with six months worth of expenses (just to name a few examples).

How Do I Set Financial Goals?

When setting financial goals you want to make sure they’re S.MA.R.T. goals. S.M.A.R.T. stands for Specific, Measurable, Attainable, Relevant, and Time-Based.

Specific

Your goals need to be very specific so that you can measure them as you work towards achieving your goals. This often means having a dollar amount attached to it. For example, instead of saying “I want to save more money” your financial goal should be something more specific like “I want to save $25,000.”

Measurable

Your financial goals should be measurable so that you can check in on your progress and see how far you’ve come towards achieving them. For example, the financial goal of “I want to save $25,000” is measurable because you can track how much money you’ve saved towards this goal.

Attainable

Your financial goals should be attainable so that you will actually follow through with them. In other words, they shouldn’t be too lofty or out of reach for your current circumstances and income level. For example, “I want to save $25,000 in a year” might not be very attainable if you only have a part-time job and make $20,000 per year.

Relevant

Your financial goals should be relevant to your life so that you will actually care about working towards them. For example, if one of your financial goals is “I want to save $25,000” but you don’t care about saving money then this goal isn’t very relevant to your life.

Time-Based

Your financial goals should be time-based. This means setting a deadline for when you need to achieve them by. For example, you can improve the goal “I want to save $25,000” to “I want to save $25,000 in 5 years.”

Why Set Long-Term Financial Goals?

You should set long-term financial goals because studies show that people who set goals stand a better chance of actually achieving them. People who set goals usually achieve their goals because setting goals helps you understand what you want and forces you to figure out how to get there.

When you’re clear on what it is you want to accomplish, it’s much easier to come up with a step-by-step plan on how you can get there.

Why You Should Always Write Down Your Financial Goals

People who write down their goals are even more likely to have success getting to where they want to go. In fact, a study by Dr. Gail Matthews, a clinical psychologist from the Dominican University of California, found that writing down your goals can improve your likelihood of success by up to 42%.

You should write down your financial goals because:

- It will help you get clear on what you want to accomplish.

- Writing down your goals is a public commitment.

- It can help you figure out how exactly to get there.

- It will hold you accountable for making progress towards reaching those goals.

- It will help you stay motivated.

- It helps you increase focus and productivity.

- It serves as a reminder.

Writing down your goals also helps because by doing so you’re holding yourself accountable for achieving them and will work harder. Writing things down actually makes them feel more real which is why you should always write down your goals.

You can make financial goals, and even write them down, but a financial goal planner will help you take action.

Using a financial goal planner allows you to plan every task you need to do in order to reach your financial goals. This means you can schedule when to pay bills, save money, and even plan ways to make more money.

I created the Financial Goal Planner because I couldn’t find a planner I liked specifically dedicated to your finances.

With this planner, you can set up your budget, save more money, and make a clear plan to get out of debt faster than you ever thought possible. This goal planner has everything you need to be productive, manage your time wisely, organize your finances, and set money goals.

You can use the Financial Goal Planner as your daily planner and as your planner specifically dedicated to your finances.

You will save money with the Financial Goal Planner because you never have to buy another planner again. Keep the files for life and reprint the pages you need—or keep it in the digital format and use it with a note-taking app as I do.

You can read my detailed article about how the Financial Goal Planner will help you save more money.

Examples Of Long-Term Financial Goals

Some examples of common long-term financial goals are:

- Have an optimized spending plan

- Saving for retirement (or early retirement)

- Save down payment to buy a home

- Paying off your student loan debt

- Fully funding an emergency fund

- Starting a business

- Save for your kids’ college education

- Growing your wealth and net worth

- Build your credit score to 800+

- Pay off your house early

- Pay off all credit card debt

- Purchase rental property

- Pay off your car

- Buy a new car with all cash

- Have multiple streams of income

- Increase your income

- Improve your financial literacy

- Create an estate plan

- Save a million dollars

- Make over $100,000 a year

- Pay for a home renovation

1. Have an optimized spending plan

Having a working budget is the foundation of any financial goal you have on this list because it will keep you accountable for your spending habits and help you save more money over time. You cannot make a plan for your money if you don’t know where it’s going.

When it comes to budgeting, I would recommend creating a monthly spending plan because this allows you to see how much money is coming in vs. going out each month. If you don’t already have a budget that WORKS, I recommend you use my Monthly and Yearly Household Budget Spreadsheet. This spreadsheet has helped me save over 50% of my income!

If you want to learn more on how to create an effective budget, read my detailed article “How To Use A Monthly and Yearly Household Budget Spreadsheet.”

2. Saving for retirement (or early retirement)

One of the most important long-term financial goals you should have is saving for retirement. It is definitely a good idea to have a retirement plan so you can have enough money in your golden years. Start accumulating your retirement savings in a tax-sheltered account like a Roth IRA or 401(k).

3. Save down payment to buy a home

Another good long-term financial goal you should have is saving for a down payment on a home. Buying a house is a good long-term financial decision because it helps you build wealth through appreciation and equity in your home. With the right investment, your home can even generate extra money through cash flow.

If this is your first time buying a home, check out my article “10 Tips For Buying Your First Home.”

4. Paying off your student loan debt

Paying off your student loan debt is another good long-term financial goal you should have. Student loans can be a huge burden on your finances so it is a good idea to pay them off as soon as possible.

5. Fully funding an emergency fund

You should make it a priority to save for an emergency fund. This is money that you can fall back on if something unexpected happens like losing your job, getting sick, etc. Having at least three months’ worth of living expenses in an easily accessible account (like a savings account or money market accounts) will help you manage emergencies and avoid credit card debt when they occur.

- Related Article: How To Choose The Right Savings Account For Your Financial Situation

I like to keep my emergency fund in CIT Bank because they pay competitive interest rates (right now it’s 10x the national average), have no monthly maintenance fees, and you only need $100 to open an account.

If you’re just getting started and you’re not sure how much you should have in your emergency fund, read my detailed article “How To Build An Emergency Fund.” Use the emergency fund calculator in that article to figure out exactly how much you need to save in your emergency savings.

6. Starting a business

Starting a business is another good long-term financial goal you should have. It takes time and effort to start your own business but the reward can be worth it (especially if you’re not happy with your current job). Starting a business can help you generate passive income and build wealth for the future. The best thing about having your own business is your income potential is limitless.

7. Save for your kids’ college education

The cost of higher education has been rising at an alarming rate. So it’s important to start saving for your child’s college education as soon as possible if you want them to go to college without having student loans hanging over their head after they graduate.

An important thing to consider is the time frame of when your child plans to go to college. If you start saving early, your children can graduate from college debt-free. If they don’t want to go to college and choose a different path in life, the money is still there for them if needed. Read this article to learn more about what happens to a college fund if your child doesn’t go to college.

8. Growing your wealth and net worth

Growing your wealth and net worth is another good long-term financial goal you should have. The best way to grow your wealth is by investing in assets that appreciate and produce cash flow (like stocks and rental property).

If you’re interested in investing in stocks, the best thing to do is start small and learn how it works first before diving into a full-scale investment strategy.

If you are new to investing and really have no clue what stocks to choose, I would recommend using a robo-advisor. A robo-advisor is an online automated advisor. They will invest your money for you based on your specific financial goal and risk tolerance using computer algorithms.

Since robo-advisors are cheaper than what you would pay a human financial advisor, it is a great low-cost option for investing.

A great option to use if you’re just getting started is Acorns. I recommend Acorns for beginners because of its round-up feature. The way it works is you link your checking accounts and credit cards to Acorns and they will round every transaction up to the nearest dollar and invest it.

If you’re trying to decide between investing apps, read my Acorns vs. Robinhood comparison to see how they stack up on fees, beginner features, and investment choices.

So let’s say you spent $9.17 at lunch. Acorns will round up that transaction to $10 and invest the $0.83. All your spare change starts to add up and before you know it you’re saving and investing. This is perfect for the person who also has trouble saving.

If you’re curious about how much your net worth should be at this stage in life, read my article “Net Worth By Age: How Do You Compare?“.

9. Build your credit score to 800+

A great long-term financial goal to have is building a good credit score. A lot of banks and lenders use your FICO score when you apply for a loan or mortgage (it’s the most widely used credit scoring system).

The best thing you can do to build your credit score is to pay all your bills on time and don’t use more than 30% of your available credit limit each month. This will help your score grow over time. It’s also important that there are not any errors on your credit report because this could cause a significant drop in your score.

The best way to monitor your credit is online with a free service like Credit Karma (it’s free and secure). This will give you access to all three of your FICO scores which are crucial when applying for loans or mortgages in the future since they’re used by banks and lenders as part of the approval process.

10. Pay off your house early

You should consider whether or not it makes sense to pay off your house earlier. If the interest rate on your house is fairly high, then there’s no better time to pay down your home loan than when you have the option to do so.

I would make saving for retirement a priority over paying off your home (especially if you have a low-interest rate), but a good rule of thumb is to have your house paid off when you enter retirement.

The good thing about paying off your home loan early is you can save thousands of dollars in interest by doing it (in some examples, over $100k!).

If you want to learn more about how you can pay off your house early, check out my article “7 Best Ways To Pay Off Your Mortgage Early And Be Financially Free.” This article will give examples of how to pay off your mortgage early in detail.

11. Pay off all credit card debt

Another great long-term financial goal to have is paying off all your credit card debt. It’s important that you don’t accrue any more credit card debt while trying to pay it down because this will just delay the process and cost you thousands of dollars in interest payments over time.

If you find yourself with credit card debt, I would encourage you to list all your credit cards in order of the highest interest rate first. Then pay as much as possible on that card each month until it’s paid off completely.

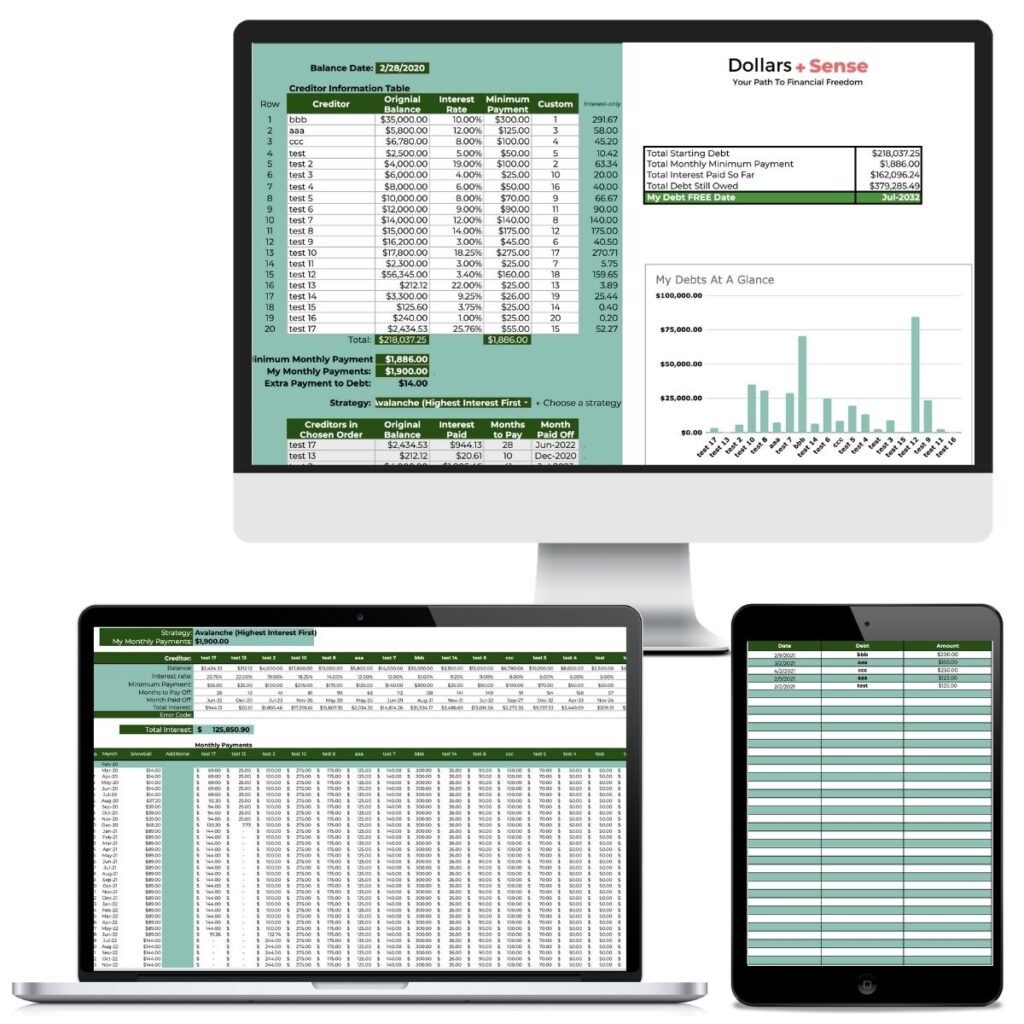

If you want a good tool to help you pay off your debt as fast as possible, check out my Debt Payoff Spreadsheet.

This spreadsheet will help you figure out a debt repayment plan for your specific situation and easily calculate your debt-free date!

You can also use this FREE Debt Payoff Tracker to help you track your progress. Use this visual to motivate you to keep going until you reach your goal!

12. Purchase rental property

Purchasing a rental property can be a great way for you to build wealth and generate passive income over time. The key here is finding the right location, making sure it’s in a safe neighborhood with low crime rates, having enough cash saved up for the down payment, and finding a great tenant.

I would encourage you to read my article “10 Major Benefits Of Investing In Real Estate From A Pro” to learn more about how you can get started in real estate.

- Related Article: Should I Hire A Property Manager? 11 Reasons Not To Hire One

13. Pay off your car

Paying off your car early is a good long-term financial goal to have because it can save you thousands of dollars in interest payments. Therefore, you should take advantage of any opportunity that you can to pay off your car early.

This will give you immediate relief from high monthly payments and can help improve your credit score since less money owed means better credit.

14. Buy a new car with all cash

You never want to pay interest on a depreciating asset such as a car. Therefore, it’s best to save up all the money you need for a car upfront and pay cash.

If you want your cash to go even further, I would recommend buying a used car because new cars lose approximately 20% of their value as soon as you drive it off the lot.

- Related Article: 9 Ways to Cut Costs Of Commuting To Work

15. Have multiple streams of income

A lot of us only have one source of income—which is usually our job. But did you know the average millionaire has seven streams of income?

Having multiple streams of income is a great long-term financial goal to have because it will give you financial security and protect you from one source of income drying up.

If you want examples of how to make more money, I would recommend reading my article “5 Easy Ways To Increase Your Income Streams.”

- Related Article: 70+ Things You Can Sell to Make Money Now

16. Increase your income

Increasing your income is another great long-term financial goal to have. One of the best ways to increase your income is by increasing the value you bring into other people’s lives. You can do this through education or just learning a new skill that allows you to provide more value in some way, shape, or form.

One of the easiest ways to increase your income is by making more money in your current job (i.e. – asking for a raise or working more hours), getting a higher paying job, finding a part-time job, or starting a side hustle.

17. Improve your financial literacy

Improving your financial literacy is important because it will help you make better decisions with your money. For example, if you have a better understanding of finance and investing, this will help you make more informed decisions as to where your money goes.

18. Create an estate plan

Creating an estate plan is a great long-term financial goal to have because it will ensure your assets are distributed according to your wishes when you pass away. An estate plan should include a will, power of attorney, and living will.

19. Save a million dollars

Saving a million dollars is a good long-term financial goal to have because it can help provide financial security for your family. It will take time and discipline to save up this much money. However, the reward of being financially independent will be worth all your hard work.

20. Make over $100,000 a year

If you make six figures or more per year, this gives you the ability to save an enormous amount of money each month. Making over $100,000 a year is a great long-term financial goal to have because it will allow you the freedom and flexibility of living life on your own terms.

If you are able to save at least 30% of your after-tax income, this could amount to over $30,000 per year in savings. Saving 30% of your income is certainly possible if you make over $100,000 a year. Check out my article “How to Save At Least 30 Percent of Your Income Every Month” to learn more about how you can get started.

21. Pay for a home renovation

If you are tired of your old, outdated home and want to make some improvements that will allow you to enjoy life more each day then paying for a home renovation can be a good long-term financial goal. The benefit of renovating your home is that it will increase the value of your home and allow you to live in a space that you love.

The cost of renovating an entire house can be quite expensive, however. If you are on a tighter budget but still want to renovate your home then I would recommend starting with one room or small project at a time so that you don’t end up over budget.

How Can I Achieve My Long-Term Financial Goals?

The first step towards achieving your long-term financial goals is to focus on only a few goals at a time. If you try to do too much at once it will be difficult for you to stay on track.

So ask yourself:

- What is the reason you want to achieve these goals?

- What are some examples of what achieving your goal will do for you, both in terms of lifestyle and emotions?

- What would life be like if you don’t achieve your goals?

Once you’re clear about the few goals you want to achieve, the next step is figuring out what steps need to take place in order for you to achieve them. The more specific and detailed you get with this step, the better outcome of achieving your long-term financial goals.

From there, I would recommend creating a calendar (or using an existing one) that allows you to schedule time for your goals each week or month. This way it will be easier for you to stay on track with achieving them over the long term. You can use my Financial Goal Planner to help you get started.

How Can I Stay Motivated By My Long-Term Financial Goals?

You should always keep your end goal in mind when working towards any big task. The best way to stay motivated is to have a plan for how you are going to get there. This means breaking down your goal into small, manageable tasks and checking them off as they become accomplished.

As you accomplish each small milestone goal, reward yourself. This way it is much easier to stay motivated and see progress day after day.

Prioritize Your Long-Term Goals Properly

Prioritizing your goals will help you stay focused on what is really important. Sometimes, people prioritize their goals in a way that doesn’t make much sense. For example, someone might spend all their time and energy trying to save up for an expensive luxury item rather than something they actually need like saving for retirement or a fully-funded emergency fund.

If you don’t properly prioritize your long-term goals, you will be taking away from the other bigger life priorities that are more important. If you want help trying to figure out how to prioritize your financial goals, check out my article “The Best Way To Prioritize And Achieve Your Financial Goals.”

Summary

There are many examples of long-term financial goals that you can work towards in order to help improve your financial security in the future. If you want to be able to save up one million dollars, make over $100,000 a year, or save for retirement, you will need to invest time and energy into the big picture. The best way to stay motivated is to break down your goal into small manageable tasks and reward yourself when they are completed. Finally, make sure that you’re prioritizing your long-term goals properly. This way it is easier to stay focused on what really matters.

Related Articles:

- How I Saved $300,000 In 4 Years

- 80 Great Personal Goals to Set

- How To Improve Time Management: 10 Easy Tips To Be More Productive

If you want to remember this article, pin it to your favorite Pinterest board.

Want more help with this? The Financial Goal Planner picks up right where this post leaves off.