Did you know that the net worth of a homeowner is 44 times greater than that of a renter? According to the most recent U.S. Federal Reserve study, the median net worth of homeowners were $231,400 (a 15% increase since the last report); and the median net worth of renters were $5,200 (a 5% decrease since the last report). So as you can see, buying a home is a great way to build wealth. In this article, I’m going to give you 10 tips for buying your first home.

Jump Ahead To:

Before trying to achieve any of your other financial goals, it is crucial that you have a functioning budget first. Creating a budget can help you save more money, and feel more in control of your finances. If you want to buy a house, the first thing you need to do is know where your money is going.

I personally use these budget templates every month to track my spending. It is the system I’m currently using for my budget, and it has helped me save over 50% of my income every month.

If you’re just getting started making a budget you can use this FREE Monthly Budget Printable.

Once you have a solid budget in place, I would focus on building an emergency fund. An emergency fund is money set aside to cover large unexpected expenses or to help you through hard financial times—like a job loss. This is a hard lesson everyone should’ve learned with the recent government shutdown.

Preparing for the unexpected is necessary if you want to meet your other financial goals. You don’t want to make progress with your other financial goals, and then get thrown off by an emergency. You should have enough cash available to help you through hard financial times or emergencies without having to rely on credit cards or take out other high interest loans.

I recommend saving three months worth of living expenses if you have relatively strong job security. If you have some instability in your employment or if finding another job could take you a long time, I recommend six months (or more).

What I mean when I say “living expenses” are the necessities (not luxuries like dining out and entertainment). However, no matter what your job situation is, I think everyone should have at least $1,000 set aside in case of an emergency.

Once you decide how much you want in your emergency fund, set a monthly savings goal and automate your savings. Once you have established a suitable size emergency fund, you can feel more secure knowing you are prepared for the unexpected.

Once you have at least $1,000 in your emergency fund, you can focus on paying off high-interest debt. Debt is a drain on your finances and slows down your dreams of buying a home. I consider any debt with an interest rate above 8% to be “high interest.”

You may have heard of the debt snowball method debt repayment strategy made famous by money guru Dave Ramsey. It is where you pay off your debts from smallest balance to largest balance, regardless of the interest rates.

I personally recommend you use the debt avalanche method when attacking debt. With the debt avalanche method, you pay your debts off from highest interest rate to lowest interest rate, regardless of the amount. Mathematically, it makes more financial sense to use the debt avalanche method. You will pay less interest if you pay off your highest-interest debt first.

However, depending on your personality, the debt snowball method can be more effective for you.

If you’re like me, you like to use paper and software to help you with your financial journey. For those of you interested in using technology to help with your debt repayment plan check out Undebt.it. It is a FREE tool to help you get out of debt.

I absolutely LOVE this website! There are SEVEN debt payoff plans you can choose from (including the debt avalanche and debt snowball method). You can even compare the different payoff plans to see which is best for you or make your own custom plan! They also have debt payoff calculators, which is also FREE.

You can keep track of all your payments and your debt payoff progress in one place. This software is so AWESOME and absolutely FREE! I haven’t come across something this good in a while!

Finally, they also have a premium account that has more features for you to take advantage of. The premium account is $12 for the entire year (only $1/month), which is still very affordable.

There’s a 30-day FREE trial if you want to check out the premium account. What I would do is sign up for the free account first, and then click on the free trial to check out the premium features. If you like it, then sign up for the premium account.

Once you have a debt repayment plan, you can use an app like Tally. Tally is the world’s first automated debt manager that makes it easy to save money, manage your cards and pay down balances faster. It’s absolutely free to download, and they don’t charge any fees to use the app.

The way Tally works is they monitor your balances, APRs, and due dates on each credit card you register. Tally’s smart technology will determine which cards to pay first, based on factors such as APRs and utilization.

In order to get the benefits of Tally, you will need to qualify for and get a Tally credit line. Depending on your credit history, your APR (which is the same as your interest rate) will be between 7.9% – 25.9% per year. If you have cards with a lower APR than your Tally credit line, you can manage the payments to those cards yourself; or have Tally pay only minimum payments to those cards to make sure you won’t be charged late fees.

You can also use an app like Qoins to help you automatically pay off your debt even faster. You’ve likely heard of apps that turn your spare change into investments (like Acorns) but Qoins is an app that takes that change and uses it to pay off your debt.

Qoins will send out payments according to the schedule that you’ve set up. They also track how much you’ve paid out towards your loans and see how much of a dent you’ve put in your debt.

I highly recommend Qoins if you want to speed up paying off your debt, while making it as easy and painless as possible.

Getting a mortgage requires a good credit score. Therefore, you want to check your credit to see where you stand and view your credit reports for any errors.

You can use a free tool like CreditWise to understand what makes up your score and find helpful ways to take action to improve it. If your score is where you want it to be, use CreditWise to keep an eye on your accounts and get alerts when something changes on your TransUnion® or Experian® credit report.

If you need to raise your credit score, a fast way to do it is to pay down credit card balances and stop using them for two months before you apply for a mortgage. Also, you’ll want to avoid applying for credit (for example, a new credit card or car loan) until after you’ve closed on your new home.

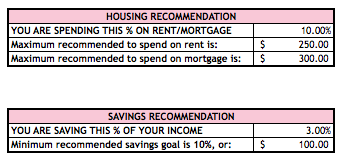

Before you even start to look at houses, you need to determine how much house you can afford. I recommend you spend no more than 30% of your take-home pay on your housing if you own. That 30% should include things such as property taxes, HOA fees/common charges, homeowners insurance, private mortgage insurance (PMI), etc.

My budget templates have a housing recommendation calculator that will help you figure out how much you should be spending every month on housing based on your take-home pay.

Once you know how much you can afford to spend every month on housing, start plugging in home values into a mortgage calculator to see what number falls in your ballpark.

For example, let’s say your take-home pay is $4,000 every month, your housing payment should be no more than $1,2000. Don’t forget property taxes and homeowner’s insurance will affect how much you can afford in mortgage payments.

Now that we know your housing payment should be no more than $1,200, let’s assume you plan to take out a 30-year mortgage with a 4% fixed interest rate. When plugging in numbers in the mortgage calculator, a $200,000 mortgage works out to be $955 per month. That leaves you with $245 for your property taxes and homeowner’s insurance.

Add the amount you saved for your down payment to the $200,000 mortgage, and that’s how much house you can afford. If your homeowners insurance and taxes are more than $245 per month, or you have other fees you have to pay (such as HOA fees or PMI), you will have to lower the price of the house you can afford.

Since property taxes and the cost of homeowner’s insurance vary, check with your real estate agent and insurance company for estimates to calculate how much house you can afford.

Now that you have a ballpark figure of how much house you can afford, it’s time to save for your down payment. I recommend you save at least 20% for your down payment. Here are some reasons why I think you should put down 20% or more:

However, I get that sometimes saving 20% or more may take years or decades (especially if you live in a high cost area like me). If saving 20% or more for your down payment isn’t reasonable for your timeline, there are a lot of first-time home buyer programs that offer low down payments (such as FHA and VA loans). Some of these first-time home buyer programs offer a down payment as little as 3.5%.

I know some money gurus will tell you to absolutely not buy a house unless you have 20% or more to put down; or that you should even buy your house cash—I disagree. Although I think you should put 20% down when buying your house, I think there are some exceptions to this rule.

As I stated in the beginning of this article, buying a home is a great way to build wealth; and sometimes it does not make sense to wait until you have 20% down to buy a house.

It’s okay to put less than 20% down if:

Remember I said one of the benefits to putting 20% or more down is so you can have more equity into your home when you buy it. Having more equity in your home safeguards you from being “under water” if the real estate market turns.

However, if home values are rising quickly, you’ll increase your equity without having to put down extra money to make it happen. Therefore the need for a large down payment is less important in that kind of market.

However, as long as you can easily afford the monthly payment, I don’t see why you have to wait until you have 20%. Just understand that you will be paying more interest over the course of the loan.

You can’t only save for your down payment, you’ll also need to save money for your closing costs. Closing costs are fees associated with buying your home that you pay the day the house become yours.

On average, closing costs are about 2-5% of the purchase price of your home. Your lender will give you a Loan Estimate, which will include your closing fees. But these are just an estimate, and the numbers can change.

Keep in mind that closing costs are negotiable, so shop around to find the lenders who are willing to offer you a loan with lower fees at closing. You can also negotiate with the seller and ask them to cover some of your closing fees.

Some other fees to keep in mind that’s an important part of the home-buying process are:

These fees you may have to pay before the house becomes yours.

Once you save for your down payment and your closing costs, don’t forget to set money aside for expenses associated with moving in. For example:

Once you have enough saved up for your down payment and your closing costs, it’s time to get preapproved for a loan.

It’s important to get a preapproval letter before you start your home search. By getting preapproved, you’re showing the seller you’re a serious buyer and you can afford the home. This is really important in a competitive market. Sellers will be more inclined to take an offer where they know financing won’t be an issue.

To get preapproved, your lender will look closely at your credit and verifies your income. Keep in mind, that mortgage pre-approval does not guarantee your loan will be approved because it is subject to property appraisal and other requirements. A preapproval letter is also generally only valid for 60-90 days.

The last of my 10 tips for buying your first home is you should always be logical when making your decision.

Buying your first home can be incredibly emotional, so it’s so easy to make a decision with your heart rather than your head. You may walk into a home and “fall in love” with it and insist you have to have it. The problem with this is you may make a bad investment or overpay.

Buying a house is a BIG decision that you should take seriously—it should be a rational decision, not an emotional one. If you appear too desperate, you will be giving away your bargaining power. Therefore, the seller’s agent will know they can get more out of you and you may end up paying more than you need to.

The best strategy is to stay cool, make a plan in advance, and stick to it! Determine your maximum budget and stay firm. If you find yourself in a bidding war for a property that will push you beyond your comfort zone, walk away! I promise you there will be a better house that suits your needs—you just have to be patient.

Now that you know my 10 tips for buying your first home, you may be wondering “what happens after the seller accepts my offer?” Once the seller accepts your offer, the closing process will begin. Here are some things you have to do before you sit down at the closing table:

You want to make sure you have a real estate attorney review the terms of the deal (also known as a purchase agreement) before you sign anything. Ask them to explain anything to you that you don’t understand, because once you sign, you’re in a legal binding agreement.

Once you sign your purchase agreement, the seller has to take the house off the market, and is obligated to sell to you (even if they get a better offer)—remember they’re in a legal binding agreement also. In most cases, you will be required to make an escrow deposit (commonly known as earnest money).

An escrow deposit is money you deposit to show the seller you’re a good-faith buyer and that you have all intentions of completing the deal. This is important so the seller doesn’t take his or her house off the market for someone who isn’t serious.

This payment is usually held in an escrow account and is later applied to the purchase of the property. This deposit is usually non-refundable, but you can get it returned to you if something specified in the contract goes wrong.

For example, earnest money would be returned if the house doesn’t appraise for the sales price or the inspection reveals a serious problem. But remember, these contingencies have to be listed in the contract—hence, why it is so important to have a real estate attorney.

Next, you should order a home inspection with a professional inspector. The purpose of the home inspection is to make sure the home is good structural shape and everything is in working order. Your inspector will be looking for minor and major defects, and elements that may violate local building codes.

Many lenders require a home inspection; but even if your lender doesn’t, I still recommend you get one anyway. You want to make sure you’re getting what you bargained for. If the inspection uncovers a major problem that needs to be fixed, you would want to bring this up to the seller before closing. You can also use any defects in the property as a bargaining tool to reduce the purchase price.

At this point, you want to start working on securing your loan. Even though you were preapproved for a loan, you still have more work to do to get a final approval on your financing. Your mortgage lender will give you a detailed list of additional financing information they need. Understand that this process will typically take a month or longer.

Your lender will also require an appraisal before loaning you any money. This appraisal is to make sure they don’t lend you more money than your house is worth. This is another reason why I say to buy with your head and not your heart. Because if you offer to pay more for a house than it’s worth, your deal may fall through unless you come up with more money.

The appraisal fee will be included in your closing costs.

Most lenders will require you to have proof of homeowners insurance in order to get approved for the loan. So start shopping around now to make sure you get a good and affordable policy that meets your lender’s needs.

You also want to do a title search and get a title insurance policy. A title search will help uncover any title defects tied to your property before you buy it; and title insurance will protect you from title problems that may become unknown after you close your transaction.

Title problems are more common than you think, and even if your lender doesn’t require it, you should definitely cover yourself anyway. For example, when I was purchasing a property, a title search uncovered that the seller had a lot of unknown liens that he wasn’t aware of. Had I purchased the property without doing a title search first, I would’ve been responsible for his former debts even though it is not my own.

I had another incident where a title search found old tax bills that were unpaid—this was a shock to the seller. Without a careful title search, these old tax liens would have become my problem had I not had the old liens resolved at closing.

Sadly for the seller, he did not do a title search when he purchased the property and did not know of these old tax debts when he was buying the home—and they became his problem.

So I can’t stress enough how important it is to do a title search and get title insurance.

On closing day, you will want to do your final walk-through. Your final walk-through is your last opportunity to make sure the house is delivered to you in the condition you agreed to purchase it in. Usually, the realtor will arrange for this to happen.

During the final walk-through, make sure that all requested repairs have been made; everything is in working order; the seller has removed all of their possessions; and that the home is clean.

If you encounter any unexpected problems during the walk-through, let the real estate agent know. It’s not too late to make things right, and most sellers will agree to pay for any necessary repairs or cleaning tasks.

Before you actually sit down at the closing table, your title company, loan officer, and/or attorney will tell you exactly what you need to bring with you.

Once at the closing table, you will be sitting down to sign numerous documents with your attorney, title company, lender, and real estate agent. The sellers may be there as well with their agents. There will be a TON of documents to sign, so make sure you ask your attorney to explain what everything means before you sign it.

Next, several checks will be exchanged and then you will be given the keys to your new house. At that point, you should be all set to move into your new house!

Buying a home is a great way to build wealth. Once you implement my 9 money tips for buying your first home you will feel more confident with your purchase.

Related Articles:

If you want to remember this article, pin it to your favorite Pinterest board.