During the U.S. government shutdown, I kept hearing the many stories of Americans struggling because of the loss of one paycheck. I think this situation should be a learning experience for us all. In this article, I will go over 5 financial lessons from the government shutdown we all should learn.

Jump Ahead To:

1.Stop Living Paycheck To Paycheck

The U.S. government last shut down started on December 22, 2018 and I too felt the effects of it. I’m an immigration attorney, and at the time, most of the immigration courts were closed. Since I’m self-employed, if I don’t go to court, I don’t get paid.

This government shutdown that began on October 1, 2025, makes me wonder why so many Americans are going through financial hardship because of the loss of one paycheck. And it made me realize a lot of people are still living paycheck to paycheck.

According to Forbes 78% of full-time workers live paycheck to paycheck. I think this is a staggering statistic.

I’m not here to belittle anyone, because I, too, once lived paycheck to paycheck, but this government shutdown has highlighted how much of an overall problem this is in our country.

I can understand if you’re just starting out in your career, or you had a financial emergency that left you with very little savings, but the statistics show that’s not the case—people simply aren’t saving enough money.

You don’t want to be in a situation where the loss of one paycheck will stop you from paying your bills.

So the first and most important lesson from the government shutdown we should all learn is to stop living paycheck to paycheck. Start saving some money every month—even if it is a very small amount of money.

Open a high-yield savings account with an online bank. You get two benefits by opening an online savings account:

- They usually pay higher interest on your money than a brick-and-mortar bank, and

- Your money is harder to access. With online banks, it usually takes a few business days for the money to be transferred to a physical bank where you can access the money; therefore, it reduces impulse purchases.

Next, set an automatic transfer to your online savings account every pay period. Automating the process lets your savings grow unattended.

If you schedule the transfer around the time that you get paid, the money for savings never really mixes with your spending funds. Thus, over time, you may get used to living on that smaller amount, making it easier to let your savings build.

Set Up A Budget

Having a budget is important if you do not want to live paycheck to paycheck anymore. If you’re just starting out, you can download my FREE Budget Binder.

However, if you want to get serious with your savings and need something a little more sophisticated, you can get my Budget Template. This is the template I actually used to save over 50% of my income every month, and it is the same template I use to this date.

2. Have An Emergency Fund

Once you have saved up enough money to ensure you can survive if you miss one paycheck, continue to build up your savings so you can fully fund your emergency fund.

This is one of the most important lessons from the government shutdown you can learn. An emergency fund is money set aside to cover large unexpected expenses or to help you through hard financial times—like a job loss.

The size of your emergency fund depends on your personal situation.

I suggest an emergency fund that is at least three to six months’ worth of living expenses. When I say “living expenses,” I mean only necessities, such as rent and groceries. I don’t mean shopping, entertainment, dining out, or vacations.

If you want to learn more about emergency funds, you can read my detailed article titled “How To Build An Emergency Fund.”

3. Have An Additional Source of Income

It is so important to have an additional source of income because it protects you in case one source “dries up.” One of the lessons from the government shutdown you must learn is you cannot rely on only one source of income. You can add other sources of income by:

Finding A Part-Time Job

Some examples are driving Uber, bartending, tutoring, retail, customer service representative, etc. Use my Uber link for $740 guaranteed. If you earn less, Uber will pay you the difference.

Starting A Part-Time Business Or Side Hustle

I personally like side hustles more than a part-time job because you’re the boss, and therefore offered more flexibility. In addition, there is more room for income growth.

The only downside to a part-time business is your income is not as stable or predictable as it would be if you had a part-time job.

When deciding what kind of part-time business to start, ask yourself “What are my talents and skills?” Figure out what kind of things you like to do.

Is there a way to turn your hobbies into additional income? If so, consider starting a part-time business or side hustle.

Establish Passive Income

There are so many ways you can establish passive income such as lending money, creating a product, or investing.

Having additional sources of income can also help you save more money every month to put towards your savings goals and emergency fund.

4. Get Your Debt Under Control

It’s important to get your debt under control. The more monthly debt payments you have, the more money you need to cover your expenses every month. The more money you need every month, the harder it is to save.

Also, the higher your expenses every month, the more money you will need to cover you in case of an emergency. Use the Debt Worksheet that you can find in my Shop to help you become more organized and prioritize your payment plan.

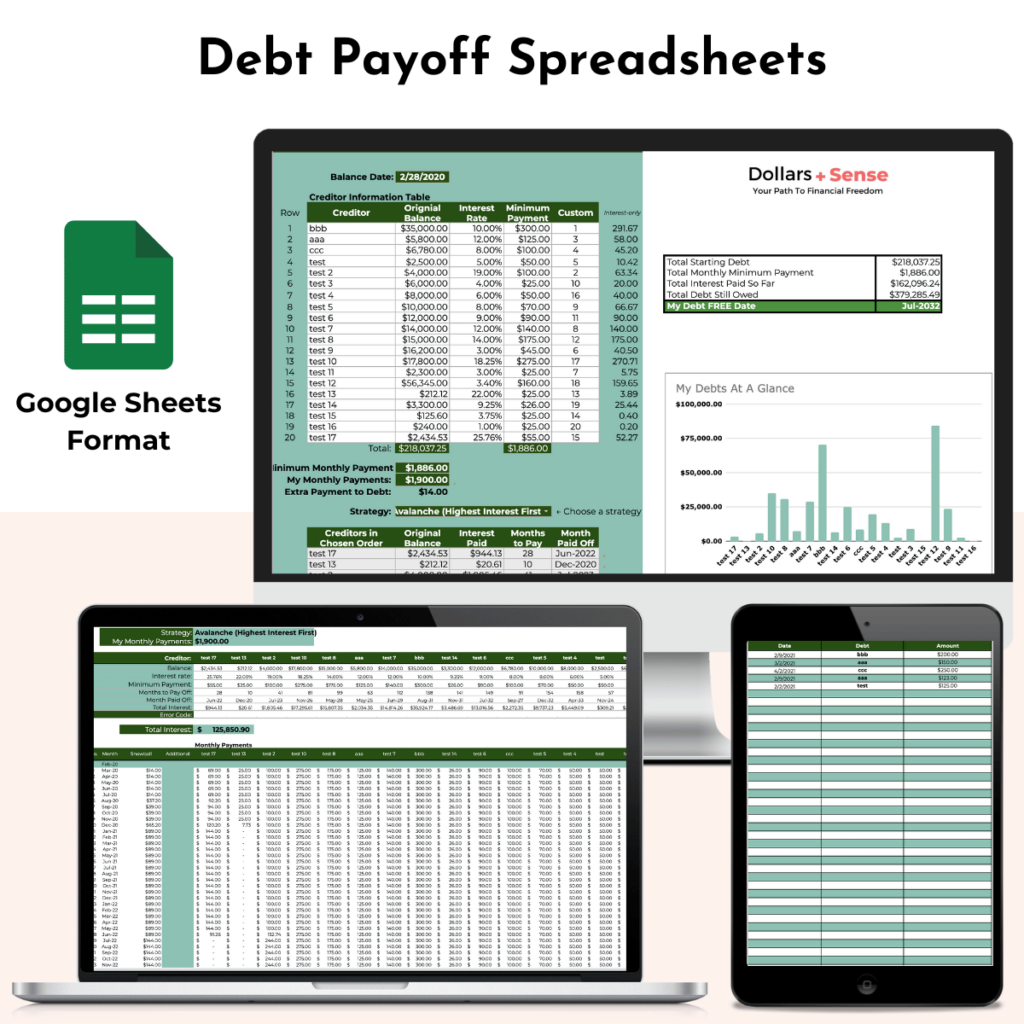

Use Technology To Help

If you’re like me, you like to use paper and software to help you with your financial journey. For those of you interested in using technology to help with your debt repayment plan, check out my Debt Payoff Spreadsheet.

The Debt Payoff Spreadsheets will help you get out of debt FAST by creating a fully custom debt payoff plan that keeps you motivated—so you can get out of debt and STAY OUT of debt forever.

5. Get More Educated About Personal Finance

One of the final lessons from the government shutdown that you should learn is you need to be more educated about personal finance. The most successful leaders in business and finance read every single day.

Warren Buffet reads 500 pages every day; Mark Cuban reads 3 hours a day; and Bill Gates reads at least 50 books a year. With this in mind, you should try and get into the habit of reading and get more educated about your finances.

You’re taking the right step by being here and reading my blog. Take advantage of my FREE Resource Library. There you will find my favorite personal finance books and podcasts that have helped me on my financial journey. You will also find tons of FREE printables, worksheets, checklists, and other money-saving tools and tips.

Summary

Although the government shutdown is focusing on the financial hardship to federal workers, this problem is not unique to them. In summary, 5 financial lessons from the government shutdown we all should learn are:

- Stop living paycheck to paycheck.

- Build up enough savings to have 3-6 months’ worth of living expenses.

- Add an additional stream to your monthly income.

- Try to reduce your high-interest debt as much as possible.

- Get more educated about personal finance.

If you are one of the majority of Americans who would also be unprepared for a financial setback, consider making some changes so you can have peace of mind.

If you want to remember this article, pin it to your favorite Pinterest board.

Want more help with this? The Recession-Proof Your Finances Masterclass picks up right where this post leaves off.

1 Comment on 5 Personal Financial Lessons From The Government Shutdown