If you owe back taxes to the Internal Revenue Service (IRS), you may be wondering how long they can collect them. The good news is that the IRS has a number of years in which they can try to collect back taxes from you. However, there are a few things that can affect how long they have to collect. In this blog post, I will discuss how long the IRS has to collect back taxes and what can affect that timeline. I will also provide some tips on how to deal with back tax debt.

Jump Ahead To:

How Long Does The IRS Have To Collect Back Taxes?

The IRS generally has 10 years from the date of assessment to collect on a balance due. This is known as the statute of limitations. The tax assessment date can change if you file an amended return or if the IRS has filed a substitute return on your behalf and you file a return to correct it.

What Can Affect The Timeline?

When the IRS refers to its time left to collect, they usually say “CSED,” which stands for Collection Statute Expiration Date. However, there are a few exceptions that can extend the amount of time the IRS has to collect back taxes.

For example, the CSED date can exceed the 10-year period if the IRS is not legally allowed to pursue collection actions against you—such as filing bankruptcy, filing a lawsuit against the IRS, applying for an installment agreement or Offer in Compromise, requesting innocent spouse relief, or living outside of the US continuously for over 6 months. All these things stop the clock on your CSED.

The IRS can also extend the ten-year statute of limitations if they suspect you of tax fraud or by suing you in federal tax court, although this only happens in rare cases.

Obtaining An IRS Transcript For Your CSED

If you want to know your exact CSED date, you can request a transcript from the IRS. This is a free service that the IRS offers.

You can get your transcript by calling the IRS at 800-829-1040, or by visiting their website through the IRS online portal (available at IRS.gov) or by completing Form 4506-T, Request for Transcript of Tax Return. The earliest CSED will display on the account transcript.

Tips For Dealing With Back Tax Debt

If you find yourself owing back taxes to the IRS, there are a few things you can do to help ease the burden. First, make a budget to see how much you can afford to pay each month. If you want to know step-by-step exactly how I created a budget to manage my money you can read “How To Use The Monthly and Yearly Household Budget Spreadsheet.”

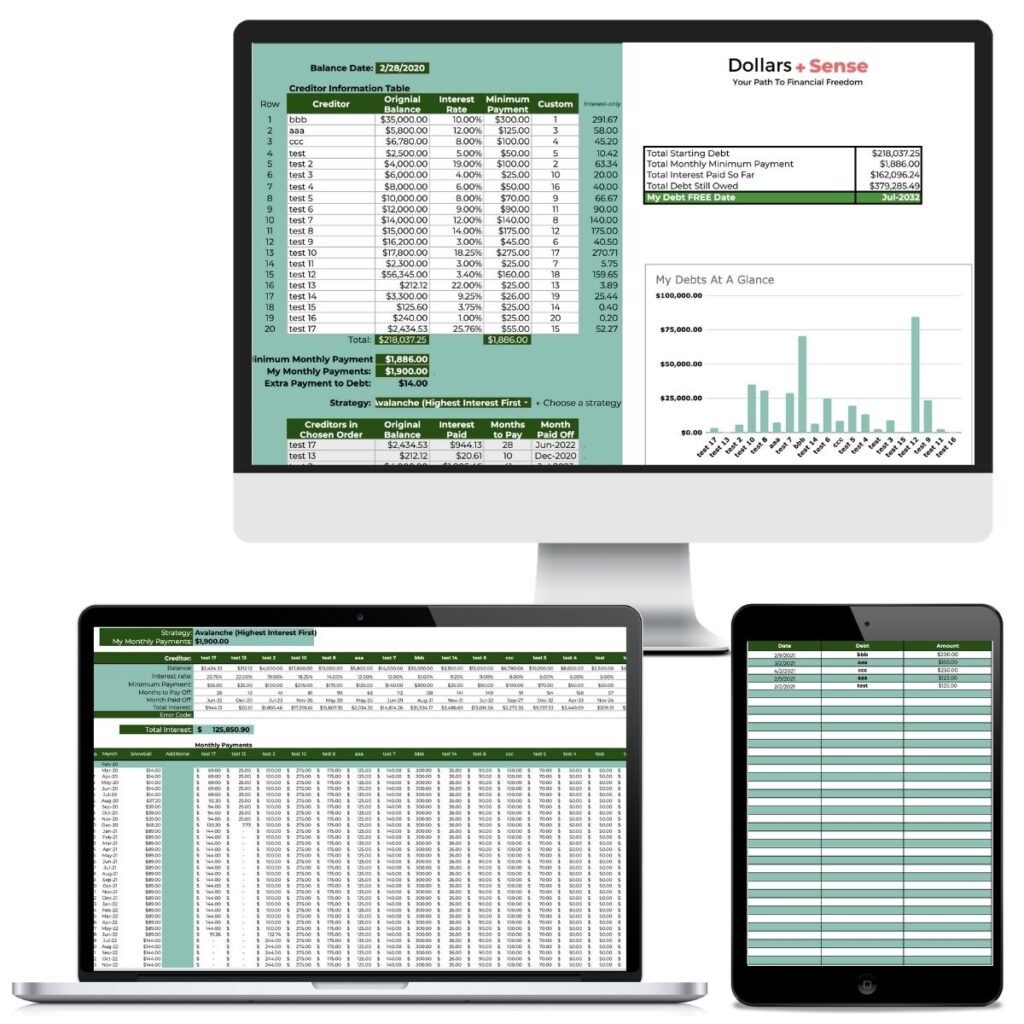

Next, make a debt repayment plan. If you need help creating a debt repayment plan, check out my Debt Payoff Spreadsheet.

This spreadsheet will help you create a plan to pay off your debt in the shortest amount of time possible and show you your debt-free date.

If you can’t afford to pay your back taxes in full, you can contact the IRS to set up a payment plan. This will allow you to make smaller payments over time until the debt is paid off.

Additionally, you can try to negotiate with the IRS to have them accept a lower amount than what you actually owe. This is known as an Offer in Compromise. However, it is important to note that not everyone will qualify for this program.

If you’re struggling to pay your back taxes, it’s important to reach out to the IRS and discuss your options. They may be more flexible than you think. But, if your CSED is in the near future, it makes sense to avoid any actions that toll the IRS statute of limitations—such as applying for an installment agreement or Offer in Compromise.

How To Negotiate A Payment Plan With The IRS

If you’re having trouble paying your taxes, you can reach out to the IRS and try to negotiate a payment plan. The IRS would rather collect something rather than nothing, that’s why they’re willing to negotiate with you to receive any unpaid taxes.

Like a credit card bill, you can agree to an installment plan where you pay your unpaid tax debt a little bit at a time. However, keep in mind that although this option is available, you increase your tax debt (because of fees, penalty, and interest) when you choose the installment option. So, if it is possible you want to pay your balances in full to minimize additional charges.

Assuming you can’t pay your tax debt in full when negotiating an IRS payment plan, I recommend requesting what’s called a short-term payment plan. This type of payment plan usually lasts 180 days or less and doesn’t have a user fee. You should only request a short-term payment plan if you believe you will be able to pay your taxes in full within the time period of 180 days or less.

If you’re not able to pay your taxes within that time frame, then you can try to negotiate a long-term payment plan with the IRS. With this type of payment plan, you have an installment agreement and you’re paying monthly—however, it has more fees associated with it than the short-term payment plan.

The best way to request a payment plan with the IRS is to use the Online Payment Agreement (OPA) application, or calling them directly at 800-829-1040 and speaking with a customer service representative.

Whatever route you choose, make sure you stay in contact with the IRS and keep up with your payments. If you fall behind on an installment plan, the IRS can revoke the agreement and start pursuing other collection methods, such as wage garnishment or levies.

What Are The Consequences Of Not Paying Your Taxes?

The government has the authority to forcibly seize your assets if you don’t try to make good on your income tax liability. In the most extreme situations, you may be subject to jail time.

If you do not pay your taxes by the due date, you will begin to accrue interest and penalties on the total sum.

At a certain point, the IRS will send you a letter demanding payment for your outstanding tax debt. If you ignore this letter, at some point the IRS may file a Notice of Federal Tax Lien to alert creditors that the IRS has a right to your personal property, real estate, or other assets. A lien secures the government’s claim on your property.

If the debt is not paid in a timely manner, the IRS may impose a levy on you. An IRS tax levy is the legal seizure of your assets in order to pay off your outstanding tax debt. Levies may be imposed in a variety of ways, including garnishing your wages directly from your employer, seizing and selling your property (such as a car or house), and taking your funds directly from your bank accounts.

In the most severe situations, the IRS may pursue criminal charges against you for tax evasion.

If the IRS does not collect on a balance due within the statutory period, the debt is considered “uncollectible.” As a general rule, this doesn’t mean that you no longer owe the money—it just means that the IRS can no longer take legal action to collect it from you.

What To Do If You Can’t Pay Your Taxes?

If you are in deep financial trouble and have a financial hardship, you can apply for Currently Not Collectible (CNC) status with the IRS. This will stop collection efforts until your income reaches a point where you can potentially begin to make debt payments. For example, the IRS won’t levy your assets and income. However, the IRS will still charge interest and penalties to your account and may keep your tax refund and apply them to your debt.

Before approving a request to delay collection, the IRS may ask for information about your financial status. They review your income and expenses and decide whether you can sell any assets or get a loan. If the IRS agrees you can’t both pay your taxes and your basic living expenses, it may place your account in CNC status.

Remember, the IRS won’t suspend interest and penalty charges, even if it stops trying to collect the balance due. So, you may want to consider other possible payment options you can afford before asking the IRS to place your account in CNC status.

If the IRS places your account in CNC status, they may contact you to update your financial information to be sure your ability to pay hasn’t changed. If your financial situation has improved when they conduct an annual review of your income the IRS may collect the balance you owe.

If you need help with your tax debt, it’s a good idea to contact a tax professional today to discuss your options and figure out the best course of action for your unique situation. A good option is the Taxpayer Advocate Service. They are an independent organization within the IRS and their services are free. These tax professionals can help you understand your options and take steps to resolve your debt. You can reach out to them HERE.

Always File Your Taxes On Time

One of the best things you can do to avoid tax debt is to always file your taxes on time, even if you cannot pay the full amount owed. Ignoring the filing deadline will only make your situation worse. By filing your return on time, you will avoid costly late-filing penalties and additional interest—so make sure you file your taxes on time during your tax year.

If you want to learn more about the penalties/interest rates for late payments and late filing, you can visit the IRS website.

Summary

The bottom line is that if you owe back taxes to the IRS, you should not wait to take action. The sooner you address the issue, the easier it will be to resolve it. If you need help, there are a number of tax professionals that can assist you. Do not hesitate to reach out for help if you are struggling to deal with back tax debt.

Related Articles

- Best Debt Snowball Spreadsheet: Pay Off Debt Fast

- 9 Things To Do When You Need Help Paying Bills

- 10 Best Things To Do With Your Tax Refund

If you want to remember this article, post it to your favorite Pinterest board.