Do you have an emergency fund? If not, saving for an emergency should be your first financial priority. Your emergency fund can help you stop adding to your debt whenever you have a financial hardship or help cover the things you don’t budget for. Find out how much you should have in your emergency fund and to build an emergency fund quickly.

Jump Ahead To:

What Is An Emergency Fund

An emergency fund is money set aside to cover large unexpected expenses or to help you through hard financial times—like a job loss. Having an emergency fund also prevents your budget from getting thrown off when an unexpected expense comes up. Preparing for the unexpected is necessary to avoid getting further into debt.

Is $1,000 Emergency Fund Enough?

Many personal finance gurus, such as Dave Ramsey, recommend saving $1,000 in an emergency fund before paying off any high-interest debt. But is a $1,000 emergency fund really enough? The short answer — no.

However, having $1,000 is a good start and the baseline that anyone should have before they think about paying off their high-interest debt.

Even Dave Ramsey recognizes that a $1,000 emergency fund is not enough. But Dave’s reasoning is “it makes you start thinking about how to handle emergencies and other ways to fix it instead of putting it on easy payments.” In other words, Dave Ramsey is saying you’ll put a little more effort into saving money and finding a solution to fit within the cash that you have.

The goal is to not have to rely on debt as an option. Therefore, even a small $1,000 emergency fund will save you from having to get further into credit card debt, borrowing money from friends or family, taking out a payday loan, or pawning off an important possession.

A $1,000 emergency fund is a good start because that amount is usually enough to get you through most emergencies — such as sudden car repairs, a trip to the urgent care, or an emergency trip to the vet. However, $1,000 is not nearly enough if you were to have an unexpected job loss (as a lot of us have seen with this recent COVID-19 pandemic).

How Much Money Should You Have In Your Emergency Fund?

The size of your emergency fund depends on your personal situation. I suggest you have an emergency fund that is at least 3 to 6 months’ worth of living expenses.

When I say “living expenses” I mean only necessities, such as rent and groceries. I don’t mean shopping, entertainment, dining out, or vacations.

If you are ever in a situation where you have to rely on your emergency fund, you shouldn’t be taking vacations or dining out anyway.

I recommend saving 3 months’ worth of living expenses if you have relatively strong financial or job security. I recommend 6 months (or more) if you have some instability in your employment or if finding another job could take you a long time.

How To Build An Emergency Fund

Now that you know exactly how much money you should have in your emergency fund, it’s time to take the next steps and actually build your emergency fund. Here are some tips to help you find the money to contribute to your emergency fund.

1. Make A Budget

The first step to building your emergency fund is to make a budget. When it comes to your emergency fund, haveing a budget is important for two reasons:

- Having a budget allows you to see how much your expenses are. You need to know how much your monthly expenses are in order for you to know how much money you need in your emergency fund.

- Having a budget can help you track your spending and figure out what areas of your life you can cut back on spending. Cutting back on spending will allow you to have more money to put towards your emergency fund.

Once you have your budget set up, you should have a good understanding of how much your living expenses are and how much money you need in your emergency fund.

If you’re just starting out, you can download this FREE Monthly Budget Worksheet.

However, if you want something a little more sophisticated, you can get my Budget Templates. This is the template I use to save over 50% of my income and it is the same template I use to this date.

These templates make it easy to see exactly what percent of your income you’re saving. It also shows you what percent of your money you are spending. Finally, it has an emergency fund calculator built in to make it easy for you to calculate how much you need to save and to remember your savings goals.

If you want to learn more about exactly how I use this excel spreadsheet, you can read my detailed article “How I Use My Monthly And Yearly Household Budget Spreadsheet.”

2. Track Your Spending

Once you make a budget, you need to track your spending to make sure you are sticking to the plan. It’s important to review your budget on a regular basis to make sure you are staying on track.

If you want to stay on top of your spending habits, use this FREE Daily Expense Tracker.

If you don’t like to manually track your spending (like me), you can use a third-party website like Empower to see your spending all in one place. Empower is a FREE wealth management tool to help you get a better understanding of your finances.

After you link all your accounts, you can see all your accounts in one place to have better money oversight.

If you sign up today and link at least one of your investment accounts (with a balance of more than $1,000), we’ll each get $50. That’s FREE money for keeping track and staying on top of your finances (something you should be doing anyway)!

- Related Article: 3 Easy Ways To Track Your Spending

3. Cut Your Expenses

Cutting expenses is important because the less you spend, the less money you will need for your emergency fund. An additional benefit to spending less money is you can save more. The more money you save, the faster you can build your emergency fund.

- Related Article: Cutting Your Monthly Expenses: Why It Is Absolutely Necessary

4. Find Ways To Save More Money

There are only so many expenses you can cut. So once you’ve cut back as much as you comfortably can, find ways to save more money on the things you have to buy.

You can also save money on the things you already buy every day by getting cash back from places like Rakuten.

Use the Rakuten browser extension to make it even easier for you to earn cash back. The way the browser extension works is when you land on a store page, Rakuten shows you how much cash back is available. Just shop as normal and then get paid by check or PayPal. It’s that simple.

If you want to learn how you can save a significant amount of money every month, read my detailed article “How To Save At Least 30 Percent Of Your Income Every Month.”

5. Increase Your Income

The more money you have coming in, the more you can put towards your emergency fund. Again, there’s only so much money you can save by cutting expenses, but there’s no limit on how much money you can make.

I also recommend you have more than one way to make money. The more streams of income you have, the more financially secure you become. If for some reason one stream of income dries up, you can rely on your other streams. Finally, the more streams of income you have, the less money you will need in your emergency fund because you are more financially secure.

If you’re looking for some ways to increase your income, read my detailed article “5 Ways To Increase Your Income Streams.”

Where Should I Store My Emergency Fund?

At this point, you know how much you need in your emergency fund and have an idea of how to build an emergency fund. Now it’s time to figure out where to keep your emergency fund.

Since an emergency can strike at any time, having quick access to your money is crucial. Another important factor is your money needs to be safe. You don’t want to put your money in a place that you can lose money.

I recommend keeping your emergency fund in a secure location, such as a money market account or a savings account. Let’s discuss the difference between a savings account and a money market account.

Savings Account

A savings account is a basic bank account. When you deposit your money in a savings account, a bank makes loans with your money. The bank pays you interest for the privilege of using your money.

Open a high yield savings account to an online bank account. You get two benefits by opening an online savings account:

- They usually pay higher interest on your money than a brick and mortar bank; and

- It reduces impulse purchases because your money is a little harder to access. With online banks, it usually takes a few business days for the money to be transferred to a physical bank where you can withdraw cash.

I recommend CIT Bank because they pay competitive interest rates (right now it’s 10x the national average), have no monthly maintenance fees, and you only need $100 to open an account.

Money Market Account

A money market account is a type of savings account that usually earns a higher amount of interest than a basic savings account. However, it usually requires a higher minimum deposit and daily balances.

Some additional benefits you get with a money market account that you do not get with a savings account are that you will typically receive a debit card and checks. This makes your account easier to access in case of an emergency and is more liquid than a savings account.

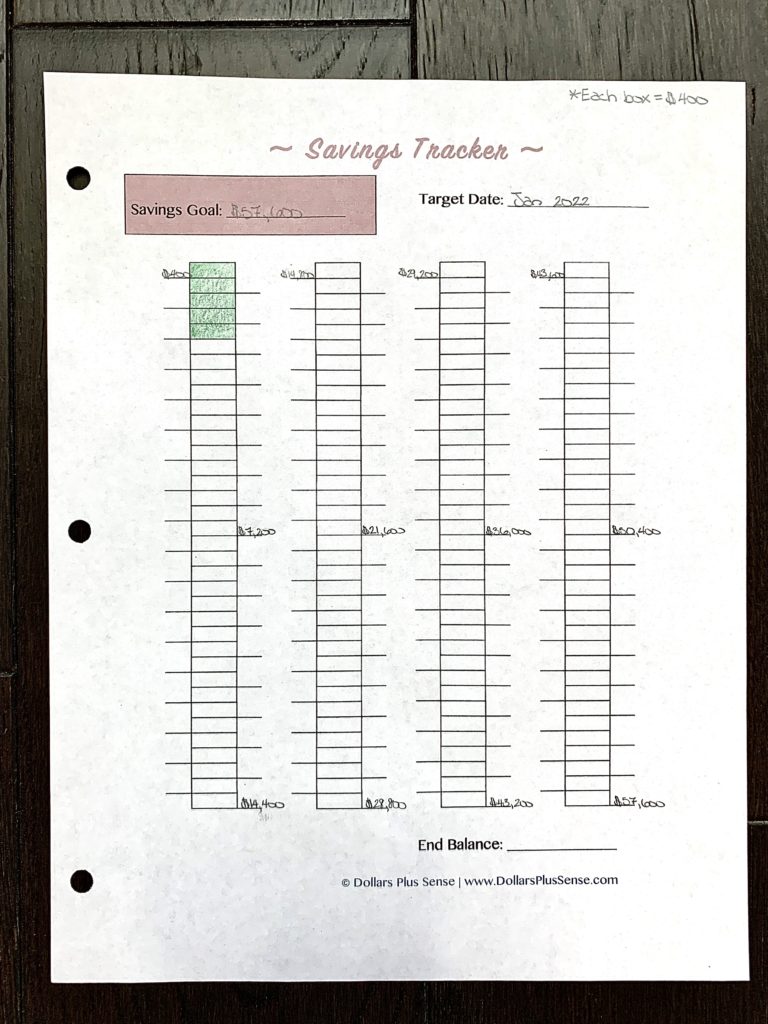

Get this Savings Tracker to keep track of your emergency fund savings goal. Color in each box as you put money towards your savings goals. Use this visual to make savings fun and motivate you to keep going until you reach your goal!

Savings accounts and money market accounts are similar in the sense that the Federal Deposit Insurance Corporation (FDIC) insures deposits. The FDIC insures against loss up to the federal limits of $250,000.

You can deposit money into savings and money market accounts as often as you want. However, federal regulations prohibit withdrawals to no more than six per month.

Please don’t confuse money market accounts with money market funds because they are very different. Money market funds are a type of mutual fund that invests in the debt of governments and corporations.

In short, the difference between a money market account and a money market fund is that money market funds are seen as an investment and are not FDIC insured. So if a bank fails, you will not get your money back from the FDIC with a money market fund.

I personally like money market accounts better than savings accounts for my emergency fund because they usually pay higher interest rates than savings accounts.

But keep in mind you will probably need a higher minimum account balance than a savings account—although there are some banks that do not require a higher minimum balance for their money market accounts.

Taking all these things into consideration, you should choose the option that’s best for you. You can start your research by seeing some of the best savings accounts HERE and some of the best money market accounts HERE.

But no matter where you decide to store your emergency fund, you should set a monthly savings goal and automate your savings. You can easily automate your savings by setting recurring transfers to your bank.

- Related Article: How To Choose The Right Savings Account For Your Financial Situation

Where NOT To Keep Your Emergency Fund

Now that you know how to build an emergency fund, it is important to know what accounts you should NOT hold your emergency fund.

CDs

At some banks, other types of savings accounts include certificates of deposit (commonly called CDs).

With CDs, you deposit your cash with a bank and agree not to withdraw your money for a specified period of time. In return for that promise, the bank will usually pay you a higher interest rate than a savings account and a money market account.

I typically don’t recommend keeping your emergency fund in a CD, although it pays a higher interest rate than the two other savings accounts we discussed. The reason is your money is locked in for a specified period of time.

If an emergency arises and you are forced to withdraw your money from a CD prematurely, you will get hit with an early withdrawal penalty.

CDs are a good choice for short term savings goals that you know you won’t need the money for at least a year or two in the future. CDs are not for emergency funds because you won’t know when you will need the money.

Stocks or Bonds

You also don’t want to keep your emergency fund in stocks or bonds.

You may be tempted to put your emergency fund in stocks or bonds because you want to earn more interest than a savings account. However, this is a mistake because the value of your stocks or bonds can go down.

Although you can sell stocks or bonds if you need to, you may have to sell it at a loss if your emergency occurs during a downswing.

For emergencies, you need a guarantee that your money will be there when you need it. Therefore, play it safe and keep your money in a savings account or money market account.

Emergency Fund Vs. Savings

It’s very important for you to understand the difference between your emergency fund and your savings account — because they both play a different role when it comes to your finances.

Your emergency fund is strictly for unexpected expenses. It shouldn’t be used for anything else besides that.

On the other hand, your savings account is where you save for a specific financial goal or expected expenses. For example, your savings account is for things like your down payment for a house, saving for a car, saving for a vacation, or for your other sinking funds.

It’s important that you keep your emergency fund separate from your everyday savings account so it’s clear to you what that money is for. You don’t want to accidentally spend your emergency fund because you thought it was for some other purpose.

What To Do After Emergency Fund?

Once you have at least $1,000 in your emergency fund, you can focus on paying off high-interest debt. Debt is a drain on your finances and slows down your achievement of financial freedom or any other financial goals.

Speed Up Paying Off Your Debt

I recommend you pay your debts off from highest interest rate to lowest interest rate, regardless of the amount. This is because you will pay less interest if you pay off your highest-interest debt first.

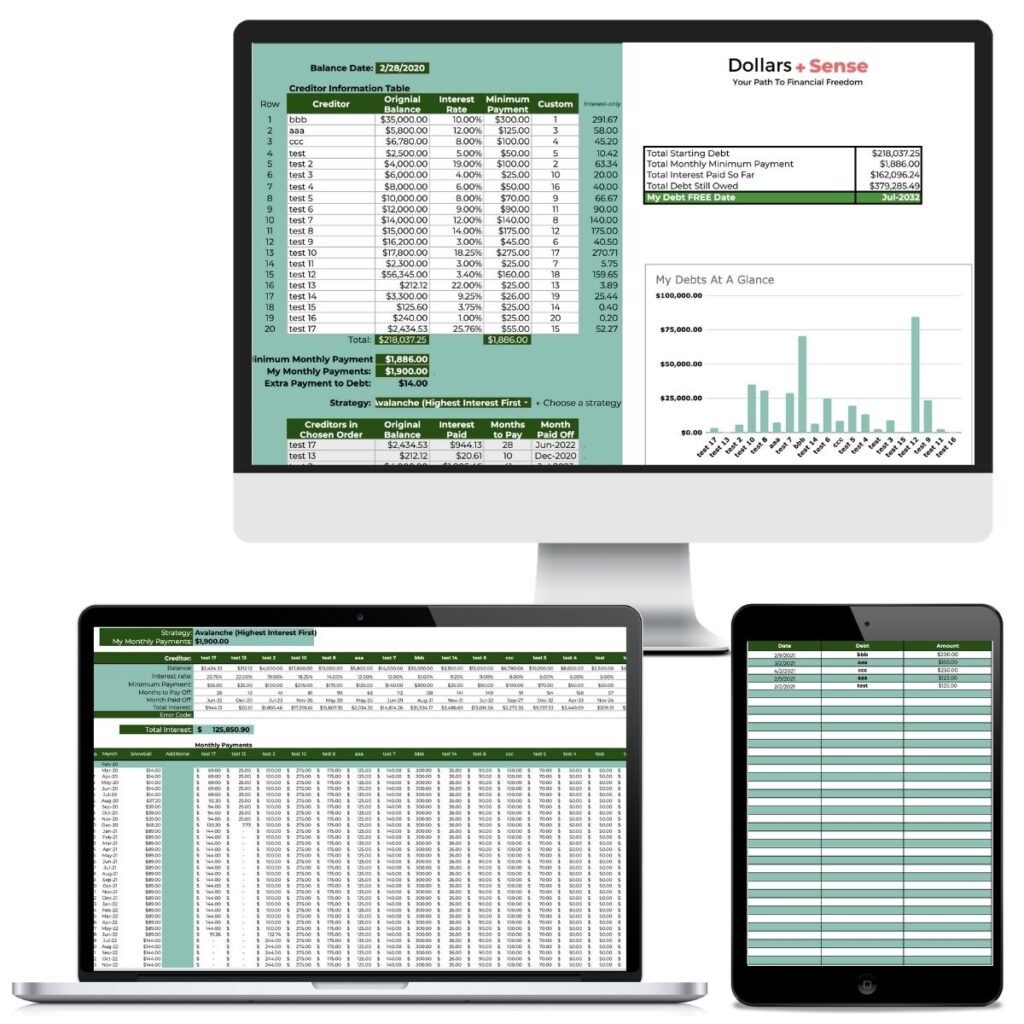

Use this Debt Worksheet to help you get organized and make a debt repayment plan.

Once you have a debt repayment plan, you can use my Debt Payoff Spreadsheet.

A debt payoff spreadsheet is a way to organize all your debt information so you can see it in one place and easily manage debt. This is great because it will help you determine which debt should be paid first, last, or somewhere in between.

Being organized and having all your debt in one place will help you stay focused, motivated, and eliminate debt as soon as possible.

It’s really easy to use. All you have to do is enter your debt information and it tells you exactly how long it will take to be debt-free.

My Debt Payoff Spreadsheet is exactly what I used to pay off over $100,000 in three years.

Also, consider refinancing your high-interest debt. Now is a good time to look into refinancing your debt because you can potentially save a LOT of money.

- Related Article: Debt Snowball Vs. Debt Avalanche: Which Method Is Best?

Other Financial Goals

Once you have your emergency fund set up and have paid off your high-interest debt, it’s time to start thinking about some other financial goals you want to accomplish. Here are some ideas of financial goals you may want to accomplish:

- Save for retirement

- Buy a house

- Build up non-retirement investment accounts

- Save for your children’s education

- Start a business

This list is just to help give you ideas, so think about what’s important to you as you begin to set your goals. If you find yourself having multiple goals you would like to achieve, read my article “The Best Way To Prioritize And Achieve Your Financial Goals” to help you figure out which goal to work towards first.

Summary

Congratulations on learning how to build an emergency fund. You want to make sure you have a budget before establishing your emergency fund. Having a budget will help you determine how much you need in your emergency fund.

Once you have a good idea of your monthly necessary expenses, you should have an emergency fund that will cover at least 3-6 months of expenses.

Finally, be sure to keep your emergency fund money in a safe place like a savings account or money market account. Knowing how to build an emergency fund will allow you to feel more secure because you will be prepared for the unexpected.

Related Articles:

- How I Saved $300,000 In 4 Years

- 7 Things To Do If You Think Another Recession Is Coming

- How To Save For Different Financial Goals

If you want to remember this article, pin it to your favorite Pinterest board.

16 Comments on How To Build An Emergency Fund